African farmers: $21/cow/year. African dairy market: $74 billion. The money’s flowing—just not to farmers.

EXECUTIVE SUMMARY: Africa’s dairy market will reach $74 billion by 2035, yet local farmers capture just 2-3% while 80% flows to imports. The paradox: Africa owns 20% of global cattle but produces only 5% of milk, with farmers earning $21-200 per cow annually versus $1,800 breakeven in developed markets. Multinationals dominate through powder reconstitution rather than local sourcing—it’s cheaper to import at 5% tariffs than to collect from smallholders who produce 1-3 liters daily. East Africa proves transformation is possible, with Kenya and Rwanda becoming exporters through cooperatives and smart policy, while West Africa remains import-dependent. For global dairy professionals, success means abandoning Western models for adapted genetics, intermediate technologies, and hybrid strategies that match Africa’s unique reality—not replicating Wisconsin in Lagos.

At a recent dairy conference, I found myself in conversation with several producers interested in African opportunities. They’d all seen the same presentations—Africa’s dairy market reaching $74 billion by 2035, up from $61.7 billion today, according to IndexBox’s November 2024 analysis. “Last frontier for dairy,” one called it.

After spending the past few months examining the dynamics on the ground, I’ve come to realize we’re dealing with something far more complex than most investment presentations suggest. Africa isn’t developing a conventional dairy sector like we’ve seen elsewhere. Instead, it’s creating a unique hybrid system that challenges our traditional understanding of dairy market development.

The Market Growth Story: Real but Different

Understanding the Demographic Shift

The fundamentals driving growth are undeniably strong. McKinsey’s consumer research from June 2023 documented that Africa’s urban middle class is expanding from 300 million today to 500 million by 2035. That’s a demographic shift comparable to adding the entire U.S. population as potential dairy consumers.

What’s particularly noteworthy is how consumption patterns are evolving. Ethiopia’s Ministry of Agriculture reported in their 2024 sector review that urban dairy spending has accelerated dramatically, especially among middle-income households. Kenya’s Dairy Board projects 5.8% annual consumption growth through 2030—that’s faster than most Asian markets at a similar stage of development.

The Import Reality Check

Yet here’s where the story becomes more nuanced. The FAO’s November 2025 Africa Food Security Report reveals that approximately 80% of this consumption growth is met by imported dairy products and reconstituted powders, not by expanded local production.

“The continent currently produces just 5% of global milk while maintaining 20% of the world’s cattle.”

According to UN Comtrade data from 2024, Africa imports $7.5 billion in dairy products annually, with projections suggesting this could reach $15 billion by 2035. The European Milk Board’s October 2024 analysis shows traditional and fat-filled milk powder accounting for 76% of these imports—particularly dominant in West African urban centers.

KEY MARKET INDICATORS: The Scale of the Challenge

- Current African production: 53.2 million tons (5% of global output)

- Cattle population: 20% of the global herd

- 2024 import value: $7.5 billion

- Projected 2035 imports: $15+ billion

- Powder products as a percentage of imports: 76%

- Estimated local farmer share of market growth: 2-3%

Why Local Production Can’t Keep Pace

The Sobering Economics

I recently reviewed research from Mountaga Diop and colleagues at Senegal’s Institute of Agricultural Research, published in 2023. Their findings on smallholder economics were sobering:

“Average annual net returns of just $21.70 per cow”

In Kenya, often highlighted as a success story, the Kenya Institute for Public Policy Research’s 2024 analysis shows that farmers average $200 in annual profit per cow, with daily yields of 5-8 liters.

To put this in perspective, a Wisconsin producer recently told me their breakeven is around $1,800 per cow annually. The disparity illustrates fundamentally different economic realities.

Three Structural Challenges Blocking Progress

1. Feed Economics That Don’t Work

ILRI’s comprehensive study across eight African countries in 2024 found that feed accounted for 70% of production costs, compared to the 40-50% we typically see in North American operations. This difference alone changes everything about profitability calculations.

Ben Lukuyu, ILRI’s principal scientist for feed and forage development in Nairobi, shared with me that Kenya and Uganda face approximately 60% annual feed deficits. When the Russia-Ukraine conflict drove fertilizer prices up 81.9% and feed costs up 13.3%, many marginally viable operations simply couldn’t survive. And that’s in Kenya, which has better infrastructure than most.

2. Climate Stress Destroying Yields

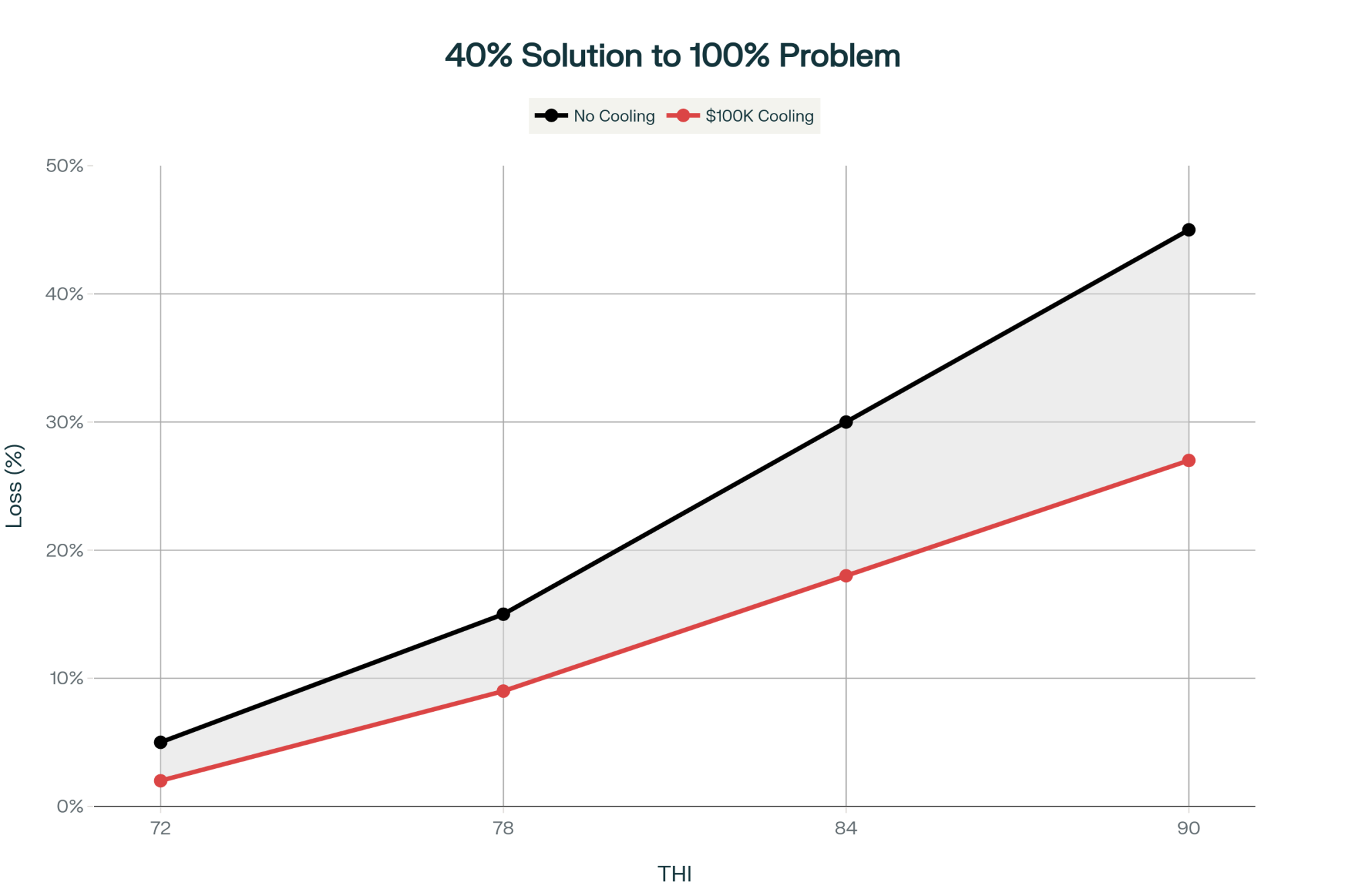

The University of Melbourne’s research team, with support from the Gates Foundation, published compelling data in Animal Production Science this March. They documented Holstein yield reductions of 17-53% under African heat stress conditions—far exceeding what we see even in challenging U.S. environments like Arizona or Southern California.

“South Africa saw average yields decline from 21 liters to 16.1 liters per cow between 2018 and 2023—a 23% drop in the continent’s most developed dairy market”

This comes from the USDA Foreign Agricultural Service’s February 2025 report, and it’s particularly concerning because South Africa has the infrastructure we’d expect to mitigate these challenges.

3. Infrastructure That Can’t Support Growth

The World Bank’s 2024 Cold Chain Assessment estimates:

“Africa loses up to 40% of perishable food due to inadequate cold storage.”

CIRAD’s research indicates that only 1-7% of locally produced milk in West Africa enters formal trade channels. The investment required to fix this—estimated at $50-100 billion for comprehensive cold chain development—exceeds current funding commitments by roughly tenfold.

What Multinationals Are Actually Building

The Reconstitution Reality

The expansion strategies of major dairy companies offer important insights. Nestlé, Danone, and FrieslandCampina are indeed investing heavily across Africa, but their business models differ significantly from what many expect.

Okereke Ekumankama’s 2023 research at the University of Nigeria examined FrieslandCampina’s operations in detail. While the company controls 75% of Nigeria’s dairy market, they source virtually no local milk. Instead, they import powder from Europe for reconstitution in Nigerian facilities.

When “Development Programs” Don’t Develop

Their Dairy Development Programme, launched in 2010, aimed to integrate smallholder farmers. However, Ekumankama’s field research with 250 participating farmers revealed persistent challenges preventing meaningful integration.

The transaction costs of collecting from dispersed producers, averaging 1-3 liters daily, often in areas lacking roads, electricity, or cold storage, exceed the economics of importing powder at 5% tariff rates.

This pattern—building processing capacity for imported inputs rather than developing local supply chains—appears across much of the continent. It creates employment and provides affordable dairy products to urban consumers, which has value. But it doesn’t necessarily translate to local dairy sector development.

East Africa: A Different Story Emerges

The Success Stories

East Africa presents a notably different picture. The FAO’s October 2024 regional report shows the region accounting for 48% of Africa’s total milk production, with 26% growth between 2013 and 2023.

Rwanda’s Systematic Transformation

According to their Ministry of Agriculture’s presentation at September’s IDF Regional Conference:

- Milk production tripled from 334,727 metric tons in 2010 to 1,092,430 metric tons in 2024

- Per capita consumption doubled from 37.3 to 79.9 liters annually

The key? Mandatory quality testing at milk collection centers through Ministerial Order 001/11.30, strategic genetics programs with Heifer International, and sustained government investment spanning multiple administrations.

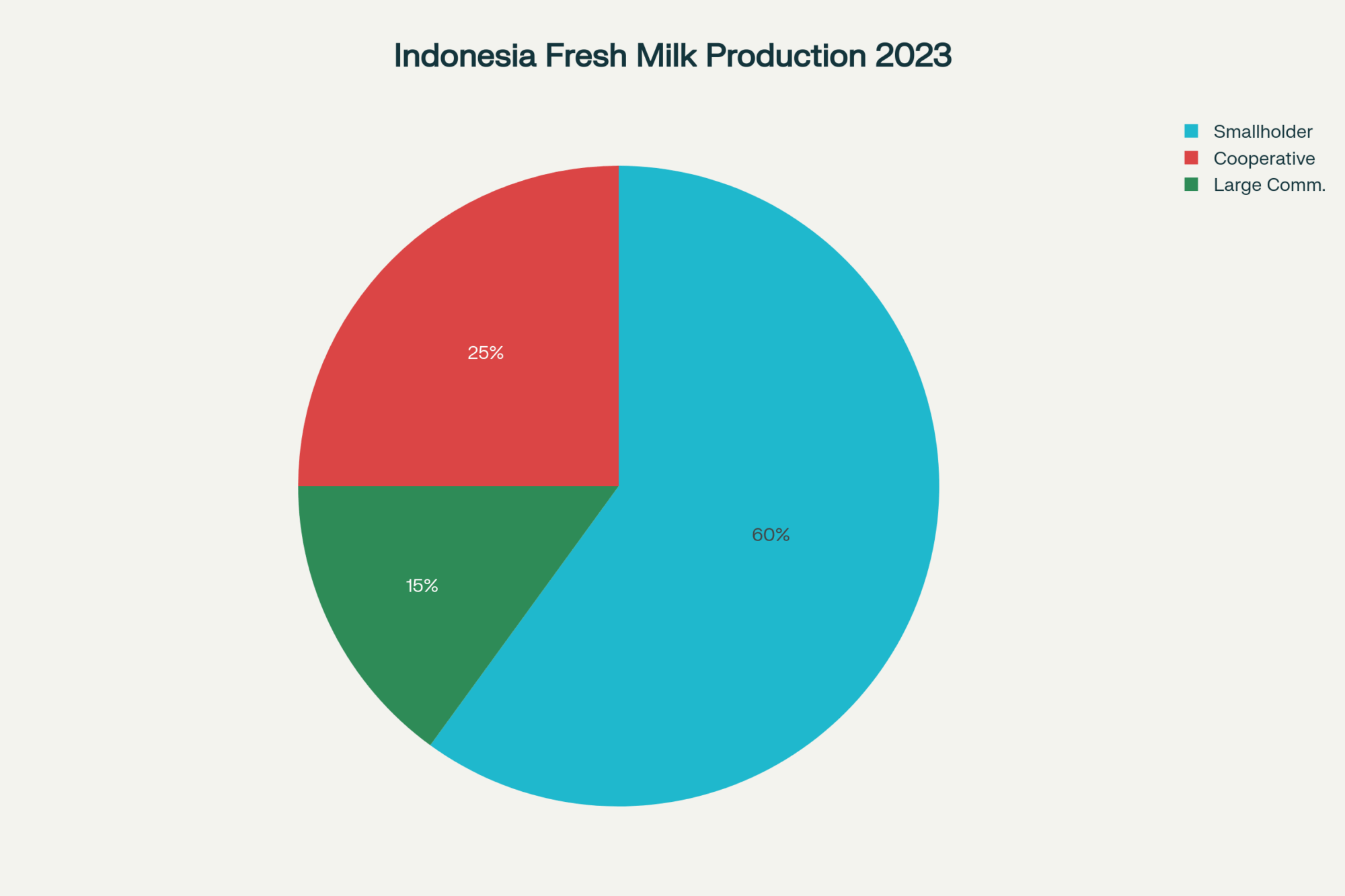

Kenya’s Cooperative Advantage

Kenya produces 5.7 billion kilograms annually, according to the Dairy Board’s 2025 outlook, with 80% originating from smallholder operations. The success factor isn’t individual farm productivity—yields remain at 5-8 liters per cow daily. Rather, it’s cooperative strength.

“Without the cooperative, I’d be selling to brokers at whatever price they offer. Now we negotiate as a group, and we get veterinary services I could never afford alone.”

— James Kibiru, dairy farmer in Nyeri County

Consider Meru Dairy Cooperative Union, which engages over 35,000 farmers through annual field days. They provide milk aggregation, veterinary support, quality-based payment systems rewarding butterfat performance, and collective bargaining power.

Uganda’s Export Achievement

IFPRI’s 2023 value chain analysis documents Uganda’s growth from a $2 million dairy industry in 2008 to $150 million by 2017. The country now exports $500 million worth of milk powder to Algeria, according to their Ministry of Trade’s 2024 data.

West Africa: Where Different Challenges Persist

I spoke with Kwame Asante, who manages a small dairy operation outside Accra, Ghana. “We can produce milk,” he told me, “but getting it to market before it spoils? That’s the real challenge. The processors prefer powder—it’s easier, cheaper, more reliable.”

His experience reflects broader West African dynamics. Ghana’s Fan Milk, now owned by Danone, built one of the region’s most successful distribution networks. Those yellow tricycles are everywhere in urban areas. Yet, as industry data shows, the operation relies primarily on imported powder, with local farmers supplying only about 2% of the processed volume.

The economics make sense from a processor perspective. A solar-powered cooling system for a single collection center runs about $15,000-20,000 according to equipment suppliers I’ve spoken with. When you’re collecting 50-100 liters daily from that center, the payback period stretches beyond what most investors will accept.

Policy Choices That Make or Break Markets

The Tale of Two Approaches

Timothy Njagi at Kenya’s Tegemeo Institute documented how the country’s 2015 implementation of a 10% import levy plus 16% VAT on milk imports catalyzed transformation. Average daily yields from indigenous breeds increased by approximately 300% over the following decade, shifting Kenya from a net importer to an exporter.

By contrast, West African nations maintain just 5% tariffs through the ECOWAS Common External Tariff. Oxfam’s 2024 trade analysis shows the result: continued heavy import dependency, with fat-filled milk powder (a blend of skim milk and palm oil) dominating 70% of consumption in major cities.

Nigeria’s New Attempt

Nigeria’s National Dairy Policy Implementation Framework, validated in November 2025, offers:

- Five-year tax holidays for processors

- Low-interest credit for farmers

- Guaranteed off-take schemes

Whether this succeeds where previous efforts struggled remains to be seen. The policy appears comprehensive on paper, but implementation has consistently been a challenge in Nigeria.

What This Means for Different Players

For Genetics Companies

Focus on adaptation, not maximum production. Raphael Mrode, who leads ILRI’s genetics program in Kenya, has been incorporating the “slick gene,” which confers heat tolerance through shorter, sleeker hair coats. These animals maintain reasonable productivity under conditions that would devastate conventional Holstein genetics.

The market opportunity exists for companies developing adaptation traits rather than pursuing maximum production designed for temperate conditions.

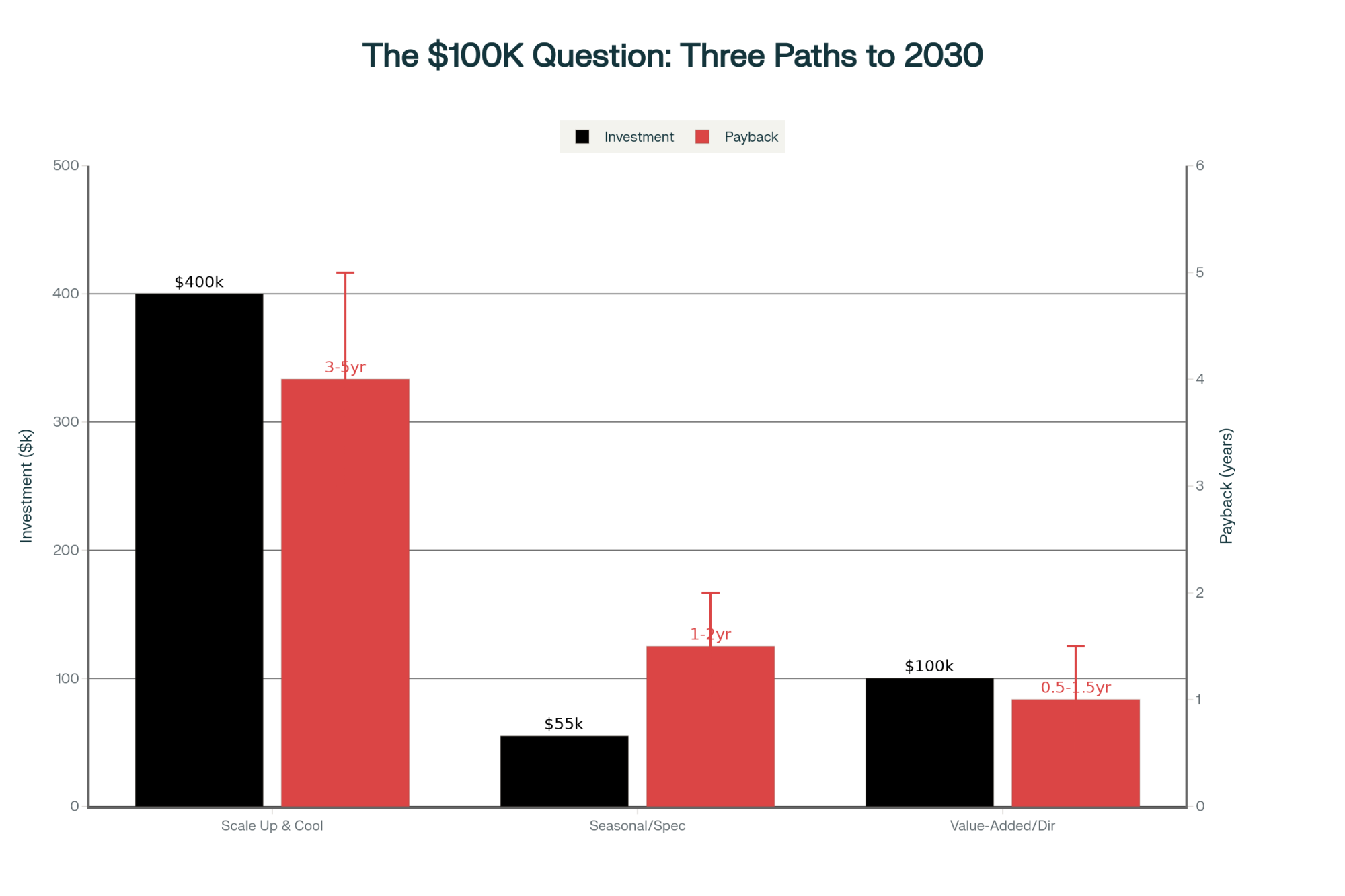

For Equipment Suppliers

Forget precision dairy technology designed for 1,000-cow operations. That’s not the market. Instead, think intermediate technologies: solar-powered cooling for collection centers (around $15,000-20,000 per unit), mobile apps for basic smartphones, robust milk testing equipment suitable for cooperative-level deployment.

Success requires matching technology to operational realities and economic constraints.

For Processors

Develop dual strategies: reconstitution capacity for urban markets while gradually building local collection infrastructure where economically viable. Don’t promise what you can’t deliver on local sourcing, but don’t ignore it either—governments are increasingly demanding local content.

The Bottom Line: Understanding the Real Opportunity

The $74 billion projection for the African dairy market from IndexBox appears realistic given demographic and income trends. However, understanding who captures this value—and how—requires nuanced analysis.

East African nations with strong cooperative structures and consistent policy support show genuine transformation potential. West Africa will likely remain import-dependent with selective local success stories. South Africa continues consolidating, potentially dropping below 500 commercial dairy operations by 2030.

What’s encouraging is seeing younger African dairy professionals returning from international training with fresh ideas. They understand both traditional systems and modern technology. They’re the ones who’ll ultimately bridge this gap between potential and reality.

For global dairy professionals, Africa represents opportunity—though not in ways that conform to conventional expectations. Success requires understanding the continent’s unique development trajectory, abandoning standard assumptions, and developing approaches appropriate to diverse regional contexts.

As we consider these opportunities, it’s worth noting that markets develop differently. Africa won’t follow the path of New Zealand or Wisconsin, or the Netherlands. It’s creating something new, and those who recognize and respect that difference will find the real opportunities.

This paradox—simultaneous consumption growth and production challenges—defines the current reality of African dairy. How the industry responds will shape both African food security and global dairy trade for decades to come.

What do you think? Are we looking at this opportunity the right way? I’d love to hear from producers who’ve worked in these markets or are considering investments there. The conversation continues.

KEY TAKEAWAYS:

- Africa’s $74B dairy market is an import story, not a production opportunity—80% flows to European powder while farmers earning $21-200/cow yearly capture just 2-3% of value

- Geography determines destiny—East Africa transforms through cooperatives and smart policy (Kenya exports after tripling yields), while West Africa stays import-dependent at 76% reconstituted powder

- The economics simply don’t work at the current scale—African farmers face 70% feed costs (vs. 40% globally), 40% infrastructure losses, and compete against powder imports at just 5% tariffs

- Success requires radical adaptation—heat-tolerant genetics (Holstein yields drop 17-53% in African heat), intermediate technology ($15K solar cooling, not $100K precision systems), and hybrid import-local business models

- Multinationals aren’t villains, they’re rational—FrieslandCampina controls 75% of Nigeria’s dairy using zero local milk because collecting from smallholders costs more than importing

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

- Heat Stress 2.0: Why Your Current Cooling Strategy Is Costing You Big Money – Provides actionable protocols for “smart soaking” and tiered cooling strategies that can recover the 17-53% yield losses cited in African herds, offering a blueprint for managing extreme climate challenges.

- Global Dairy Markets Signal Imminent Price Correction as Production Surge Overwhelms Demand – Explains the “supply tsunami” from major exporters driving the low-cost powder surplus that undercuts local African production, helping you understand the macro-economic forces fueling the import paradox.

- Bred for Success, Priced for Failure: Your 4-Path Survival Guide to Dairy’s Genetic Revolution – Reveals the accelerating gap between high-performance Western genetics and global operational realities, offering critical context for why “adapted” traits are becoming an economic necessity over pure production speed.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.