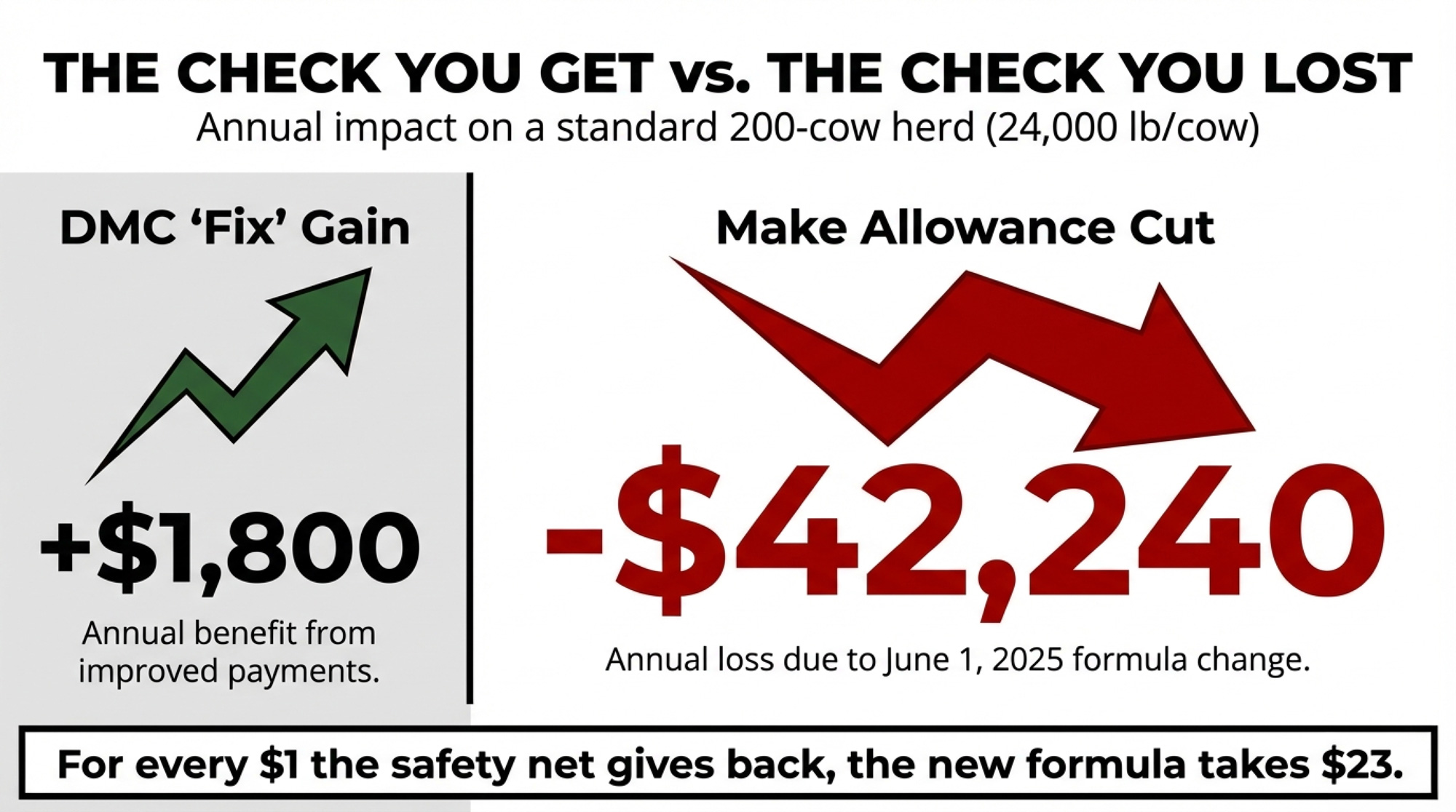

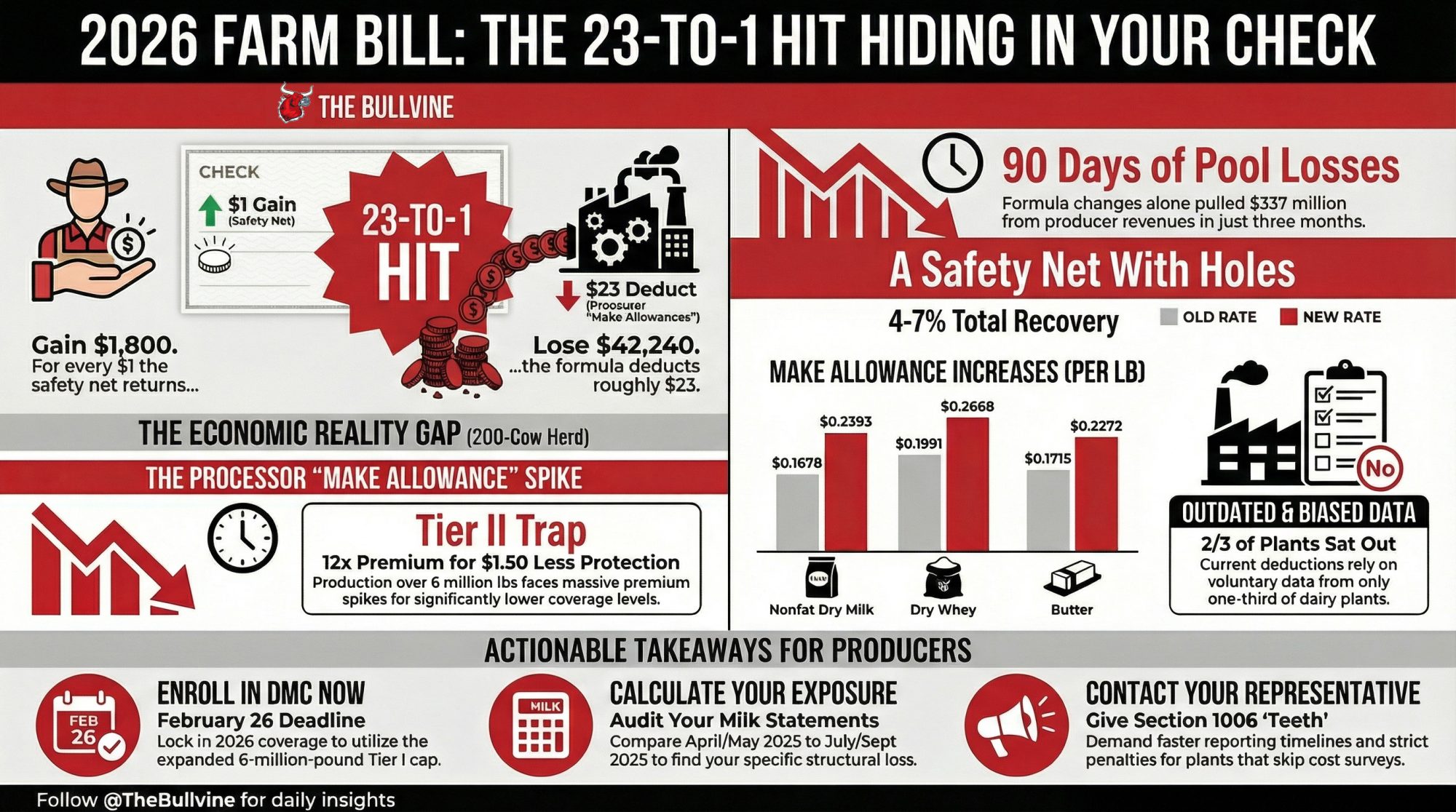

Your 200-cow dairy gets $1,800 from the 2026 Farm Bill — and loses $42,240 to make allowances. Ready to see the 23‑to‑1 hit hiding in your milk check?

Executive Summary: The House Agriculture Committee’s 2026 Farm Bill draft — released February 13 by Chairman GT Thompson — gives a 200-cow dairy roughly $1,800 a year in improved DMC payments. Make allowance increases that took effect on June 1, 2025, have already cost that same herd $42,240 annually. That’s a 23-to-1 gap, and AFBF economist Danny Munch has tracked $337 million in pool losses from the formula change alone in its first 90 days. The bill’s sharpest tool is Section 1006: permanent mandatory processor cost surveys — the only mechanism that could eventually push make allowances back down. But the FMMO hearing process has never reduced make allowances, and Munch’s own timeline puts the earliest possible relief at 2028, with a more realistic read closer to 2031. Markup starts on February 23, DMC enrollment closes on February 26, and Lolly Lesher at Way-Har Farms in Pennsylvania — who testified before the committee — is one of the producers watching to see whether Section 1006 gets real teeth or stays symbolic. Two deadlines, one structural gap, and a formula that’s never been adjusted in the farmer’s direction.

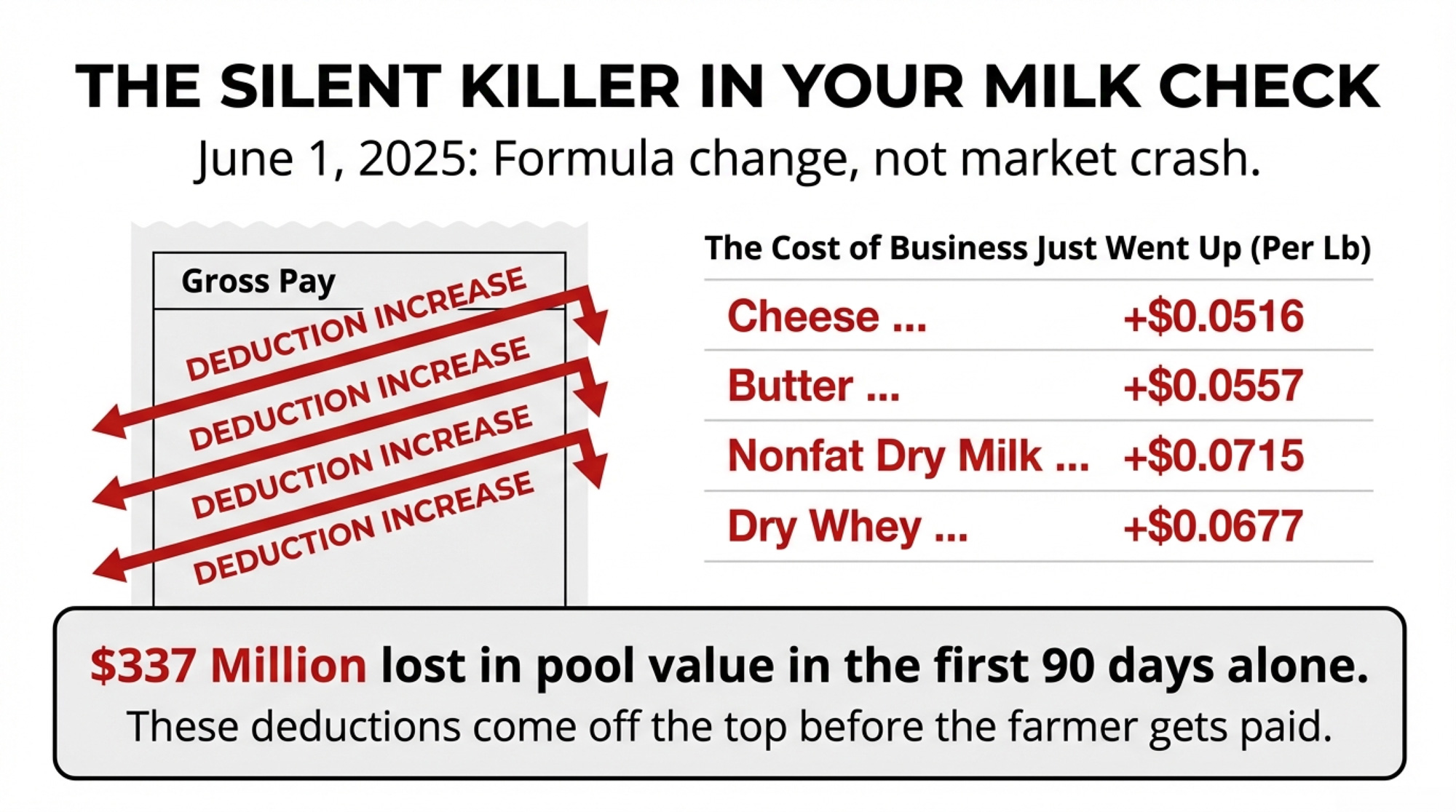

The House Agriculture Committee’s 2026 Farm Bill draft improves your Dairy Margin Coverage payment by roughly $1,800 a year on a 200-cow herd. The make allowance increases that took effect June 1, 2025, have already cost that same herd about $42,240 a year. That’s a 23-to-1 gap. For every dollar the safety net gives back, the formula takes twenty-three.

Those make allowance increases pulled $337 million out of producer pool revenues in their first 90 days, per AFBF’s September 2025 Market Intel analysis — not from a market crash, but from the formula change alone. It hit every FMMO-pooled dairy in America the same month Lolly Lesher at Way-Har Farms in Bernville, Pennsylvania, was bottling milk and scooping 90 flavors of ice cream alongside her milking herd of about 260 cows.

Lesher has talked publicly about what pricing instability means for multi-generational dairy families. She and her family expanded from 80 cows to over 200 when her daughter returned to the operation — because, as Lesher has discussed on the Lancaster Farming FarmHouse podcast, the economics of an 80-cow operation couldn’t stretch to support multiple family members coming back to the farm. “When milk prices flip-flop up and down so much,” she told the podcast, “you need to be well-versed in planning and how to handle the debt and the payments.” That planning just got harder. And the bill that’s supposed to help? It recovers somewhere between 4 and 7 cents of every dollar the formula already took.

Where Did $337 Million Go?

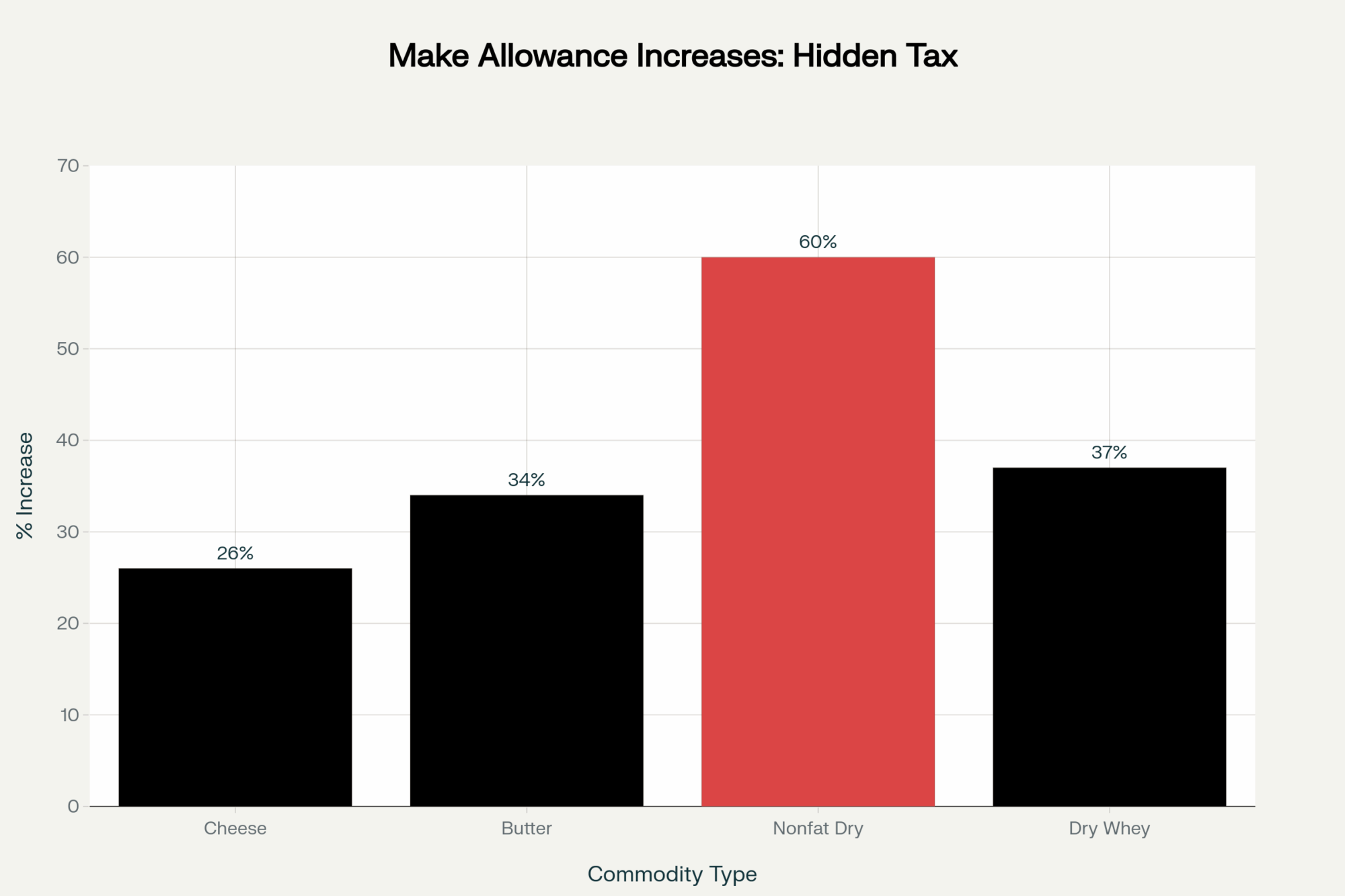

The make allowance increases weren’t part of this Farm Bill. They came through USDA’s FMMO modernization package, finalized in November 2024, approved by producer referendum in all 11 orders, and implemented on June 1, 2025. Make allowances — the per-pound deductions covering processor manufacturing costs, subtracted before farmers get paid — jumped across all four product categories:

| Product | Old Rate ($/lb) | New Rate ($/lb) | Increase ($/lb) | % Change |

|---|---|---|---|---|

| Cheese | $0.2003 | $0.2519 | +$0.0516 | +25.8% |

| Butter | $0.1715 | $0.2272 | +$0.0557 | +32.5% |

| Nonfat dry milk | $0.1678 | $0.2393 | +$0.0715 | +42.6% |

| Dry whey | $0.1991 | $0.2668 | +$0.0677 | +34.0% |

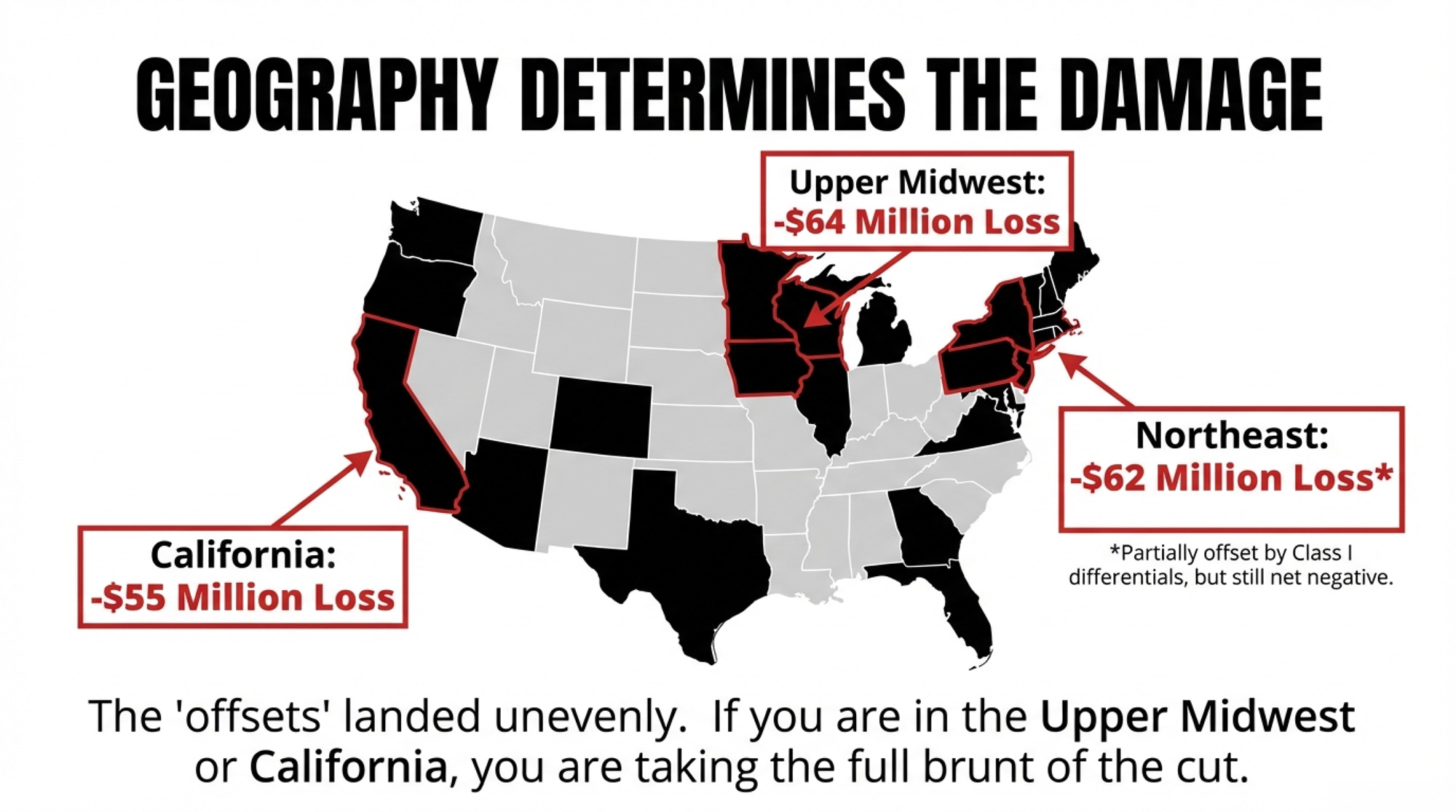

AFBF economist Danny Munch tracked what those increases did to pool values. Average Class I prices dropped $0.89/cwt. Class II fell $0.85. Class III lost $0.92. Class IV, $0.85 — a 4 to 5% cut across the board attributable solely to higher make allowances. The Upper Midwest order alone lost $64 million in pool value over those first three months. The Northeast lost $62 million. California, $55 million.

The FMMO amendments weren’t all one-directional, though. Higher Class I differentials — also part of the modernization package — added an estimated $137 million back to pool values in the same period, led by the Northeast (+$34 million) and Mideast (+$30 million), per the same AFBF analysis. The net total pool revenue decline from all FMMO amendments combined was roughly $232 million. But the offsets landed unevenly: California and the Upper Midwest — the two hardest-hit orders from make allowances — gained only $6 to $8 million each from higher differentials. If you’re pooled in the Upper Midwest, the differential cushion barely registers.

Processors had their own math. Christian Edmiston, VP of Procurement at Land O’Lakes, testified at the 2023 FMMO hearing that make allowances hadn’t been updated since 2008 and that manufacturing costs at LOL’s plants had risen substantially. He acknowledged the proposed increases “would not fully offset the increases in manufacturing costs” since 2008, but argued they “offer a balance between the producer price impact from raising make allowances and the processor cost impact.”

University of Minnesota dairy economist Marin Bozic told Brownfield in January 2025 that he expects higher allowances will eventually pull more milk back into pools: “As make allowances increase, that means that the processors have stronger incentives to bring that milk to the pool to try to get a piece of the producer price differential and forward that to their patrons.”

The short version of Bozic’s argument: when regulated minimum prices don’t reflect real processor economics, processors pull their milk out of the pool. Under the old make allowances, the regulated Class III price didn’t reflect where the market actually was, as Bozic put it — the gap between minimum regulated prices and processors’ real-world economics was wide enough to distort pooling behavior. That squeezed processor margins within the pool and pushed them to de-pool. Bozic told Brownfield the old system “manifested as a declining and then disappearing premium and more and more milk being depooled.” With higher make allowances, regulated minimums drop closer to market reality, reducing the misalignment that triggers de-pooling. More pooled milk means more revenue stays in the pool — and Bozic expects over-order premiums to return as a result. But “eventually” doesn’t help the check that’s already been issued.

[Read more: We mapped where those pool dollars went, region by region]

How Does the 2026 Farm Bill Change Your DMC Payment?

The barn math on the make allowance side is straightforward. Take a 200-cow Holstein herd producing 24,000 pounds per cow annually:

- 200 cows × 24,000 lb = 4,800,000 lb/year = 48,000 cwt

- AFBF’s class price reductions range from $0.85 to $0.92/cwt, depending on class utilization

- Using $0.88 as an approximate midpoint: 48,000 × $0.88 = $42,240 per year

Scale it up. At 500 cows: $105,600. At 1,000 cows: $211,200. Your actual number depends on your order’s class utilization — a herd pooled mostly in Class III (Upper Midwest) takes a hit closer to $0.92/cwt, while heavier Class I utilization lands nearer $0.89. And if you’re in an order with strong differential gains (Northeast, Mideast), part of that loss is offset by higher Class I values — pull your actual milk statements to see the net.

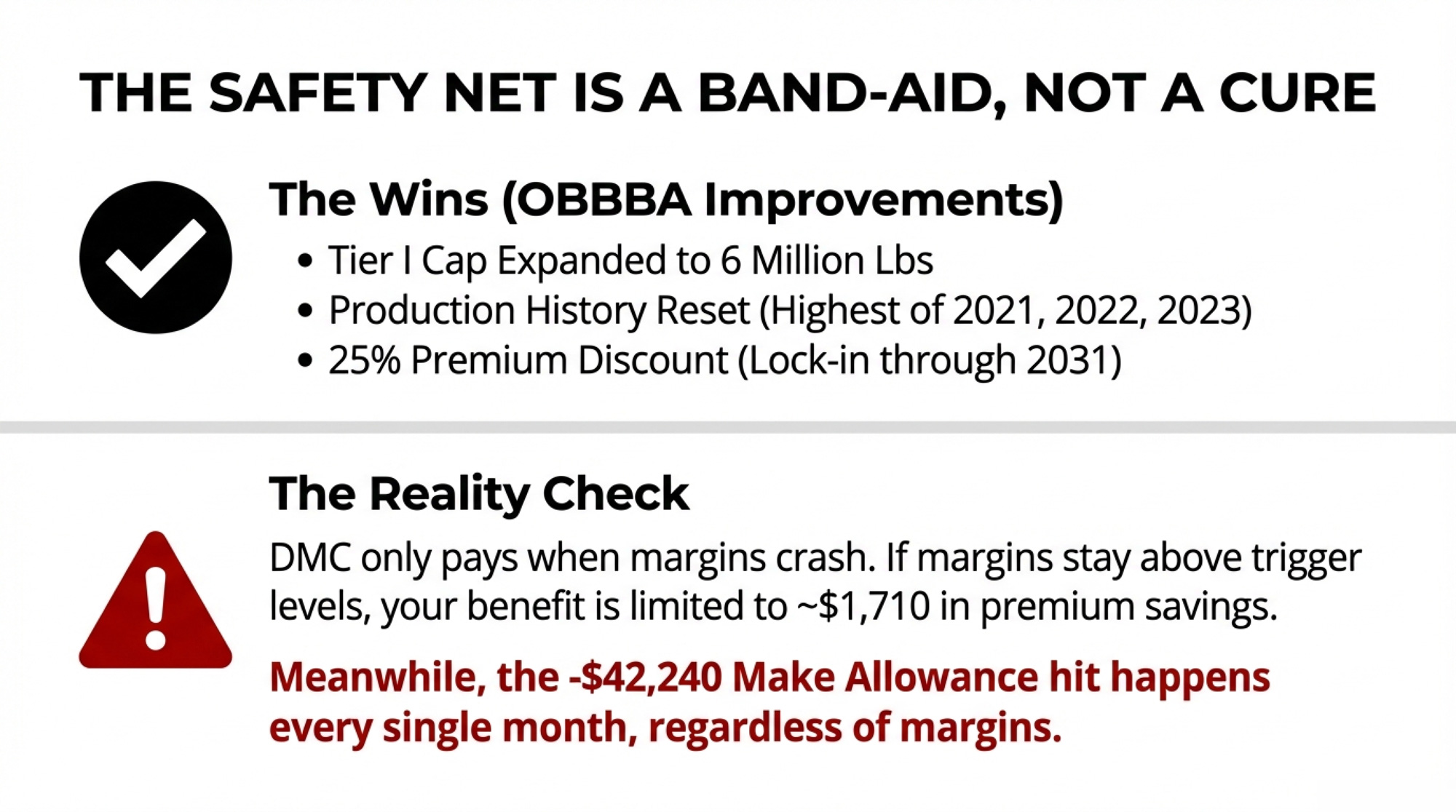

Now the safety-net side. The One Big Beautiful Bill Act (OBBBA) — the 2025 budget reconciliation package signed into law July 4, 2025 — delivered genuine DMC improvements: Tier I expanded from 5 million to 6 million pounds, production history resets to the highest of 2021, 2022, or 2023 marketings, and a 25% premium discount kicks in for producers who lock coverage through 2031. Premium rates under both Tier I and Tier II are unchanged from the 2018 Farm Bill structure.

Run it for the same 200-cow herd at $9.50 Tier I coverage, 95% enrollment:

- 4,800,000 lb × 0.95 = 4,560,000 lb covered = 45,600 cwt

- Premium at $0.15/cwt = $6,840/year at full rate

- With 25% lock-in discount: $5,130/year — saving roughly $1,710 annually

- In a year where DMC triggers for three to six months, additional indemnity payments could add $600 to $1,600

Total realistic DMC benefit in a tight-margin year: approximately $1,800 to $3,000. Against $42,240 in structural pool losses, that recovers between 4 and 7 cents per dollar.

The Quick Math for a 200-Cow Herd:

- Loss (Make Allowances): −$42,240/year

- Gain (DMC Fixes): +$1,800 to $3,000/year

- Net Structural Gap: −$39,240 to −$40,440

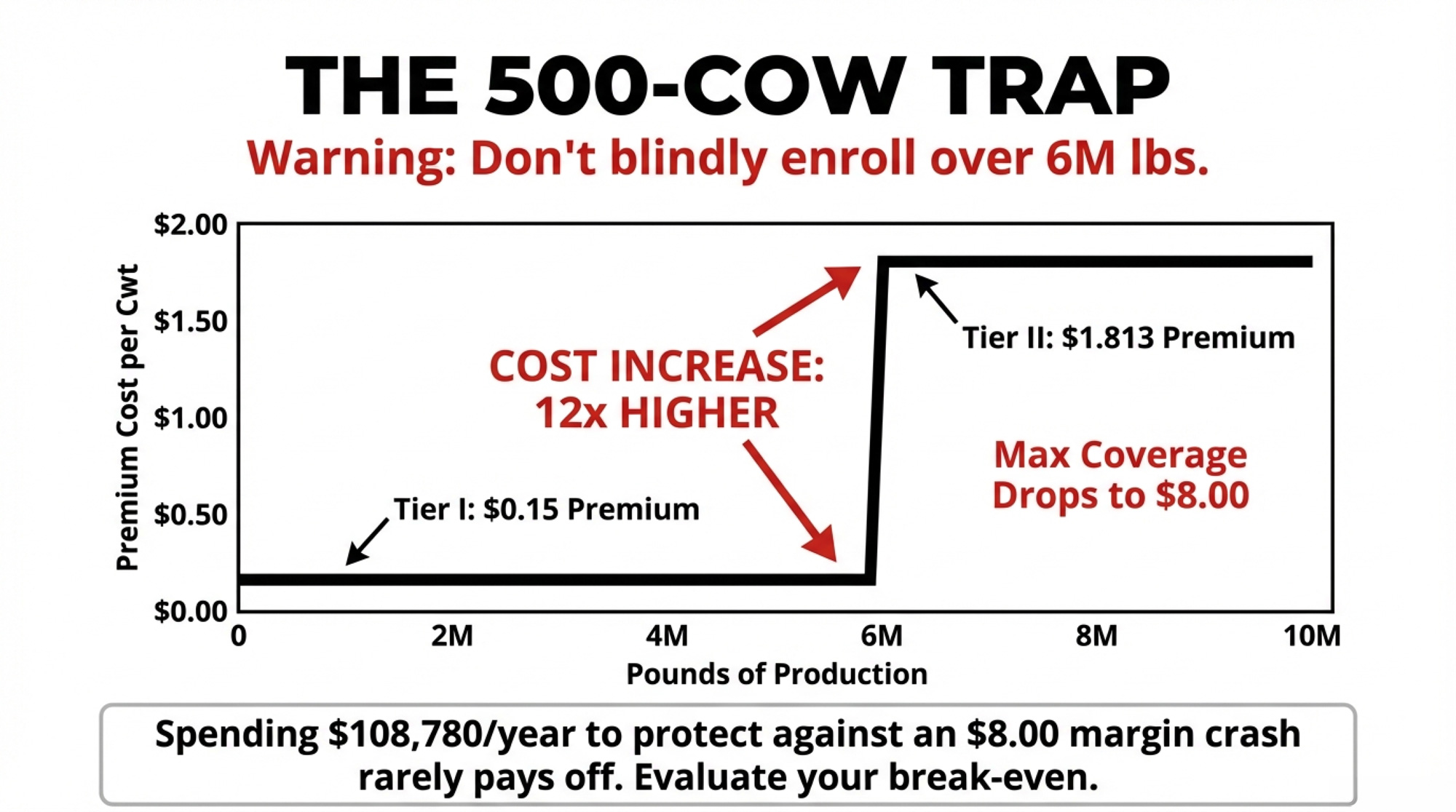

The 500-Cow Tier II Trap

Bigger herds hit a wall. At 500 cows producing 24,000 lb/cow, you’re generating 12 million pounds a year. Under the new Tier I cap, the first 6 million pounds qualifies for Tier I. The remaining 6 million drops into Tier II — and the economics shift sharply:

- Tier I (first 6 million lb): Max coverage = $9.50/cwt. Premium at $9.50 = $0.15/cwt.

- Tier II (remaining 6 million lb): Max coverage drops to $8.00/cwt. Premium at $8.00 = $1.813/cwt — a 12x increase for $1.50 less protection.

- Tier II annual premium math: 6,000,000 lb ÷ 100 = 60,000 cwt × $1.813 = $108,780/year at the $8.00 ceiling.

- And here’s what you’d get back: If the margin drops to $7.00 for three months, Tier II indemnity on 60,000 cwt = $1.00 × 60,000 × 3/12 = $15,000 — against $108,780 in annual premium.

- Meanwhile, the make allowance hit on 500 cows: $105,600/year, and that lands regardless of your DMC election.

Most large-herd advisors, including Mike North at Ever.ag, counsel producers to carefully evaluate Tier II against the frequency with which margins actually fall below $8.00. If your breakeven sits well above $9.00, Tier II may not be worth the premium.

| Coverage Tier | Coverage Ceiling | Annual Premium | Indemnity (3 mo @ $7.00) | Net Cost | Worth It? |

|---|---|---|---|---|---|

| Tier I (first 6M lb) | $9.50/cwt | $9,000 | $37,500 | +$28,500 | Yes |

| Tier II (next 6M lb) | $8.00/cwt | $108,780 | $15,000 | -$93,780 | Rarely |

| Tier I + Tier II combined | Mixed | $117,780 | $52,500 | -$65,280 | No |

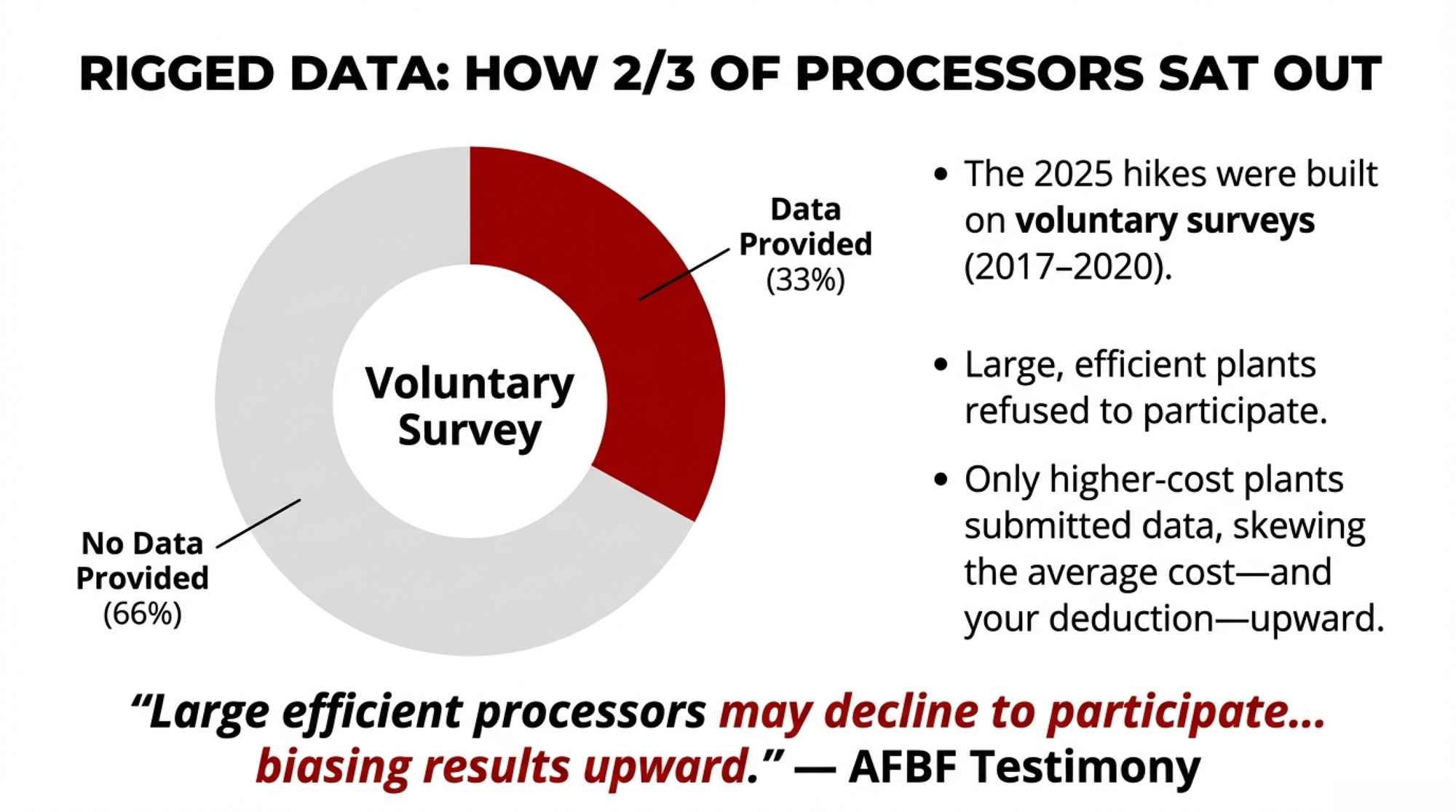

How Two-Thirds of Processors Sat Out and Shaped Your Check

Munch has been sounding this alarm for two years. When Brownfield covered AFBF’s concerns at World Dairy Expo in October 2024, he laid out the numbers: “76% of cheddar cheese plants, 80% of butter plants, 40% of nonfat dry milk plants” skipped the voluntary cost surveys entirely. The cheese survey covered about 43 million pounds in total, but Stephenson’s sample captured only 6 to 7 million. The joint AFBF/NMPF petition to USDA put an even finer point on it: roughly two-thirds of dairy manufacturing plants provided no cost data at all.

| Product Type | Participation Rate (%) |

|---|---|

| Cheese | 24% |

| Butter | 20% |

| Nonfat Dry Milk | 60% |

| Dry Whey | ~30% |

The survey, conducted by University of Wisconsin economist Mark Stephenson, gathered data from October 2017 through December 2020. So the make allowance increases, hitting your 2025 checks, were built on cost data that’s largely 5 to 8 years old, from a voluntary sample that skewed toward higher-cost operations.

The structural incentive isn’t subtle. Plants that benefit from higher make allowances were the same ones deciding whether to supply cost data. Big, modern facilities running at scale — with the lowest per-unit costs — had every reason to sit out. As AFBF wrote in its hearing testimony: “large efficient processors may decline to participate, which would bias the cost survey results upward.” Even Edmiston at Land O’Lakes acknowledged in his testimony that “the ideal data that a mandatory and audited survey would provide does not exist today.”

And there’s a historical pattern here. Allowances have been raised twice in the modern FMMO era — once in 2008 and again in 2025 — since the current formula structure was established during the 2000 order consolidation. They’ve never been reduced. The ratchet turns one direction.

[Read more: The U.S./Canada dairy comparison that puts domestic pricing reform in a continental context]

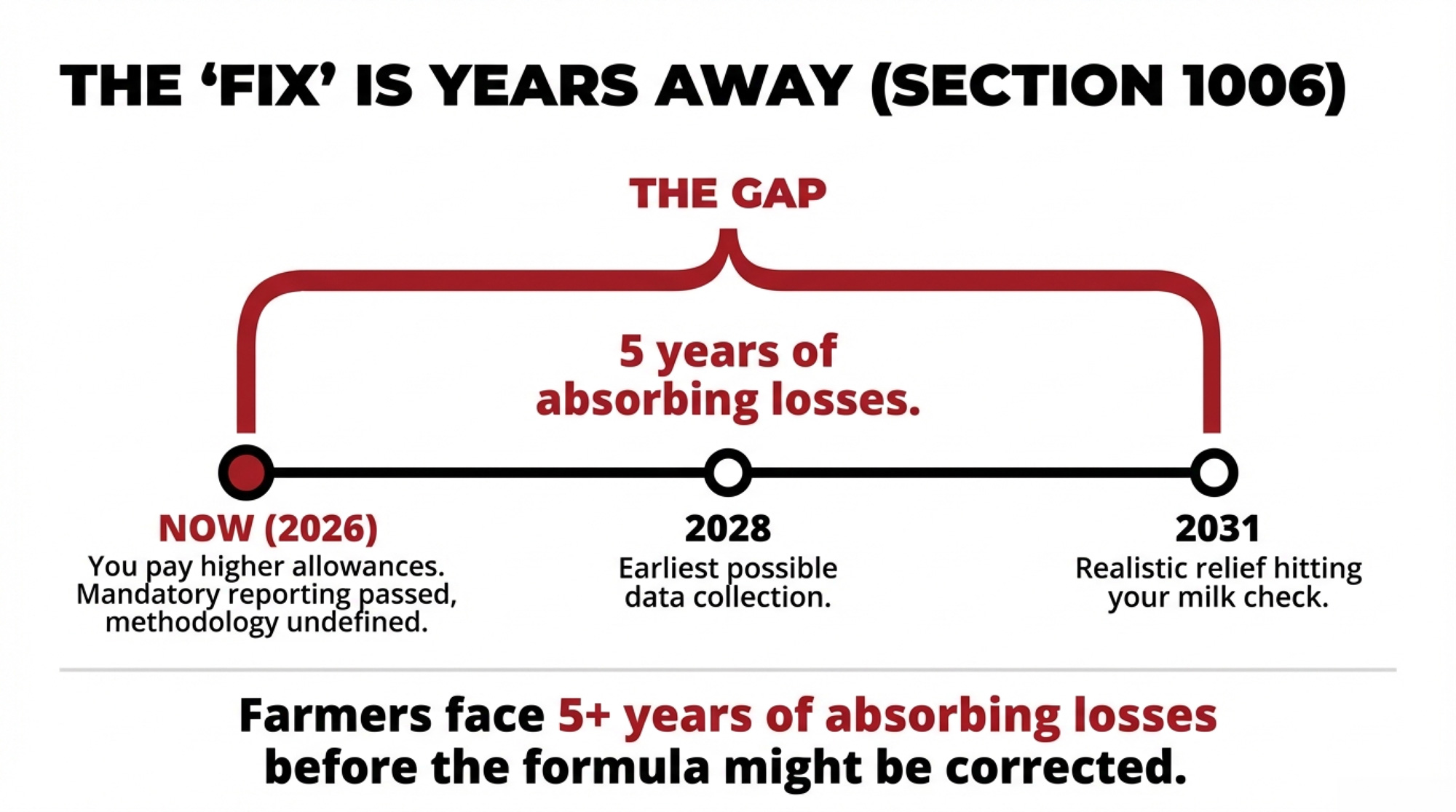

Will Section 1006 Actually Change Anything?

Here’s where it gets interesting. Section 1006 of the Farm, Food, and National Security Act of 2026 — titled “Mandatory reporting of dairy product processing costs” in the bill’s table of contents — makes permanent the mandatory biennial cost surveys initially authorized and funded at $9 million in the OBBBA (the 2025 reconciliation package).

NMPF President Gregg Doud said it plainly in the organization’s February 13, 2026, statement: “NMPF thanks Chairman Thompson, House Agriculture Committee members, and their staffs for working to put together a farm bill that will bring greater certainty to producers at a difficult time.” IDFA’s Michael Dykes called it “a permanent authorization for Mandatory Cost Surveys that will ensure make allowances in the Federal Milk Marketing Orders accurately reflect the cost of manufacturing dairy products.”

Kevin Krentz, Wisconsin Farm Bureau president and owner of a 600-cow dairy near Berlin, Wisconsin, has been a consistent voice for this reform — testifying at the 2023 FMMO hearing and at Farm Bill listening sessions that make allowance changes need mandatory, verifiable data behind them.

Lesher has walked that same path. She testified before the House Ag Committee and told Lancaster Farming that she received more questions from representatives than from the economists and professors in the room. “If I don’t tell our story,” Lesher said, “somebody else is going to tell a story. And it may not be as accurate.”

But Section 1006 doesn’t automatically adjust make allowances when new data arrives. Munch told Brownfield in October 2025 — after the OBBBA passed — that this is a common misconception: “That’s not the case. There’s still the traditional federal milk marketing order hearing process in place to make those amendments, so we would have to have a dairy industry stakeholder claim that there’s a problem, mention that problem, and initiate a whole other hearing.” And even getting the surveys running is on hold. “They’re going to have to set up a methodology. They’re going to have to have staff and researchers set aside for this,” Munch said, adding that government shutdowns have already caused delays.

There’s also a scenario nobody’s talking about. Mandatory surveys could confirm that processor costs genuinely rose as much as the voluntary data suggested. Edmiston’s own testimony showed that Land O’Lakes’ manufacturing costs at their Tulare, Carlisle, and Kiel plants all increased since 2008. If mandatory data backs that up, the reform argument shifts from “lower make allowances” to “at least now we know.” Either way, verified data beats unaudited self-reporting from one-third of plants.

Munch has been clear on the timeline: “any resulting formula adjustments remains unclear, with changes unlikely to reach milk checks before 2028.” That’s Munch’s floor. A more conservative read based on the full FMMO hearing track record: AMS builds survey methodology through 2027–2028, first mandatory report around 2029, then add two to three years if stakeholders petition for an adjustment. Possible relief in the 2031–2032 range.

Five to six years of absorbing $42,240 annually on a 200-cow herd before make allowances might come down. “Might” is doing heavy lifting.

[Read more: When the financial pressure is structural, not cyclical, the playbook has to change]

What Canadian Producers Should Watch

Bullvine readers north of the border: this isn’t just an American story. When U.S. FMMO pool prices drop structurally — not due to a bad market but to a formula change — it depresses the price at which American dairy enters the USMCA tariff-rate quota system. Lower U.S. pool prices mean American milk crosses into the TRQ window at a wider discount relative to Canadian cost-of-production pricing, shifting the competitive dynamics Canadian producers face under supply management. And there’s a sharper edge: if Section 1006 ultimately fails to lower make allowances, sustained U.S. price depression could widen the gap between what American and Canadian producers receive for comparable components — a gap that already sparks political friction on both sides of the border.

If you’re tracking your quota value against cross-border pricing, this formula change affects the spread. We’ll break down the Canadian math when the Senate version drops.

[Read more: We compared what’s happening to U.S. farms vs. Canadian quota holders]

Four Moves Before Markup

Chairman Thompson confirmed the House Ag Committee will begin markup the week of February 23. Here’s what you can do between now and then.

This month:

- Lock in your 2026 DMC coverage by February 26. That’s the enrollment deadline. At $9.50 Tier I with the 25% six-year discount, a 200-cow herd pays ~$5,130 vs. ~$6,840 at the full rate. The trade-off: you’re committed through 2031. If margins run strong over those six years, you can’t adjust coverage until the next cycle. Here’s the threshold: if your margin has dropped below $9.50 in any month since June 2025, the $9.50 level is likely worth the premium. If it hasn’t, model the savings at $8.50 and $9.00 coverage before locking into $9.50 through 2031 — the premium savings at lower levels may outweigh the indemnity probability over a six-year window.

- Call your representative with two specific asks on Section 1006. First, compress the timeline for the first mandatory cost report—if AMS already audits prices weekly under NDPSR, cost data shouldn’t take years to collect. Second: add explicit penalties for non-compliance. Roughly two-thirds of plants sat out the voluntary surveys. Mandatory only works with teeth. Thompson’s DC office: (202) 225-5121.

Within 90 days:

- Calculate your make allowance exposure. Pull your milk statements from April–May 2025 (pre-FMMO change) and compare blended price per cwt to July–September 2025 (post-change). Your annual hundredweight × that difference = your structural loss from the formula shift, separate from any market-driven movement. That number strengthens every conversation with your lender, your co-op board rep, and your congressman.

- Check EQIP eligibility if you’re planning capex. USDA removed EQIP payment limits for 2025 — the previous $450,000 five-year cap is gone. The Farm Bill draft supports conservation “with a continued designation of conservation funds for livestock producers and a directive for states to prioritize methane-reducing practices,” per NMPF’s analysis. With no cap, larger manure-handling or precision-feeding projects now qualify. But EQIP is competitive — uncapped funding attracts bigger operations too — and most state batching deadlines fall in March through April. Contact your local NRCS office this week if you want to be in the spring cycle.

Within 12 months:

- Watch for AMS’s announcement of the mandatory cost survey methodology. Once AMS publishes how they’ll collect data under Section 1006, the clock starts on when new make allowance data could inform a hearing. That announcement is your signal for whether the 2028 floor or the 2031 ceiling is more realistic.

| Action | Deadline | Urgency | What to Do | Why It Matters |

|---|---|---|---|---|

| Enroll in DMC | Feb 26, 2026 | HIGH | Lock $9.50 Tier I with 25% 6-year discount; model Tier II carefully | $1,710/year savings on 200-cow herd; production history reset to highest of 2021–2023 |

| Call your rep on Section 1006 | Feb 23, 2026 (before markup) | HIGH | Ask for faster reporting timeline + penalties for non-compliance | Mandatory surveys are only mechanism to lower make allowances; voluntary surveys had 2/3 non-response |

| Calculate your exposure | Within 90 days | MEDIUM | Compare April–May 2025 vs. July–Sept 2025 milk statements | Separates formula loss from market loss; strengthens lender/co-op conversations |

| Check EQIP eligibility | March–April 2026 (state batching deadlines) | MEDIUM | Contact NRCS for methane/manure projects; no payment cap | Uncapped funding but competitive; larger projects now qualify |

| Watch for AMS methodology announcement | Within 12 months | LOW | Monitor when AMS publishes Section 1006 survey design | Signals whether 2028 floor or 2031 ceiling is realistic for relief |

When the financial pressure is this structural — baked into the formula, not driven by the market — the hardest call isn’t to your congressman. [If you or someone on your operation is feeling the weight of it, read this.]

[Read more: How your balance sheet tells the story before your milk check does]

What This Means for Your Operation

- The make allowance hit is permanent and automatic. It lands on every hundredweight of pooled milk, every month, regardless of your DMC enrollment or conservation participation. You don’t choose this deduction. It’s already in the formula.

- The offset is real but uneven. Higher Class I differentials added $137 million to pool values nationwide — but the gains concentrated in the Northeast and the Mideast. If you’re in the Upper Midwest or California, the differential cushion covers a fraction of your make allowance loss.

- DMC improvements are conditional. You only see indemnity payments when the margin drops below your coverage level. In a year where DMC never triggers, the benefit is limited to the premium discount — about $1,710 for a 200-cow herd at $9.50 Tier I with the six-year lock-in.

- If your operation crosses 250 cows, you’re now likely within Tier I under the expanded 6-million-pound cap. Run your numbers at Tier I rates before assuming you need Tier II — the premium jump from $0.15/cwt to $1.813/cwt on production above 6 million pounds is steep, the coverage ceiling drops from $9.50 to $8.00, and the indemnity math rarely justifies the premium.

- Section 1006 is the only mechanism in this bill that could eventually reduce make allowances. But the FMMO hearing process has never produced a downward adjustment. The regulatory timeline suggests 2031–2032 at best. Necessary, not sufficient.

- Bozic’s pooling argument is worth watching. If higher make allowances genuinely pull more milk back into pools — by reducing the price misalignment that incentivizes processors to de-pool — that could partially offset class price reductions through restored over-order premiums. “Partially” is the key word, and the offset depends on your region’s pooling dynamics.

- The gap frames your advocacy. For every $1 the safety net returns, the formula deducts roughly $14 to $23 from the same check, depending on whether DMC triggers and how often it does so. That imbalance doesn’t change until mandatory cost data forces a reckoning.

Key Takeaways

- Enroll in DMC before February 26 — the production history reset and higher Tier I cap may change your optimal coverage level. Don’t default to last year’s election.

- Calculate your per-cwt make allowance exposure by comparing pre-June and post-June 2025 blended prices on your actual milk statements. That’s your starting point for every financial conversation this year.

- Contact your House rep before the February 23 markup with specific asks on Section 1006: a faster reporting timeline and enforcement penalties for non-participating plants.

- If you milk 500+ cows, model the Tier I/Tier II split carefully before locking in coverage. The expanded 6-million-pound Tier I cap helps mid-size operations, but the Tier II premium and coverage ceiling haven’t changed—and the $8.00 Tier II indemnity-to-premium ratio is brutal.

The Bottom Line

Pull your April 2025 and September 2025 milk statements. Look at the blended price. That gap isn’t all market. A meaningful piece of it is structural — baked into a formula built on voluntary data from roughly one-third of plants, through make allowances that have never been adjusted downward. Section 1006 gives producers like Lesher — who expanded her herd, built a farm market, and testified before Congress — the first real tool to challenge that pattern with mandatory data instead of hunches. Whether it works depends on what happens between now and markup, and whether enough dairy farmers make the call.

When the committee marks this up, we’ll re-run every number. Bookmark this page.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- The $0.90/cwt FMMO Hit: Reset Your Breakeven, DMC Coverage, and Heifer Strategy for 2026 – Reveals the immediate tactical roadmap for neutralizing formula-driven losses by auditing your herd’s component potential and locking in 2026 DMC tiers before the February 26 deadline, protecting your operational liquidity in a structural squeeze.

- The Triple Cushion Trap: Why 2025’s Strong Margins Won’t Save You in 2026 – Exposes the long-term risk of relying on beef-on-dairy premiums and temporary feed lows, arming you with a strategic framework to reposition your balance sheet before the inevitable 2026 margin compression erases six figures in equity.

- Genetic Revolution: How Record-Breaking Milk Components Are Reshaping Dairy’s Future – Breaks downhow the April 2025 genetic reset and new Lifetime Cheese Merit $ (CM$) indices enable you to outrun regulatory deductions by breeding high-protein “future-proof” cows that thrive in a processor-dominated, high-capacity market.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.