62% of Americans now prefer cheese to chocolate for Valentine’s. The $6.7B question: does any of that reach your milk check?

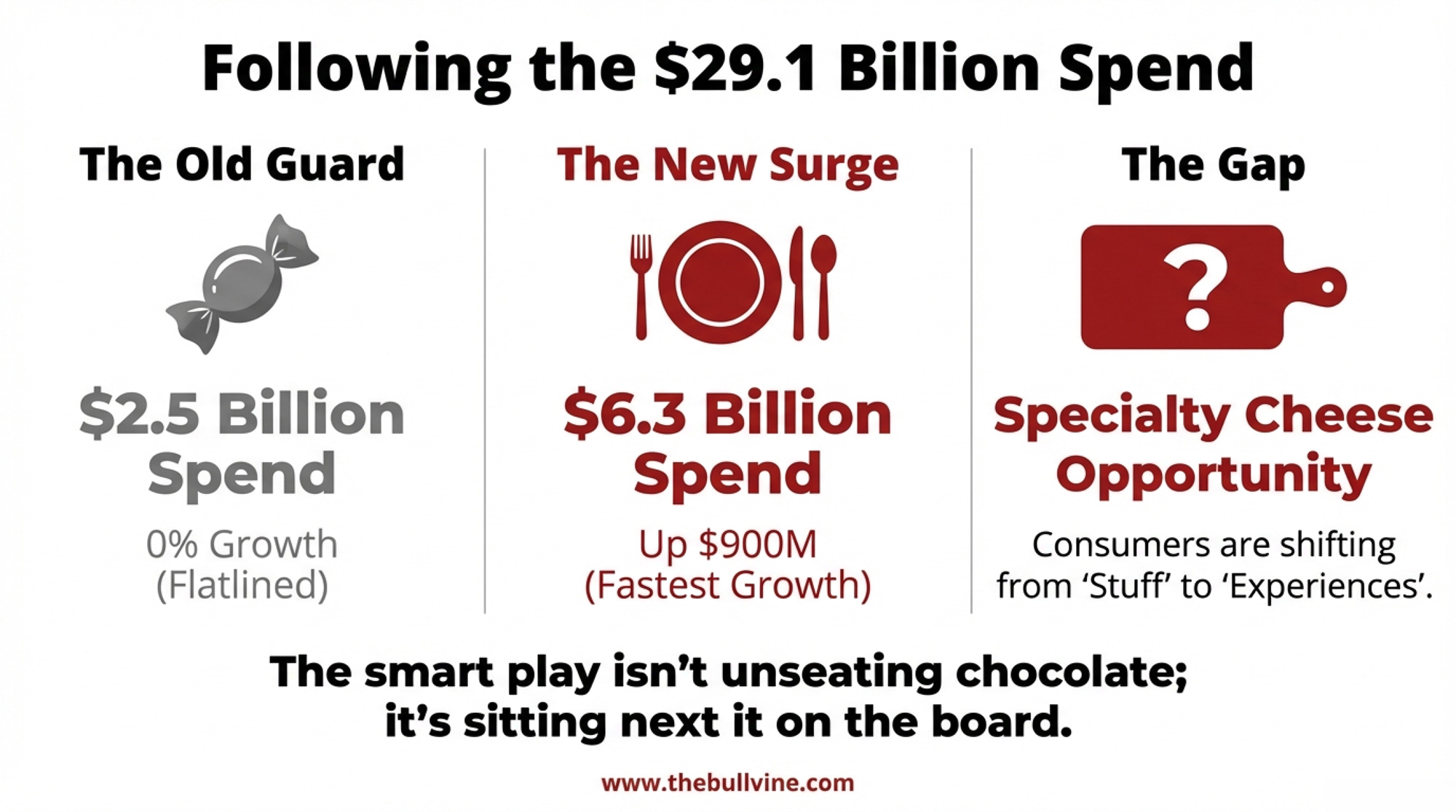

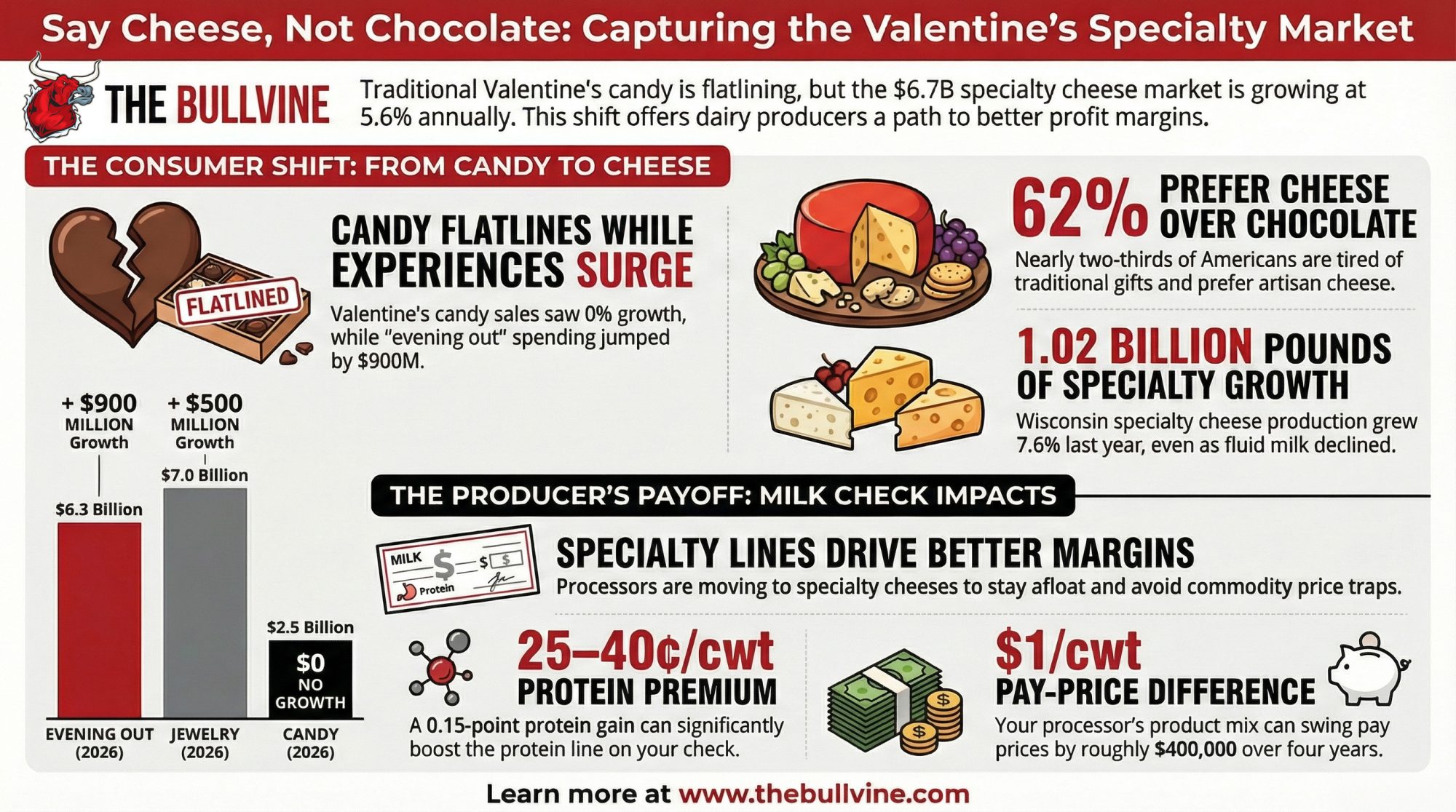

Executive Summary: Americans are on track to spend a record $29.1 billion on Valentine’s Day in 2026, but candy — at $2.5 billion — is the only major category that hasn’t grown at all. A Wakefield Research survey for Wisconsin Cheese shows 62% of Americans are tired of traditional gifts and 64% would trade roses for wedges of artisan cheese, while the US specialty cheese market has climbed to $6.67 billion and is growing 5.6% a year. Wisconsin now produces 1.02 billion pounds of specialty cheese — 53% of the US total — and is testing the Valentine’s opportunity with farmstead boards from Crave Brothers and a $100 Wedges of Love bouquet from Wisconsin Cheese. The catch is that processors like Klondike openly admit that specialty cheese keeps their business afloat, yet there’s no clean public data showing how much of that premium flows back as component bonuses on your milk check. Bullvine’s own component grid math shows a 0.15-point protein gain can add 25–40¢/cwt, and processor product mix can swing pay price by about $1/cwt over time. This feature walks through the numbers, the farmstead vs. coalition paths, and the seasonal risk so you can decide if and where Valentine’s specialty cheese fits in your own herd strategy.

Americans are spending a record $29.1 billion on Valentine’s Day this year — $199.78 per celebrating shopper — according to the National Retail Federation and Prosper Insights & Analytics annual survey of 7,791 adult consumers conducted January 2–8, 2026. That’s up from $27.5 billion in 2025, which itself broke the previous record of $27.4 billion set in 2020. And for the first time, there’s hard consumer data suggesting specialty cheese wants a piece of that.

A Wakefield Research poll of 1,000 nationally representative US adults, conducted December 12–16, 2025 — commissioned by Wisconsin Cheese, the promotional arm of Dairy Farmers of Wisconsin — found that 62% of Americans are tired of traditional Valentine’s gifts like chocolates, flowers, and teddy bears. Sixty-six percent said cheese is their “love language.” Sixty-four percent would trade a dozen roses for a dozen wedges. The methodology is credible. The sponsorship still matters. But those numbers are hard to ignore.

The US specialty cheese market hit $6.67 billion in 2024, according to Grand View Research, and is projected to reach $9.2 billion by 2030 at a 5.6% compound annual growth rate. Flavored cheese is the fastest-expanding segment. Meanwhile, total US fluid milk sales barely ticked up 0.5% in 2024 — the first increase since 2009, per USDA Agricultural Marketing Service data — and that growth came almost entirely from whole milk (up 1.6%), organic (up nearly 7%), and value-added products like fairlife, not traditional skim and reduced-fat, which continued to decline.

Where the $29.1 Billion Goes

| Category | 2025 ($B) | 2026 ($B) | Change |

|---|---|---|---|

| Jewelry | $6.5 | $7.0 | +$0.5B |

| Evening Out | $5.4 | $6.3 | +$0.9B |

| Clothing | $3.2 | $3.5 | +$0.3B |

| Flowers | $2.9 | $3.1 | +$0.2B |

| Candy | $2.5 | $2.5 | $0.0B |

Not all Valentine’s dollars matter equally for dairy. Here’s where NRF says the money landed in 2026, with 2025 comparisons:

- 💍 Jewelry: $7.0 billion, up from $6.5B in 2025 (25% of shoppers, up from 22%)

- 🍽️ Evening Out: $6.3 billion, up from $5.4B in 2025 (39% of shoppers, up from 35% — the fastest-growing category, jumping $900 million in a single year)

- 👗 Clothing: $3.5 billion

- 🌹 Flowers: $3.1 billion, up from $2.9B in 2025 (41% of shoppers, up from 40%)

- 🍫 Candy: $2.5 billion both years (56% participation — the only major category with zero growth)

- 🧀 Specialty Cheese: No Valentine’s-specific figure exists yet — that’s the opportunity gap. The US market is growing at 5.6% annually.

The story is clear. Candy flat-lined. Experience spending surged. That $900 million jump in “evening out” tells you consumers are spending more on shared experiences — and cheese boards positioned as a date-night-at-home experience tap directly into that shift.

Two Wisconsin Plays Worth Watching

Play #1: The Farmstead Coalition Board

Crave Brothers Farmstead Cheese, based in Waterloo, Wisconsin, launched a “Better Together” Valentine’s campaign in late January — four curated cheese boards, each matched to a relationship stage. “These boards highlight how local cheeses can be the centerpiece of any celebration, while supporting the farmers and producers behind them,” Roseanne Crave, the family’s sales and marketing manager, told Perishable News.

The boards feature products from at least nine other Wisconsin makers: Sartori, Carr Valley, Widmer’s, Henning, Marieke, Ellsworth Cooperative Creamery, Buholzer Brothers, Renard’s, and Pine River. That’s coalition marketing — pooling reach instead of one brand shouldering the cost. The Crave family farms 2,500 acres in south-central Wisconsin, running a herd of over 2,000 Holsteins with a biodigester for energy and water recycling across the operation. Their cheeses are farmstead — the milk comes from their own cows. To celebrate the month of love, they’re also donating 5% of all proceeds from their online store during February to the American Heart Association.

Play #2: The $100 Cheese Bouquet

Dairy Farmers of Wisconsin went bigger. On National Cheese Lovers Day (January 20), Wisconsin Cheese launched Wedges of Love — a bouquet-style gift box featuring nine award-winning artisan cheeses arranged like a floral bouquet. Retail price: $100 with free overnight shipping. It includes four stainless steel knives, a personalized poem, and pairing guides.

The lineup: Carr Valley Cranberry Chipotle Cheddar, Deer Creek Carawaybou, Hoard’s Dairyman Farm Creamery Belaire, Landmark Creamery Tallgrass Reserve, Marieke Fenugreek Gouda, Roelli Cheese Haus Dunbarton Blue, Roth Grand Cru Reserve, Sartori SarVecchio, and Uplands Cheese Company Pleasant Ridge Reserve. Limited drops sold on January 20, January 27, and February 3. Demand was strong enough that Parade ran a story headlined “It’s Almost Sold Out.”

“The Wedges of Love box provides a delectable glimpse, showcasing a variety of tastes and styles from farmstead producers and cheesemakers of all sizes,” said Suzanne Fanning, chief marketing officer for Wisconsin Cheese.

Here’s what connects both plays to the broader supply chain: Wisconsin produced a record 1.02 billion pounds of specialty cheese in 2024 — up 7.6% from 2023 — according to the USDA’s National Agricultural Statistics Service. That’s 28.3% of the state’s total cheese output of 3.59 billion pounds, and more than 53% of all specialty cheese produced in the United States. Ninety-three of Wisconsin’s 116 cheese plants manufactured at least one specialty variety. Production has increased twelvefold since the USDA started collecting data in 1993.

The Honest Scale Problem

Let’s be direct about the gap. Valentine’s candy flat-lined at $2.5 billion. A $100 cheese bouquet and a set of board recipes aren’t competing at that scale. Not yet.

But specialty cheese has a structural tailwind that fluid milk doesn’t. A 5.6% CAGR doesn’t sound dramatic until you stack it against fluid milk’s 13-year decline. Reduced-fat milk dropped another 4.4% in 2024. Meanwhile, Wisconsin specialty cheese output grew 7.6% in a single year. The premium and commodity ends of dairy are diverging, and Valentine’s Day is one of the clearest seasonal moments to capture premium demand.

The smart play isn’t to unseat chocolate. It’s to sit beside it on the board and quietly capture more of the basket every February.

Does Any of This Reach Your Milk Check?

Here’s the question every producer reading this is actually asking.

The answer starts at the processor level, and it’s blunt. “The whole reason we went into specialty cheeses is because they do have better profit margins, so we can keep the business afloat,” Luke Buholzer, vice president of sales at Klondike Cheese Company, told Wisconsin Watch in October 2025. Klondike produced about 38 million pounds of cheese last year — nearly double their output from a decade ago — and every pound is specialty. They phased out commodity cheeses entirely.

John Lucey, director of the Wisconsin Center for Dairy Research at UW-Madison, told Cheese Market News the shift was driven from the plant floor up: “Cheesemakers at smaller plants started to become more flexible, entrepreneurial, and willing to take on some risk. They got fed up with the low cheese prices and trying to compete with commodity plants.”

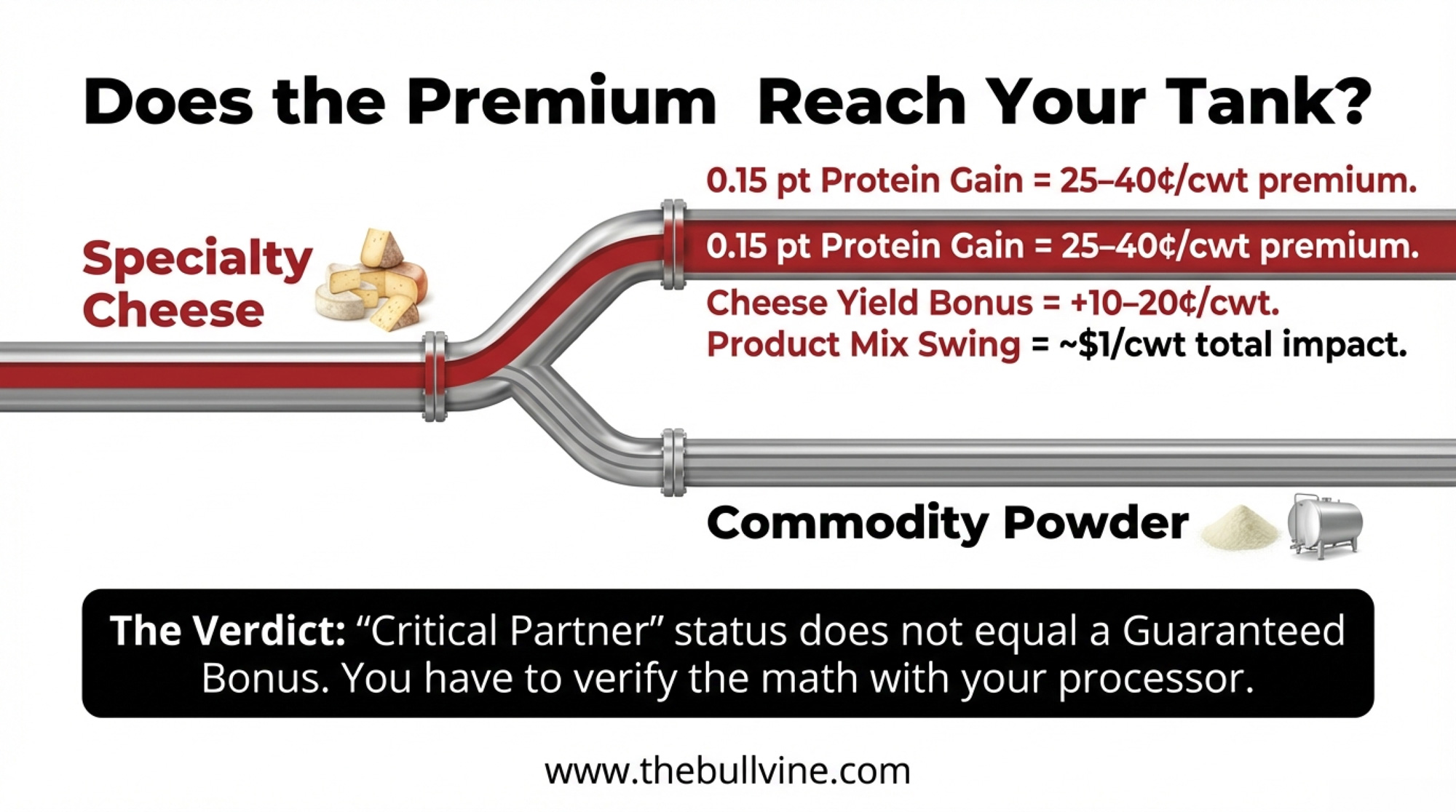

That margin advantage at the processor level is real. But how much flows back to your bulk tank? That’s where the data gets thin. No public source we found connects specialty cheese market growth directly to measurable premium increases for individual farms.

Here’s what we do know. On a typical Upper Midwest Class III–based component grid, a 0.15-point protein gain can be worth 25–40¢/cwt on the protein line alone, with cheese yield bonuses adding another 10–20¢/cwt. And as we’ve covered before, where your processor sends your milk — pizza cheese and specialty yogurt versus commodity powder and private-label fluid — can mean a steady $1/cwt pay-price difference, worth roughly $400,000 in equity over four years for a 400-cow herd. Specialty cheese growth widens that gap.

| Scenario | Component/Product Mix Impact | Premium (¢/cwt) | Annual Impact* | 4-Year Equity Gain |

|---|---|---|---|---|

| Baseline | Standard components, commodity channel | $0.00 | $0 | $0 |

| Protein Gain | +0.15 protein points (3.15% → 3.30%) | +25–40¢ | $27,375–$43,800 | $109,500–$175,200 |

| Product Mix | Milk allocated to specialty cheese vs. powder | +$1.00 | $109,500 | $438,000 |

| Combined | Protein gain + specialty channel access | +$1.25–$1.40 | $136,875–$153,300 | $547,500–$613,200 |

Chad Vincent, CEO of Dairy Farmers of Wisconsin, framed the farmer’s stake this way in a December 2025 piece for Professional Dairy Producers of Wisconsin: “Your milk is the foundation for innovation far beyond the vat. As processors continue to explore new uses for dairy byproducts, farms supplying consistently high-quality milk will remain critical partners.”

That’s the right direction. But “critical partners” and “a line item on your milk check” aren’t the same thing. If your milk ships to a plant with an artisan line and your components are strong, bring one question to your next field-rep visit: What butterfat and protein specs does your specialty cheese require, and does meeting them earn me a premium? If they can’t answer, the answer is probably no. And that’s worth knowing.

Farmstead vs. Coalition: Two Ways In

If you’re evaluating how to connect your operation to this channel, there are two models on the table:

| Farmstead Path (Crave Brothers model) | Coalition Marketing Path (Wedges of Love model) | |

| Investment | $218,500–$553,000 startup (general industry estimates, BusinessPlanKit.com, March 2025 — not a university source; UW-Madison’s Center for Dairy Research may have region-specific benchmarks); equipment is 40–50% of total | Marketing contribution only — split across partners |

| Timeline | 12–24 months to first product; years to brand recognition | Can launch a seasonal campaign in weeks if the cheese already exists |

| Control | Full — you own the product, the brand, and the margin | Shared — you’re one cheese among many |

| Risk | High licensing, cold chain, seasonal inventory if Valentine’s demand disappoints | Low to moderate — reputational risk if the campaign flops, but no capital at stake |

| Margin | Highest per unit — farmstead commands premium retail pricing | Moderate — depends on wholesale terms with the promotional partner |

| Best fit | Operations already exploring DTC or on-farm processing | Any producer whose milk goes into cheese that could be part of a curated offering |

Neither path is right for every operation. For many dairy farms, the honest answer is that neither applies today. That’s fine. But if 7.6% annual growth in Wisconsin specialty production continues to compound, the channel will need more milk. Knowing where you sit when that call comes is worth something.

What This Means for Your Operation

Ask your processor one question. Does your plant have a specialty or artisan cheese line—and does seasonal Valentine’s demand create any pull on component volumes or pricing? Wisconsin specialty cheese output hit a record 1.02 billion pounds in 2024, up 7.6% year-over-year. Somebody is capturing that margin.

If you’re farmstead-curious, Valentine’s is a natural first test. One limited-edition SKU — heart-shaped, gift-boxed, paired with a local chocolatier — before committing to year-round production. But know the capital: $218,500–$553,000 for a small-scale cheese operation. Run the numbers before the dream.

Think experience, not commodity. The $199.78-per-shopper Valentine’s budget isn’t going toward a random wedge in the dairy case. Wisconsin Cheese proved there’s a $100 price point that moves for a curated box with the right packaging and story.

Don’t fight chocolate — partner with it. Crave Brothers’ Chocolate Mascarpone is the template. Their “Udderly in Love” gift box pairs it with Heart-Shaped Mozzarella and custom Valentine’s cow portraits. Become chocolate’s co-star, not its replacement.

Coalition marketing lowers the barrier. Both Wisconsin campaigns feature products from multiple cheesemakers — 10 in Crave Brothers’ campaign and 9 in the Wedges of Love bouquet. Pooling spend builds a category story bigger than one brand can tell alone.

Watch the experience-spending surge. “Evening out” jumped from 35% to 39% — and from $5.4 billion to $6.3 billion — in a single year. That $900 million increase is the largest dollar jump of any Valentine’s category. At-home food experiences are reshaping how consumers spend on dairy.

Be honest about the seasonal risk. Valentine’s is a one-week window. For farmstead operations, gearing production to that spike means holding inventory that may not move if demand disappoints. Coalition marketing avoids this — the cheese already exists; you’re just merchandising it differently.

A Note for Canadian Readers

Most of the market data in this piece is US-specific, and supply management changes the economics of specialty cheese north of the border. But the channel isn’t closed. Dairy Farmers of Ontario has operated an Artisan Cheese Programsince April 2006, setting aside 3 million litres designated as “Artisan Cheese Milk” — available to qualifying new processors at up to 300,000 litres per applicant annually. The program covers small-batch, hand-produced specialty cheeses (excluding cheddar and mozzarella) and operates alongside the Canadian Dairy Commission’s Domestic Dairy Product Innovation Program. If you’re a Canadian producer interested in the specialty channel, these programs are worth understanding — the demand trends are crossing the border, even if the supply structure doesn’t.

Key Takeaways

- 62% of Americans are tired of traditional Valentine’s gifts, and 64% would trade roses for cheese wedges (Wakefield Research for Wisconsin Cheese, 1,000 US adults, Dec 2025). Consumer pull backed by credible methodology — from a survey commissioned by the state’s cheese promotional organization.

- Wisconsin produced a record 1.02 billion pounds of specialty cheese in 2024, up 7.6% from 2023, accounting for 53% of all US specialty cheese (USDA NASS). That growth — in an industry where fluid milk declined for 13 straight years — tells you where the premium is heading.

- Valentine’s spending hit $29.1 billion in 2026, up from $27.5 billion in 2025 (NRF). Candy was the only major category with zero-dollar growth ($2.5B in both years). “Evening out” surged to $900 million, bringing the total to $6.3 billion. Experience spending is climbing. Boxed-gift spending isn’t.

- Two Wisconsin operations proved the Valentine’s model. Crave Brothers built a farmstead coalition board with nine partner cheesemakers and tied it to an American Heart Association donation. Wisconsin Cheese’s $100 Wedges of Love bouquet drew enough demand across three limited drops to near sell-out. Different models. Both replicable.

- The farm-level bridge is real but incomplete. Specialty cheese processors are clear about why they’re there — better margins. A 0.15-point protein gain can be worth 25–40¢/cwt on Class III grids, and where your milk lands in the value chain can mean a $1/cwt difference. But whether Valentine’s-specific demand moves your check depends on your processor relationship. Ask the question.

The Bottom Line

Your best move this Valentine’s Day is to make sure that when someone spends $199.78 on the person they love, cheese shows up alongside the truffles—not as an afterthought in the grocery cart. The Crave family and Wisconsin Cheese already made that bet. What’s your operation’s play?

Editor’s Note: Valentine’s spending data comes from the National Retail Federation and Prosper Insights & Analytics (7,791 adult consumers, Jan 2–8, 2026; and 8,020 adult consumers, Jan 2–7, 2025). Consumer sentiment on cheese gifting comes from Wakefield Research, commissioned by Wisconsin Cheese / Dairy Farmers of Wisconsin (1,000 nationally representative US adults, Dec 12–16, 2025). Specialty cheese market figures are from Grand View Research (2024 base year, US scope). Wisconsin specialty cheese production data are from USDA NASS as reported by Cheese Reporter (June 2025) and Wisconsin Watch (Oct 2025). Wisconsin industry quotes are from Wisconsin Watch (Oct 9, 2025) and Professional Dairy Producers of Wisconsin (Dec 2025). Fluid milk trends are from USDA AMS data as reported by High Ground Dairy (Feb 2025). Premium component data are from The Bullvine’s analyses in “The Protein Premium” (Jan 2026) and “Same Milk, Different Payday” (Jan 2026). Startup cost ranges are general industry estimates from BusinessPlanKit.com and may vary by region, scale, and regulatory environment. Canadian program details are from Dairy Farmers of Ontario. We welcome producer feedback and case studies for future coverage.

Learn More

- $19.14 Costs vs. $18.95 Milk: Is Your Barn Tech Paying the Difference? – Stop bleeding margin on Monday by auditing the 90% of your existing tech you aren’t using. This 30-day “tech tune-up” reveals how integrating current herd software and activity collars claws back $20,000–$45,000 in immediate health-related savings.

- More Milk, Fewer Farms, $250K at Risk: The 2026 Numbers Every Dairy Needs to Run – Exposes the brutal math of the $250,000 margin gap facing mid-size dairies in 2026. This strategic analysis arms you with the cost-per-hundredweight benchmarks needed to decide if your operation should grow, hold, or exit before the market chooses.

- PDO cheese premiums – Delivers the “Jasper Hill” blueprint for achieving a 2.23x milk price multiplier through collective regional branding. This disruptor report breaks down the capital required to exit the commodity race and secure $50+/cwt premiums through organized, PDO-style consortiums.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.