Cull cow: $2,000. Daily milk profit: $2. You’re not failing – you’ve been lied to about what survival actually requires.

EXECUTIVE SUMMARY: The management myth just died. USDA’s October 2025 data confirms what the numbers have been screaming: your location now determines your profitability more than your skills ever will. Cull cows are fetching $2,000 as beef while daily milk margins scrape by at $2-3 per cow—and the smart money has noticed. Federal Milk Marketing Order data shows cheese-oriented regions pulling $1.00-1.50/cwt more than powder areas, handing some operations a $50,000+ annual advantage their neighbors can’t touch, no matter how hard they work. The heifer shortage—at 1970s lows—has flipped from crisis to cash flow, with producers breeding surplus heifers now banking $100,000+ annually. Billions in new processor investments are creating what analysts call “permanent regional stratification,” and lenders are already tightening credit windows. Strategic repositioning isn’t a five-year plan anymore—it’s a five-month decision. October’s culling data proves the reshuffling has already begun, and the producers who act now will be the ones still standing when the dust settles.

The USDA’s October 2025 Milk Production report confirms what we’ve all been feeling in our gut: The national herd is shrinking, but you know what? The reasons have fundamentally changed. This isn’t just about milk prices anymore—we’re watching a restructuring that’s making everything we thought we knew about good management seem… well, less relevant than it used to be.

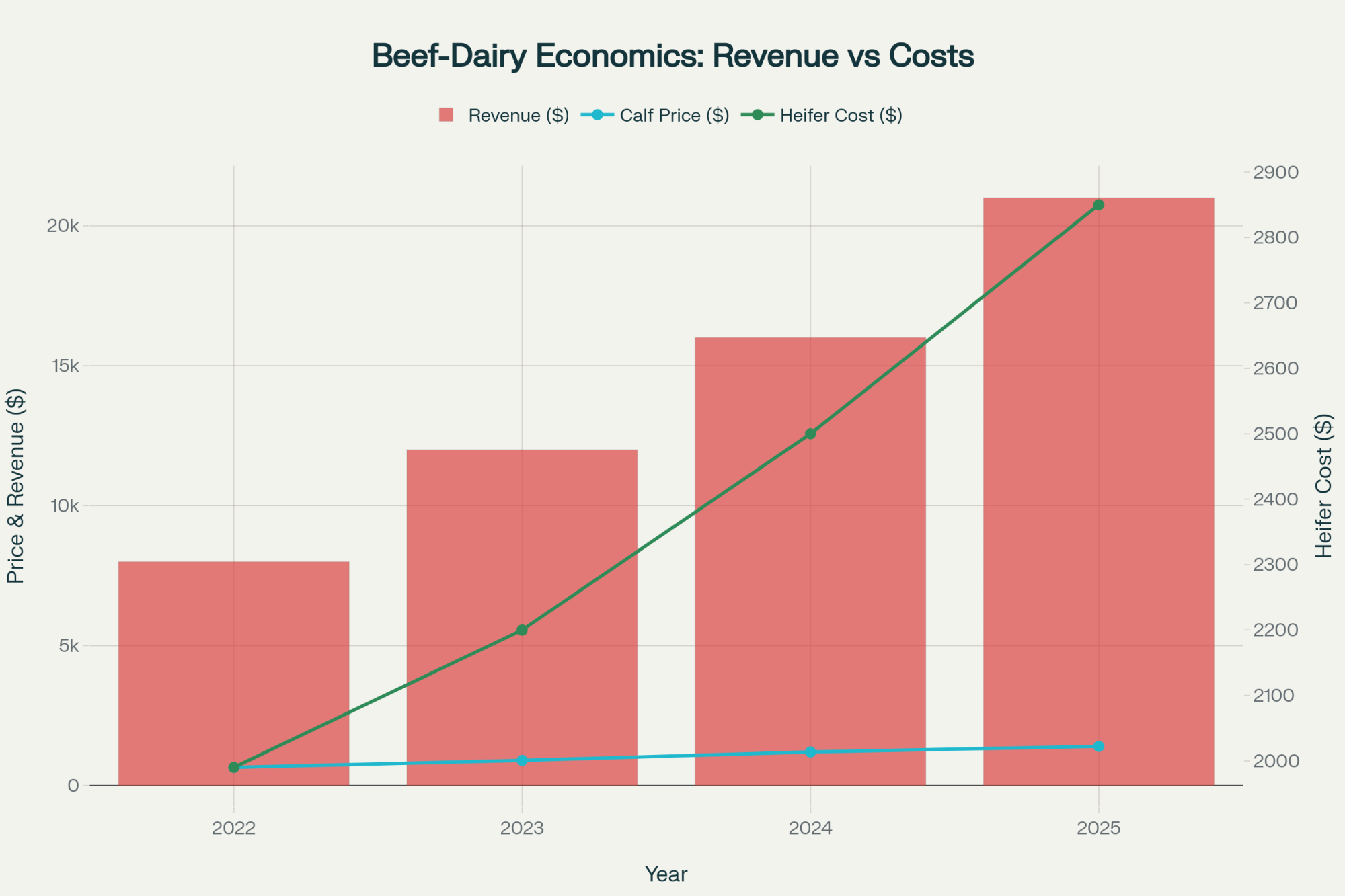

Here’s the math we’re all looking at. October’s Class III milk was hovering in the mid-$16s per hundredweight, according to CME Group’s daily settlement data. Take your typical cow producing around 65 pounds daily—she’s bringing in maybe $11 in gross revenue. Feed costs? Using the USDA Farm Service Agency’s Dairy Margin Coverage calculations from October, we’re looking at roughly $8 to $9 daily per cow. That doesn’t leave much after labor, utilities, and keeping the lights on…

Meanwhile—and here’s what has everyone talking over morning coffee—that same cow is worth close to $2,000 as beef. USDA’s Agricultural Marketing Service weekly reports show cull cows bringing $1.60 to $1.70 per pound in some regions. A decent 1,200-pound cow? Do the math.

As one Extension economist down in Mississippi who tracks livestock markets put it to me, “When you’re looking at these beef prices, producers are asking themselves some pretty rational questions.”

But this goes deeper than just comparing milk checks to beef prices, doesn’t it? What October’s really showing us is the start of something bigger—where geography, genetics, and who you’re shipping to will matter more than ever. Management excellence? I hate to say it, but it’s becoming less relevant in the face of structural disadvantages.

The New Revenue Stream: Breeding for the Market, Not Just the Milking String

Here’s something clever that’s changing the entire breeding game—and I think more of us need to be talking about this. If you breed 20-25% more heifers than you need for replacements and sell the extras at these premium prices… well, as many of us have figured out, a 600-cow herd selling 30 surplus heifers at around $3,500 each? That’s roughly $100,000 in additional annual revenue. We’re talking about turning what most see as a constraint into a profit center.

USDA’s January 2025 Cattle inventory report shows dairy heifer numbers at historically low levels—we haven’t seen this level since the late ’70s. All those years of breeding for beef-on-dairy when milk prices were tough? Well, now we’re seeing the consequences—or maybe the opportunities.

Recent auction reports from key dairy states show good springers regularly trading above $3,000 per head, with top groups occasionally pushing past $4,000 per head. I spoke with an extension specialist at the University of Florida who’s been tracking this closely. “The consistency of these high prices,” he said, “that’s what’s remarkable. We’re not seeing the usual seasonal dips.”

A lending specialist at CoBank pointed out something fascinating—and think about this—the shortage that prevents you from expanding also prevents your competition from growing. Operations that might have expanded to grab market share? They simply can’t get the heifers at prices that make sense. It’s creating this forced discipline in the market that we haven’t seen before.

Smart producers are figuring out different ways to optimize. Can’t solve problems through expansion anymore—that playbook’s out the window. Instead, you’ve got to improve within your existing footprint. Genetic selection becomes crucial when you can’t add cows. I’m seeing more genomic testing than ever before.

I recently heard from a 480-cow operation in central Wisconsin that made the switch to component-based optimization last spring. They’re seeing an extra $3,800 monthly just from butterfat premiums alone, even with slightly lower volume. “We’re producing less milk but making more money,” the owner told me. “That’s not something I thought I’d ever say.”

How Geography Trumps Management

You know, the old wisdom was that efficient operations outlast downturns. We’ve all believed that, right? But what I’m seeing now challenges that thinking in ways most of us haven’t fully grasped yet.

Federal Milk Marketing Order data from October 2025 shows some cheese-oriented regions getting roughly $1.00 to $1.50 more per hundredweight than powder-oriented areas. Think about that for a minute—if you’re running a thousand cows, that gap could mean $50,000 or more annually. That’s not something you can just manage your way around, no matter how good you are at what you do.

And the driver behind these gaps? It’s these massive processor investments we’re seeing. The International Dairy Foods Association’s October 2025 capital investment tracking report shows billions in new and expanded dairy processing projects—dozens of facilities either under construction or recently announced across multiple states through the rest of this decade.

The concentration is what gets me. Texas is seeing major cheese facilities go in, including that big Leprino project near Lubbock everyone’s talking about. New York’s seeing major expansions in yogurt and premium milk. Idaho’s getting more cheese capacity around Twin Falls with Glanbia’s expansion. Wisconsin continues to add to its cheese infrastructure, with multiple expansion projects underway. Even the California Central Valley, despite its challenges, is seeing selective investment in specialized products.

What dairy economists at universities like Cornell and Wisconsin are telling me is this creates something like “permanent regional advantage.” Makes sense when you think about it. If you’re near these new cheese plants, you’re capturing premiums. If you’re shipping to butter and powder? Those challenges compound every month.

The producers in growth states—places like Idaho and Texas, where this new capacity promises good premiums—they culled selectively in October to upgrade genetics. Smart move.

But in other regions? Southwest dairy operations dealing with water restrictions, or Southeast producers managing not just heat stress but increasingly volatile feed costs and limited local grain production—that culling represented something different. Those folks are reducing exposure to what’s becoming a tougher competitive environment.

Building Your Bridge Through What’s Coming

For operations trying to navigate current challenges while positioning for better times, I’ve been collecting strategies from extension folks and producers who are making it work. From Southeast dairy operations dealing with heat stress and feed availability challenges to Upper Midwest producers managing seasonal variations, to California Central Valley farms wrestling with water costs.

First thing—and this is crucial—you need to understand your true economics beyond just that all-milk price everyone talks about. Several dairy economists at land-grant universities keep emphasizing this, and they’re right. With current component premiums, if you’re optimizing for volume rather than components, you could be leaving tens of thousands annually on the table, even for a modest-sized herd.

Component optimization matters more than ever. With butterfat premiums running anywhere from 50 cents to over a dollar per hundredweight above base in some areas—especially Upper Midwest operations shipping to cheese plants—if you’re still focusing on volume over components, you’re leaving serious money on the table.

Here’s what’s gaining traction based on my conversations:

You need to secure working capital lines now, while your operation still looks stable to lenders. Several ag lenders, including Farm Credit Services and regional banks, are telling me they expect to become more cautious about new working capital over the next year or so. Some are even talking about focusing more on financing acquisitions and restructurings if margins stay tight. That window? It’s narrowing faster than most folks realize.

The Dairy Margin Coverage program makes sense, too. According to the USDA’s Risk Management Agency, October 2025 updates, depending on your coverage level and production history, premiums often run from a few dimes to maybe 70 cents per hundredweight. But that cash flow protection when margins get really tight? Could make all the difference between weathering the storm and… well, not.

And here’s something livestock economists at universities like Kentucky and Kansas State are watching—CME feeder cattle futures have pulled back sharply since mid-October. Producers who locked in their beef-on-dairy calf values earlier are feeling pretty good right now. Consider hedging at least half your production to protect what’s become crucial revenue.

What’s interesting is that the operations doing these things aren’t expecting prosperity if milk prices drop to the $14-16 range that the USDA’s World Agricultural Supply and Demand Estimates suggest for next year. They’re building resilience to stay independent through what could be a tough stretch before things improve.

The Technology Factor and Labor Reality

The technology piece matters here too—and it’s changing the labor equation dramatically. Robotic milking systems, which can cost $150,000-250,000 per stall, are becoming more feasible for larger operations that can spread those fixed costs.

But here’s what’s interesting: these systems aren’t just about milking efficiency. They’re addressing the chronic labor shortage that’s hitting dairy farms nationwide.

One Pennsylvania producer running four robots told me, “We went from needing six milkers to basically one herd manager. In a market where finding reliable labor costs $18-22 per hour plus benefits, that math changes everything.”

For mid-sized farms, though, the capital requirements are creating another pressure point that’s accelerating consolidation decisions. And for those sub-300 cow operations? The technology investment rarely pencils out unless you’re adding significant value through on-farm processing or direct marketing.

Why Processors Keep Building While We’re Struggling

This apparent contradiction—processors pouring billions into new capacity while we’re dealing with tight margins—it makes more sense when you look at the longer game they’re playing.

Several outlooks from groups like Rabobank’s Q3 2025 Global Dairy Quarterly point to some interesting dynamics. The International Dairy Federation’s World Dairy Situation report is talking about potential gaps between global supply and demand later in the decade if trends continue.

Recent trade data from USDA’s Foreign Agricultural Service shows Chinese imports of cheese and whole milk powder running well ahead of year-ago levels. Countries like Indonesia are expanding school milk programs that could add meaningful demand over the coming years. And with EU production constrained by environmental regulations, the U.S. is positioned well as a growth supplier.

Gregg Doud, who served as U.S. chief agricultural trade negotiator and now works with Aimpoint Research, explained it well at the recent World Dairy Expo: “Processors aren’t building for today’s prices. They’re looking at where they think we’ll be in 2028, 2030. The current downturn? It actually helps their positioning by limiting competitive expansion.”

What’s less visible—and this is based on industry analysis from groups like CoBank and what I’m hearing through the grapevine—is that a large share of new processing capacity appears to be already tied up in multi-year arrangements with larger farms. Contracts negotiated when prices were recovering in ’23 and ’24, locking in supply regardless of current spot conditions. It’s creating this two-tier market that not everyone fully grasps yet.

The Information Gap That’s Hurting Smaller Operations

One challenge I keep hearing about from mid-sized operations is what university economists call “information asymmetry.” Basically, larger farms dealing directly with processors often see market shifts months before that information reaches smaller producers through traditional channels.

This gap shows up in several ways. Larger operations often have earlier visibility into processor needs and plans. They might subscribe to proprietary research from firms like Terrain or StoneX, which costs tens of thousands of dollars annually. Meanwhile, smaller operations rely on cooperative communications that, honestly, can lag market realities by quite a bit.

A Pennsylvania producer managing 600 cows—a fifth-generation dairy farmer—put it to me straight: “We thought October’s price drop was temporary. We didn’t realize how much had already been decided about where the industry’s headed. By the time we understood, our lender was already getting cautious about new credit.”

The practical impact? By the time many producers recognize these fundamental shifts, the window for smart positioning has already narrowed considerably.

Regional Winners and What’s Creating Lasting Advantages

The geographic distribution of new processing investment is creating what analysts at CoBank call “permanent regional stratification.” Strong words, but they’re not wrong.

Looking at Federal Milk Marketing Order data from October 2025 and processor announcements, here’s who’s seeing sustained advantages:

Idaho’s Magic Valley continues to benefit from expansions in cheese infrastructure. USDA National Agricultural Statistics Service data shows Idaho among the fastest-growing milk states, with many operations reporting solid annual gains. The Texas Panhandle’s seeing competitive pricing from multiple cheese plants.

Kansas—and this surprised me—has emerged as a real growth story, with some of the strongest percentage gains in the country according to USDA data. Central New York’s premium milk and yogurt facilities are creating genuine competition for local supplies.

But then you’ve got regions facing structural challenges. The Pacific Northwest remains primarily powder-oriented with limited cheese processing. California’s Central Valley operations are dealing with both water costs and a commodity-focused product mix that limit pricing upside.

Southwest dairy producers face increasing water restrictions and rising costs for heat-stress management. Southeast operations are wrestling with not just heat stress but also limited local feed production and basis challenges that add $30-40 per ton to feed costs. The Upper Northeast faces geographic isolation that creates significant transportation penalties that can substantially erode margins.

The hard truth? And this is tough for many of us to accept—operational excellence can’t overcome a structural pricing gap of $1 or more per hundredweight by geography. That recognition is driving some of October’s herd adjustments.

Practical Steps Depending on Your Situation

Based on what’s emerging from October’s data and conversations with folks making it work, here’s what I’m seeing:

If You’re in a Growth Region:

Focus on genetic improvement within your existing herd rather than expansion. A Texas producer near one of the new cheese plants told me, “We’re genomic testing everything and being selective like never before.”

Work on developing direct processor relationships where possible. Several Idaho producers tell me they’re having success negotiating directly rather than relying only on their co-op. And consider partnerships with neighboring operations—achieve some scale advantages without individual expansion.

If You’re in a Challenged Region:

You need an honest evaluation of your long-term position given structural disadvantages. Run scenarios at different milk prices—$14, $16, $18—to really understand your breakevens. It’s sobering but necessary.

Look at diversification that reduces dependence on commodity pricing. I know Northeast producers are finding success with on-farm processing, agritourism—not for everyone, but worth considering. California Central Valley operations are exploring specialty milk products that command premiums despite the region’s challenges.

For those sub-300 cow operations, the math gets even tougher. But I’m seeing some find success through direct marketing, value-added products, or transitioning to organic, where premiums can offset scale disadvantages. Others are forming producer groups to share resources and negotiate collectively.

And assess whether relocating might work, though as one Wisconsin friend said, “The math on moving with current land and heifer prices? Brutal.”

Universal Strategies That Work:

Secure financial flexibility now while credit’s available. Every lender I’ve talked to expects standards to tighten over the next year.

Implement component-focused production aligned with how your processor actually pays. This means regular ration work, good DHI records.

And develop non-milk revenue streams. Despite some recent softening, beef-on-dairy remains profitable according to cattle market folks at the Chicago Mercantile Exchange. Every bit helps.

The Consolidation Already Underway

Let’s be honest about what’s happening here. Consolidation isn’t some future possibility—it’s here, right now. USDA’s 2022 Census of Agriculture shows dairy farm numbers in the mid-30,000s, and USDA Economic Research Service economists expect that to continue declining as the industry consolidates.

What’s driving this? ERS research consistently shows larger herds tend to have lower costs per hundredweight than smaller ones—often by several percentage points. Processors prefer fewer, larger suppliers to reduce complexity.

Technology adoption, especially robotic milking systems that can run $150,000-250,000 per stall, requires capital that favors bigger operations. The labor savings alone—reducing milking staff by 60-80% while addressing the chronic shortage of qualified dairy workers—makes automation almost mandatory for operations planning to survive long-term.

And the heifer shortage prevents smaller operations from achieving competitive scale, even if they wanted to.

Rather than viewing consolidation as failure—and this is important—many are recognizing it as evolution. As one university dairy economist at Wisconsin explained, “Operations that position strategically, whether through improvements, repositioning, or thoughtful exit timing, preserve more value than those forced into decisions.”

The Bottom Line

Several outlooks, including the Food and Agricultural Policy Research Institute’s baseline projections, suggest better price prospects later in the decade if global demand continues growing and herd size stays in check—though these are projections, not guarantees, as we all know.

Factors that could support recovery: The heifer shortage physically constrains expansion for a while. Global demand appears to be growing faster than supply, according to FAO data. Environmental regulations limit expansion in some major producing regions. And all this new processing capacity will need higher milk prices to generate returns.

But—and this matters—recovery probably won’t benefit everyone equally. Operations with secured processor relationships, geographic advantages, and superior genetics will likely capture premiums. Others might find that even recovered prices don’t fully offset their structural disadvantages.

What October’s Really Telling Us

After looking at the data and talking with folks across the industry, several lessons emerge pretty clearly.

Geography increasingly determines destiny. Those regional pricing gaps reflect structural realities that great management can’t overcome. If you’re in a disadvantaged region, that needs to factor into your planning—like it or not.

The heifer shortage creates both constraint and opportunity. Operations that optimize within their existing footprint while potentially monetizing excess production can turn the shortage to their advantage. Creative producers are making this work.

Information and relationships matter more than ever. Direct processor relationships and access to good market intelligence increasingly separate operations that thrive from those that struggle. Better information pays—literally.

Financial positioning can’t wait. Every lender emphasizes this—the window for securing working capital and risk management tools is months, not years. Wait until you need flexibility, and it might not be there.

Strategic positioning beats stubborn persistence. Whether improving for independence, positioning for acquisition on good terms, or planning an orderly exit, proactive decisions preserve more value than reactive ones. There’s no shame in strategic repositioning—it’s smart business.

We’ve weathered dramatic transitions before—from diversified farms to specialized operations, through technological changes and trade upheavals. This is another transition. What’s different is both the speed and the degree to which these advantages are becoming structural. Operations that recognize and adapt, rather than hope for a return to old patterns, are best positioned.

October’s strategic culling by forward-thinking producers shows something important: successful operations aren’t waiting for change to happen to them. They’re actively positioning for whatever comes next.

For those still evaluating, October’s message seems clear—the time for strategic decisions is now, while you’ve got options and can preserve value through thoughtful positioning.

The path forward won’t be identical for everyone—and that’s fine. But understanding the forces reshaping our industry helps inform decisions. In a world where change keeps accelerating, maybe the biggest risk is standing still.

For more specific information on programs mentioned, producers can check with their local USDA Service Center, university extension offices, or agricultural lenders.

KEY TAKEAWAYS

- Your zip code now outweighs your work ethic: Cheese regions earn $1.00-1.50/cwt more than powder areas—that’s $50,000+ annually, no amount of great management will ever close

- The heifer shortage is now your profit center: Breeding 20-25% surplus heifers generates $100,000+ annually while locking competitors out of expansion at today’s prices

- Your lender’s flexibility has an expiration date: Working capital windows slam shut by mid-2026—secure financing now, not when you desperately need it

- This is a five-month decision, not a five-year plan: October’s culling data proves the reshuffling has begun—producers positioning now will be the ones still milking in 2027

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

- The 90-Day Dairy Pivot: Converting Beef Windfalls into Next Year’s Survival – Reveals a specific 90-day financial blueprint for reinvesting short-term beef premiums into long-term efficiency upgrades, helping producers secure working capital before lender windows tighten in 2026.

- The Rules Changed and Nobody Told You: Three Paths Left for the 300-Cow Dairy – Analyzes the three remaining viable business models for mid-sized herds and provides a strategic framework for deciding between scaling up, specializing, or executing a high-equity exit.

- The Holstein Genetics War: What Every Producer Needs to Know About the Battle for Our Breed’s Future – Demonstrates how to use advanced genomic testing to precisely identify the bottom 20% of your herd for beef-on-dairy programs, maximizing the surplus heifer revenue stream mentioned in this article.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.