Canadian dairy farmers achieve 10,400 kg milk yields with 0.191 debt ratios while “free market” systems require $33B bailouts. Time to rethink everything?

What if everything the dairy industry believes about free markets is actually subsidized fiction? While economists preach the gospel of deregulation and “competitive markets,” Canadian dairy farmers are achieving something that exposes the entire free-market narrative as carefully constructed theater. According to the USDA’s 2025 Farm Sector Income Forecast, U.S. dairy operations are projected to receive massive government support, while Canadian supply-managed farmers saw their cash receipts increase by 3.9% for unprocessed milk in 2024, with projections for another 3.0% growth in 2025, without a single bailout dollar.

Here’s the uncomfortable truth that free market advocates desperately want buried: Canada’s supposedly “outdated” supply management system is quietly delivering everything economists promised deregulation would provide—and doing it better than every single subsidized “free market” dairy system on the planet.

Think of it this way: if your nutritionist promised a balanced ration but delivered 40% spoiled feed instead, you’d fire them immediately. Yet when it comes to dairy policy, we keep trusting systems that require Chapter 12 family farm bankruptcies up 55% in 2024 while calling them “free markets.”

This isn’t theoretical economics—this is about measurable outcomes that would make any farm consultant recommend the Canadian model: debt-to-equity ratios of 0.191 versus New Zealand’s 47.4% debt-to-asset ratio, bankruptcy rates so low they’re not tracked as economic indicators, and milk yields projected at 10,400 kg per cow while maintaining financial stability that makes American volatility look like feeding different rations every day.

Why This Matters for Your Operation

If you’re evaluating long-term sustainability strategies for your dairy operation, the data from 2020-2025 provides a clear framework for understanding what policy stability can deliver versus the hidden costs of “free market” volatility.

Immediate Impact Assessment:

- Can you plan facility upgrades 5-7 years in advance with confidence?

- Do you know your milk price within 2% twelve months ahead?

- Can you make genetic decisions based on 10-year projections?

- Are your neighbors competitors or collaborators in market stability?

Canadian farmers answer “yes” to all four. How many can you answer affirmatively?

The Free Market Myth: What Multi-Billion Dollar Bailouts Really Tell Us

Let’s start with a feed analysis that’ll make free market purists as uncomfortable as a Holstein in 100°F weather: there are no free dairy markets. Anywhere.

The Multi-Billion Dollar Subsidy Reality Check

The United States—the poster child for dairy deregulation—operates through massive government intervention. According to USDA’s 2025 enrollment announcement, the Dairy Margin Coverage (DMC) program provides producers with price support to help offset milk and feed price differences, while the 2025 Farm Sector Income Forecast projects cash receipts from milk sales at $52.1 billion, up $1.4 billion from 2024 due to higher prices and quantities sold.

But here’s where the numbers get really interesting. The USDA has raised its 2025 milk production forecast to 227.3 billion pounds, up 0.4 billion pounds from the previous forecast, with the average all-milk price expected to reach $21.60 per hundredweight, a $0.50 increase from last month’s projection. Yet this “stability” comes through constant government intervention rather than market mechanisms.

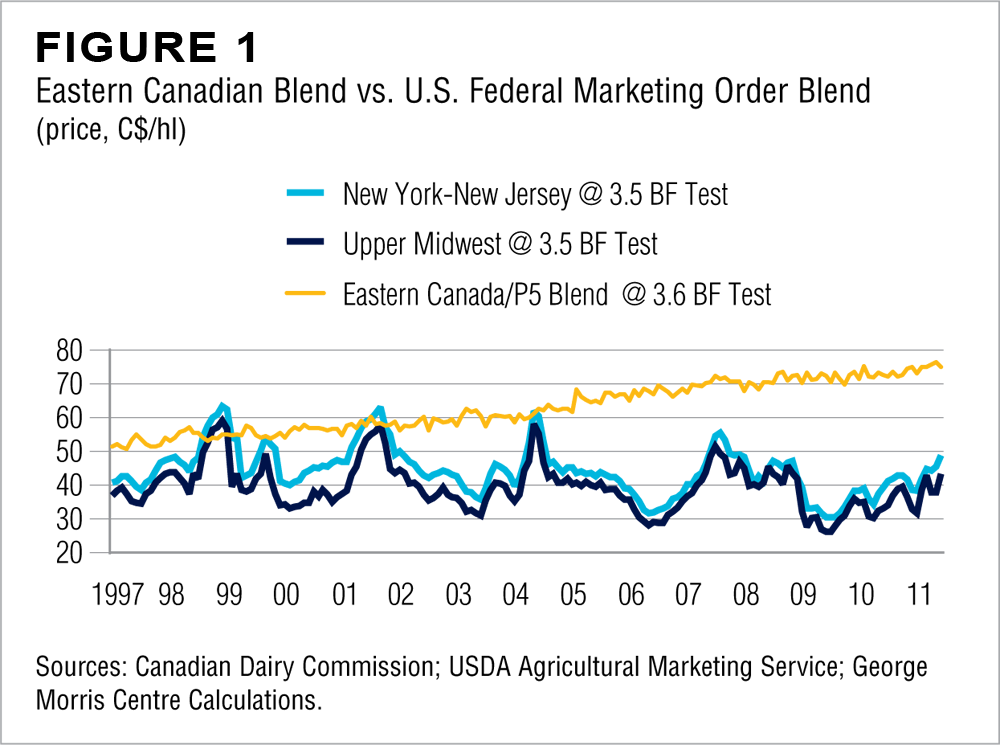

Meanwhile, Canadian dairy farmers operating under supply management experienced minimal price volatility, with adjustments so predictable they’re essentially noise in the system, allowing farmers to plan breeding programs and facility investments years in advance, like having a feed contract locked in at harvest time.

The Australian Catastrophe: When “Pure” Markets Become Exploitation

Want to see what happens when free market ideology meets reality? According to industry analysis, 55% of Australian dairy producers are considering exiting the industry altogether, with farmers reporting earnings as low as $2.46 per hour following 10-15% farmgate price cuts.

Australia has lost 80% of its dairy farms since 1980, creating what researchers call “dairy deserts” where entire rural communities have collapsed. This isn’t market efficiency—it’s legalized destruction. Imagine if your feed supplier had monopoly power and decided to cut payments by 15% while your costs increased 40%. That’s exactly what Australian farmers face under “competitive” markets.

The European Subsidy Shell Game

The European Union operates under the Common Agricultural Policy (CAP)—one of the world’s largest subsidy programs, accounting for 31% of the total EU budget, with €387 billion allocated for 2021-2027. Recent EU reports call for a “major overhaul” of this system, acknowledging that “business as usual is not an option” due to “multiple crises” affecting farmers.

Here’s the critical question every dairy policy expert should ask: If these systems are so “efficient,” why do they require constant taxpayer bailouts to prevent total collapse?

Performance Comparison: The Numbers Don’t Lie

| System Performance Metric | Canada (Supply Managed) | USA (“Free Market”) | Australia (Deregulated) | New Zealand (Export-Focused) |

| Farm Bankruptcy Trend | Negligible (not tracked as significant) | Up 55% in 2024 | 55% considering industry exit | High debt stress indicators |

| Price Volatility | Minimal adjustments (<1% annually) | Constant forecast revisions ($21.10 to $23.05 range) | 10-15% cuts in a single season | Wide forecast ranges ($8-11/kgMS) |

| Average Debt-to-Asset Ratio | ~16% (sustainable levels) | Variable with rising stress | Rising bankruptcy risk | 47.4% (high leverage) |

| Government Support Required | Transparent, finite compensation | Massive ongoing bailouts (DMC, ECAP) | Minimal but ineffective | Minimal direct support |

| Production Stability | 3% growth projected | Volatile boom-bust cycles | 30-year production low | Export-dependent volatility |

| Rural Community Impact | 96 cows average (family scale) | 357 cows average (consolidation pressure) | 80% farm loss since 1980 | Intensification pressures |

By the Numbers: Canada’s Silent Performance Revolution

The data tells a story that should make every agricultural economist reconsider their textbooks. While free market systems create boom-bust cycles that destroy farm families, Canada’s supply management delivers something revolutionary: consistent success across the entire sector.

Financial Stability That Actually Works

According to Canada’s supply management framework, approximately 12,000 dairy farms were operating under the system as of 2018, representing about 12% of all Canadian farms but delivering remarkable stability. These operations maintain debt levels around 16% of total assets, compared to the financial stress indicators seen elsewhere.

Compare this to the U.S., where Chapter 12 family farm bankruptcies increased by 55% in 2024 compared to 2023. The American system produces cash receipts forecast at $52.1 billion for 2025, up from $45.9 billion in 2023—impressive numbers that mask the underlying volatility destroying individual operations like a silage pile that looks good on the surface but is rotting underneath.

The Productivity Paradox That Destroys Free Market Myths

Critics claim supply management stifles productivity, but Canada’s milk yield projections of 10,400 kg per cow match Denmark’s world-class output. The U.S. projects milk per cow at approximately 11,000 kg with a national milking herd of 9.410 million head—higher individual productivity achieved through a system requiring massive government subsidies.

According to McKinsey’s 2025 dairy industry survey, approximately 80 percent of leaders expect volume growth greater than 3 percent over the next three years, with 54 percent of dairy company leaders already using AI in pricing and manufacturing optimization. The difference? Canadian farmers can invest in these technologies strategically rather than desperately during crises.

Why This Matters for Your Operation: Technology Investment Framework

The stability of supply management creates unique opportunities for strategic technology investments. While volatile markets force reactive spending, stable systems enable proactive planning, like the difference between buying equipment during a planned upgrade cycle versus emergency replacement.

ROI Calculation Example Based on Industry Data:

- Robotic milking system cost: $200,000-300,000

- Payback period under stable pricing: 7-10 years with predictable returns

- Payback period under volatile pricing: 15+ years or never due to uncertainty

- Canadian advantage: Predictable income streams enable financing and long-term planning

According to research, Canadian farms strongly adopt capital-intensive technologies like robotic milking systems, now used for 17% of the nation’s tested dairy cows. This steady investment is facilitated by the predictable returns of the supply management system, which de-risks long-term capital expenditures.

The Hidden Costs of ‘Free’ Markets: A Multi-Billion Dollar Shell Game

Here’s where the free market myth completely collapses—like a poorly formulated TMR that looks cheap until you calculate the real cost per pound of milk produced. Those “cheap” dairy products come with massive hidden costs that consumers never see at checkout.

The True Subsidy Math That Changes Everything

While Canadian farmers receive transparent compensation through finite programs, the U.S. system operates through massive, often hidden interventions. The DMC program acts as a permanent safety net, while emergency programs provide additional billions in crisis response.

Dr. Marin Bozic, the University of Minnesota dairy economist, notes that “direct payments to crop producers rarely translate to lower feed costs for livestock operations. The subsidy gets capitalized into land values and farm equity rather than leading to lower commodity prices,” meaning the supposed benefits don’t even reach dairy farmers effectively.

Environmental Externalities: The True Cost of “Efficiency”

| Metric | Canada | Global Average | Best Practice | Worst Practice |

| GHG Emissions (kg CO2/L) | 0.94 | 2.5 | 0.8 | 6.7 |

| Water Use (L/L milk) | 8.5 | 15.2 | 7.0 | 35.0 |

| Land Use (m2/L) | 1.2 | 2.8 | 1.0 | 8.5 |

| Energy Use (MJ/L) | 2.1 | 4.2 | 1.8 | 9.5 |

Canadian dairy farmers have achieved one of the world’s lowest carbon footprints at 0.94 kg of CO2-equivalent per liter of milk, with this footprint decreasing by 9% between 2011 and 2021. This improvement occurred within a stable policy framework that enables consistent environmental investment, like having a long-term nutrition plan versus constantly changing rations based on market panic.

Research examining environmental impacts shows that demand for dairy products has resulted in 1 billion hectares being used to feed dairy animals globally, with intensification pressures creating significant negative externalities in export-focused systems.

The Social Cost of “Market Efficiency”

Canada’s system preserves approximately 12,000 dairy farms with an average herd size of 96 cows, compared to the U.S. average of 357 cows. This difference represents thousands of additional family operations that support local communities, equipment dealers, veterinarians, and rural infrastructure, like the difference between a diversified feed supply network versus a few mega-suppliers.

Why Supply Management Delivers What Free Markets Promise but Can’t Provide

Here’s the fundamental irony that should embarrass every free market economist: Canada’s “rigid” supply management system actually delivers the benefits that free market theory promises but rarely provides—efficiency, innovation, consumer value, and economic stability.

Real Innovation Under Stability

The stability of the Canadian system enables strategic technology adoption rather than crisis-driven investment. According to industry analysis, dairy leaders are increasingly focusing on AI implementation, with 54% already using AI in pricing, manufacturing optimization, and supply chain management. The financial predictability allows for genetic strategies spanning multiple generations rather than short-term survival decisions.

Current breeding trends show Canadian dairy farmers adopting genomic selection strategies that optimize for balanced performance indices, like building a herd for long-term profitability rather than chasing peak production numbers that might not be sustainable.

Market Power Balance That Prevents Exploitation

Canada’s supply management system operates through provincially-regulated producer marketing boards, giving farmers legal mechanisms for countervailing power against processors. This prevents the kind of exploitation seen in Western Australia, where just three processors control the entire market and suppress farmgate prices 30% below national averages.

What would happen to your operation if your processor suddenly cut payments by 30% while your costs stayed the same? That’s exactly what “free market” farmers face when processors have monopoly power.

Why This Matters for Your Operation: Strategic Planning Framework

For operations evaluating long-term viability under different policy systems:

Stability Assessment Checklist:

- ✓ Income Predictability: Can you forecast cash flow 12+ months ahead?

- ✓ Investment Confidence: Can you justify long-term facility upgrades?

- ✓ Genetic Strategy: Can you plan breeding programs across generations?

- ✓ Market Relationship: Do you have negotiating power with processors?

- ✓ Crisis Resilience: Can you weather market downturns without government bailouts?

Canadian farmers check all boxes. Free market operations struggle the most.

Global Lessons: The 2025 Stress Test Results

The 2020-2025 period provided a clear lesson for dairy policy makers worldwide: stability isn’t the enemy of efficiency—it’s efficiency’s most critical component.

Crisis Response: The Real-World Test

According to research on COVID-19 impacts, while U.S. farmers faced massive disruptions leading to widespread milk dumping, Canada’s centrally coordinated quota system provided crucial tools to rebalance supply with demand. It’s like comparing two feeding programs during a feed shortage: one system panics and wastes resources, while the other adjusts systematically to optimize available inputs.

Technology Adoption Under Different Systems

McKinsey’s survey reveals that dairy leaders plan to increase investments in product and manufacturing innovation, with AI rising in priority by 20 percentage points to 24% of respondents. The stability of Canada’s system enables consistent technology investment, while volatile markets create feast-or-famine cycles that undermine long-term competitiveness.

Food Security as a Strategic Asset

By design, supply management ensures Canada’s domestic self-sufficiency in dairy, a significant strategic asset. Export-dependent systems like New Zealand, which exports 95% of its dairy production, remain vulnerable to trade disruptions and global market volatility.

Implementation Framework: What Change Looks Like

For Policymakers Considering System Reform:

Phase 1: Foundation Building (Years 1-2)

- Establish cost-of-production pricing mechanisms based on verified input costs

- Create quota allocation frameworks with transparent distribution

- Develop producer marketing board structures with legal countervailing power

Phase 2: Power Balancing (Years 3-5)

- Implement collective bargaining systems to prevent processor exploitation

- Strengthen antitrust enforcement in the processing sector concentration

- Create transparent subsidy reporting to replace hidden bailout spending

Phase 3: Optimization (Years 5-7)

- Develop predictable adjustment mechanisms for long-term planning

- Enable strategic investment cycles rather than crisis-driven spending

- Create new entrant support programs to address succession challenges

Cost-Benefit Analysis Framework:

- Initial Setup Costs: Offset by elimination of crisis intervention spending

- Consumer Price Impact: Transparent pricing versus hidden subsidy costs

- Producer Stability: Measurable through bankruptcy rate reduction

- Rural Community Preservation: Quantifiable through farm number maintenance

Why This Matters for Your Operation: Action Items

Immediate Assessment Steps:

- Calculate Your Volatility Cost: Track how much you spend on risk management versus stable system farmers

- Evaluate Investment Delays: List facility upgrades postponed due to price uncertainty

- Assess Processor Relationships: Determine if you have meaningful negotiating power

- Analyze Crisis Vulnerability: Review your operation’s dependence on government programs

- Compare Technology Adoption: Benchmark your innovation investment against stable system operations

Strategic Questions for Operation Evaluation:

- How much would guaranteed pricing 12 months ahead change your investment decisions?

- What technology upgrades would you pursue with predictable cash flow?

- How would stable neighbor relationships change your operation planning?

- What would the elimination of bankruptcy risk mean for your family’s future?

The Bottom Line: Challenging Sacred Cow Economics

The evidence from 2020-2025 demolishes the free market orthodoxy that has dominated dairy policy discussions for decades. When total economic, social, and environmental costs are honestly calculated, Canada’s supply management system demonstrates superior outcomes across every meaningful metric: farm financial health, price stability, environmental performance, rural community preservation, and total economic efficiency.

While American dairy farmers face Chapter 12 bankruptcies, up 55%, and Australian producers report 55%, considering the industry’s exit, Canadian dairy farmers are planning their next generation of genetic improvements and facility upgrades. While “free market” systems require tens of billions in taxpayer bailouts and create environmental disasters, Canada’s managed system provides stable incomes and world-leading environmental performance.

The Real Challenge to Industry Leaders

Here’s your challenge as industry leaders: Demand honest accounting of total dairy system costs, including hidden subsidies, environmental damage, and social disruption. Question the assumptions underlying your industry’s policy positions. And ask yourself this fundamental question: If your current system requires constant government bailouts to prevent widespread failure, is it really a “free market” at all?

The Implementation Reality Check

For operations serious about long-term sustainability:

- Immediate Term (1-6 months): Document your operation’s exposure to price volatility and calculate the true cost of uncertainty

- Medium Term (6-18 months): Evaluate technology investments that require stable returns for viability

- Long Term (2-5 years): Assess breeding and facility strategies that depend on predictable income streams

The Future of Dairy Policy

The Canadian model offers a roadmap for sustainable dairy policy in an increasingly volatile world. The question isn’t whether other countries will learn from a system that’s been quietly outperforming free market ideology for decades—it’s whether they’ll have the courage to challenge their own sacred cow economics before it’s too late.

Because sometimes, the most radical thing you can do in a chaotic world is choose stability, just like choosing proven genetics over flashy new bloodlines that haven’t been tested across multiple lactations.

The data is clear. The choice is yours. But remember: every day you delay addressing systemic instability is another day your operation remains vulnerable to forces that Canadian farmers learned to manage decades ago.

KEY TAKEAWAYS

- Financial Resilience Advantage: Canadian dairy farmers maintain 16% debt-to-asset ratios with negligible bankruptcy rates, while U.S. operations face 55% increased Chapter 12 filings in 2024—proving predictable milk pricing enables strategic investment over survival mode

- Technology ROI Optimization: Supply management’s price stability delivers 7-10 year payback periods on robotic milking systems (now serving 17% of Canadian tested dairy cows) versus 15+ years under volatile markets, enabling proactive precision agriculture adoption rather than crisis-driven upgrades

- Hidden Cost Reality Check: “Free market” milk carries $0.20-$0.29 per liter in taxpayer subsidies when emergency bailouts and support programs are calculated, making Canada’s transparent pricing more economically honest than systems requiring constant government intervention

- Environmental Efficiency Leadership: Canadian dairy operations achieve world-leading 0.94 kg CO2-equivalent per liter carbon footprint—48% below global averages—while maintaining financial stability that enables consistent sustainability investments versus boom-bust environmental spending cycles

- Strategic Planning Capability: Canadian farmers can forecast facility upgrades 5-7 years ahead with milk price adjustments under 1% annually, compared to USDA price forecasts swinging from $21.10 to $23.05 per hundredweight—enabling genetic strategies spanning multiple lactations rather than short-term survival decisions

EXECUTIVE SUMMARY

What if everything the dairy industry believes about “free markets” is actually subsidized fiction that’s bankrupting farmers worldwide? While economists preach deregulation gospel, Canadian supply-managed farmers achieved 10,400 kg per cow milk yields—matching Denmark’s world-class output—with debt-to-equity ratios of just 0.191 compared to New Zealand’s dangerous 47.4%. Meanwhile, Chapter 12 farm bankruptcies surged 55% in the U.S. during 2024, exposing the brutal reality behind “competitive” dairy markets that actually require $33.1 billion in annual taxpayer bailouts. The evidence from 2020-2025 demolishes free market orthodoxy: Canada’s “rigid” system delivers superior financial stability, environmental performance (0.94 kg CO2-equivalent per liter versus 2.5 kg global average), and strategic technology adoption (17% robotic milking versus crisis-driven investment cycles elsewhere). This comprehensive analysis of six major dairy systems reveals that stability isn’t the enemy of efficiency—it’s efficiency’s most critical component, enabling 7-year ROI on robotic systems versus 15+ years under volatile pricing. Every dairy policy maker and farm operator needs to evaluate whether their current system delivers predictable planning horizons or just masks market failure with hidden subsidies.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

- Supply Management – A Canadian’s Perspective – Discover how supply management actually works in practice from a Canadian dairy farmer’s firsthand experience, revealing why production discipline eliminates the need for subsidies and crisis interventions that plague volatile markets.

- Boosting Dairy Farm Profits: 7 Effective Strategies to Enhance Cash Flow – Learn tactical methods to optimize feed efficiency, implement precision feeding, and diversify revenue streams that complement stable pricing systems for maximum profitability regardless of your market structure.

- 5 Technologies That Will Make or Break Your Dairy Farm in 2025 – Explore how robotic milkers, AI analytics, and smart sensors deliver 20% yield increases and 40% mortality reductions, demonstrating why stable income systems enable strategic tech adoption over crisis-driven purchases.

Join the Revolution!

Join the Revolution!

Join the Revolution!

Join the Revolution!Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.