When milk is worth 34.5ppl, and it costs close to 49ppl to produce, your contract decides whether you survive this squeeze or bleed cash until the bank decides for you.

EXECUTIVE SUMMARY: Two farms. Same county. Same herd size. One loses £187,500 more this year—the only difference is the contract. UK milk sits at 34.5ppl while production costs hit 49ppl (FAS Scotland, January 2026), leaving farmers on processor-discretionary deals 14-15ppl underwater on every litre. AHDB forecasts no relief until H2 2026 at the earliest. Seven contract clauses are doing the damage—from indemnification language that pins processor-facility contamination on you, to volume traps that trigger clawbacks when drought cuts your output. The UK’s Fair Dealing regulations gave farmers a complaints process, but in ASCA’s first twelve months, not one producer filed formally; nine called in confidence, then went silent. For non-aligned operations with less than six months of cash, the decision window isn’t approaching—it’s here.

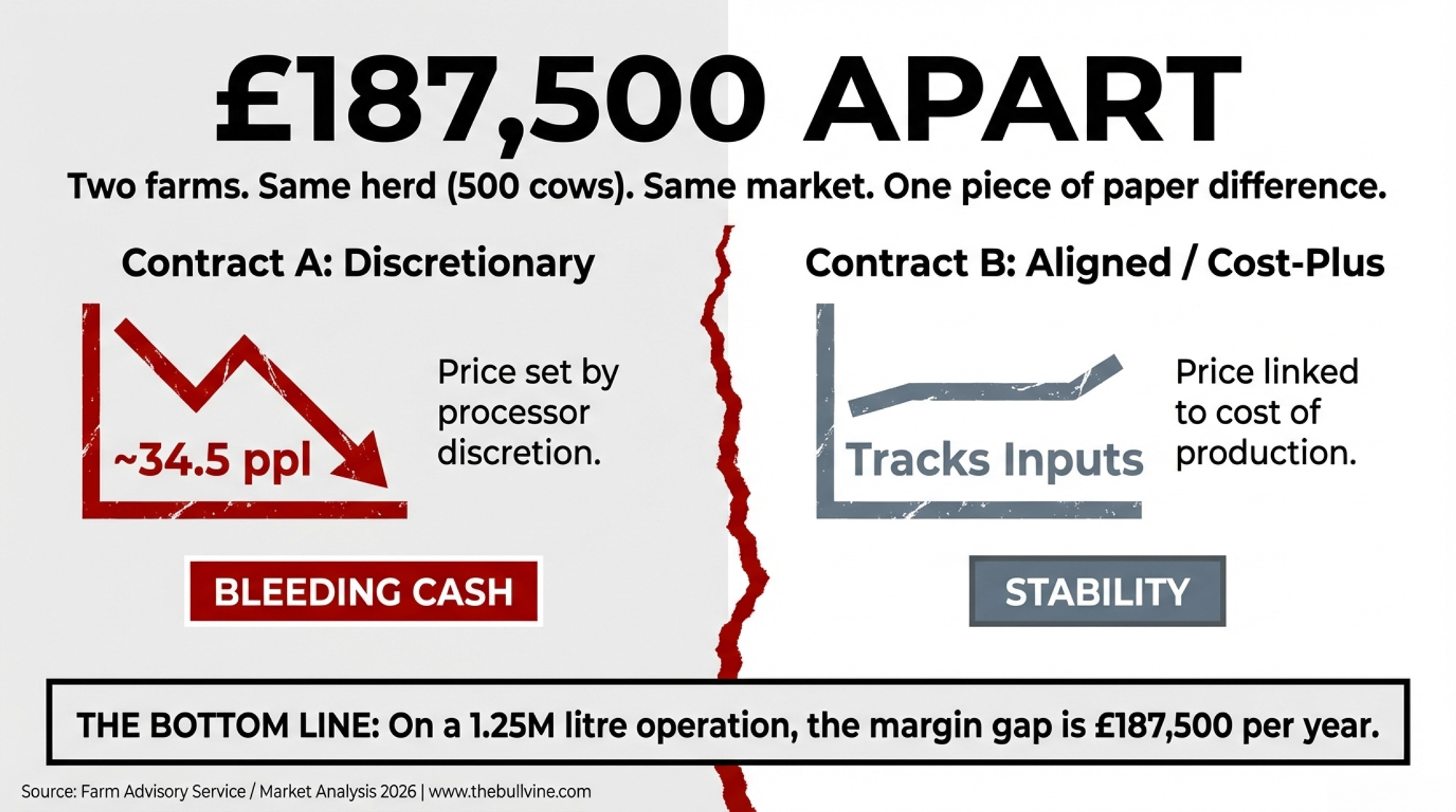

Two farms. Same county. Same herd size. Same brutal market.

One loses close to £190,000 more this year than the other.

The difference isn’t just Müller’s March 2026 price cut to 34.5ppl. It’s not only the record milk glut or the butter crash. It’s what’s written in the contract—specifically, which operation bears the downside when processors slash farmgate prices, and which has terms that track costs and provide a floor.

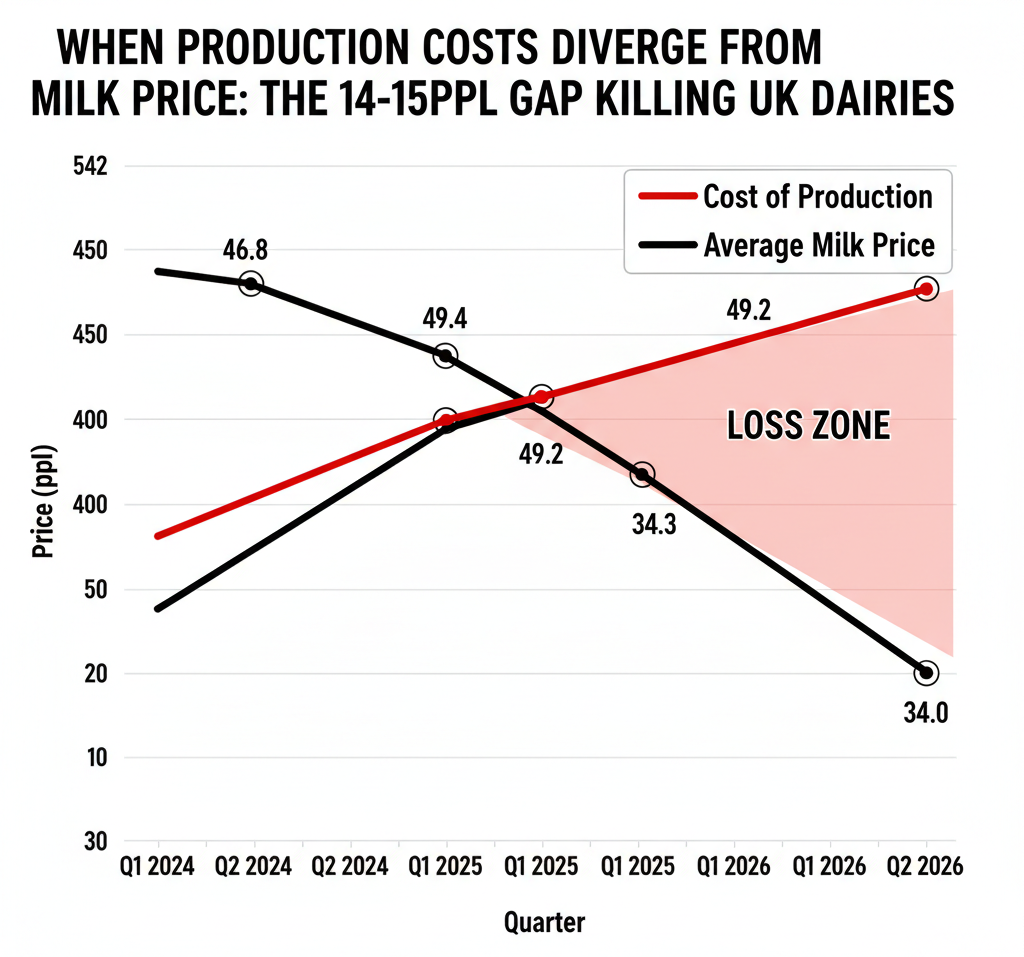

Aligned retail contracts held steady in January 2026. Processor-discretionary deals dropped 1-4ppl. Meanwhile, The Dairy Group—reporting through Scotland’s Farm Advisory Service in January 2026—put the average cost of production at 48.5ppl for 2024/25, with a forecast of 49.2ppl for 2025/26. That means many non-aligned farms are now producing milk for roughly 14–15ppl more than they’re being paid.

On a 500-cow operation producing 1.25 million litres annually, that 14–15ppl gap represents roughly £175,000–£187,500 per year in lost margin compared with a neighbour on a cost-of-production-linked contract facing the same market.

| Farm Parameter | Farm A (Non-Aligned) | Farm B (Aligned Retail) | Difference |

| Herd Size | 500 cows | 500 cows | — |

| Annual Production | 1.25M litres | 1.25M litres | — |

| Milk Price (Early 2026) | 34.5 ppl | 48.5 ppl | +14.0 ppl |

| Cost of Production | 49.2 ppl | 49.2 ppl | — |

| Margin per Litre | -14.7 ppl | -0.7 ppl | +14.0 ppl |

| Annual Loss/Profit | -£183,750 | -£8,750 | £175,000 |

“Prices are falling fast while costs remain high,” said Bruce Mackie, chair of NFU Scotland’s Milk Committee, in December 2025. “Processors must communicate clearly and fairly with suppliers.”

The UK now has regulatory teeth—the Fair Dealing Obligations (Milk) Regulations 2024 and the Agricultural Supply Chain Adjudicator to enforce them. But in ASCA’s first 12 months, not a single formal complaint landed across the entire industry. Nine farmers rang up in confidence. None followed through.

Is the regulation toothless, or are farmers too terrified of their milk buyer to bite back?

The Market Numbers You’re Up Against

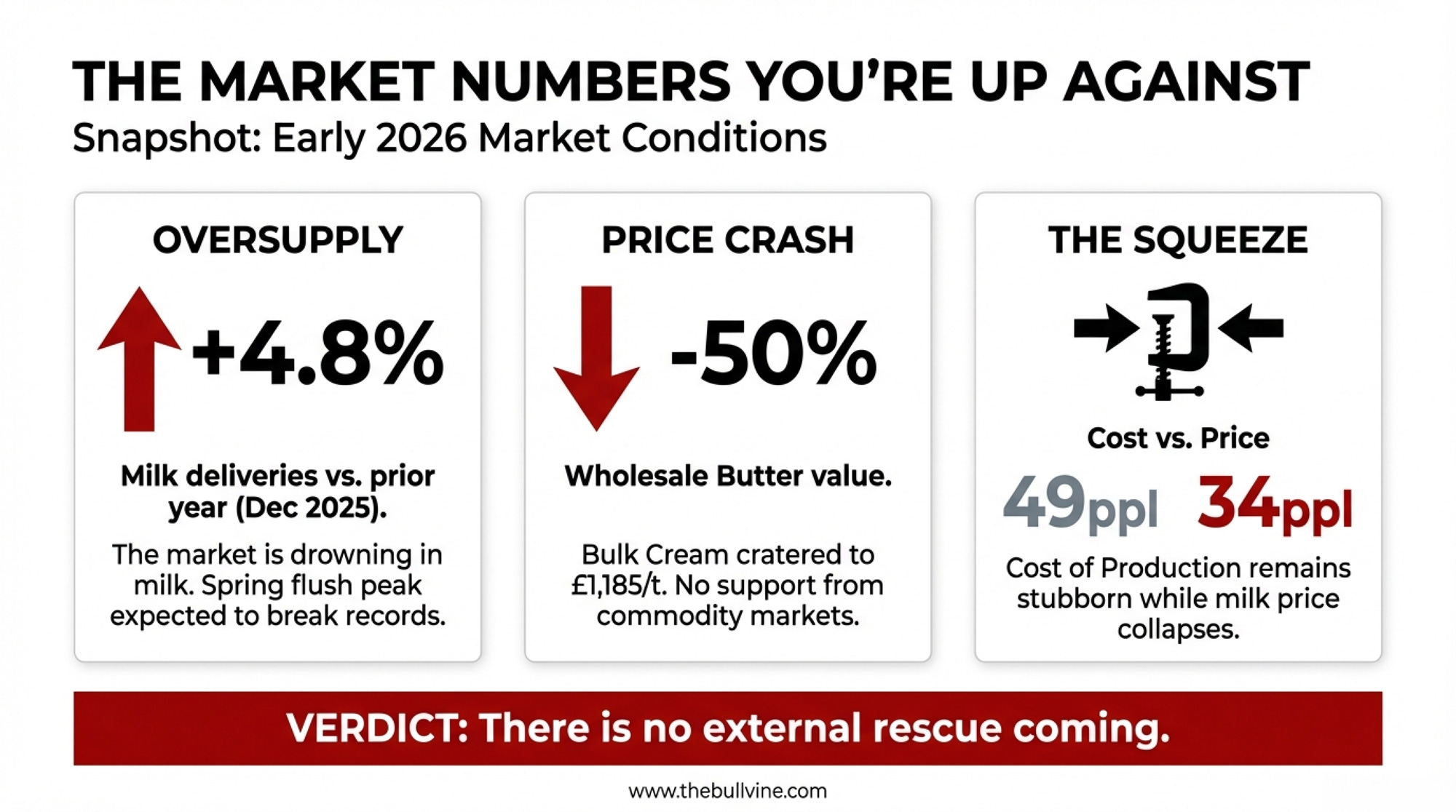

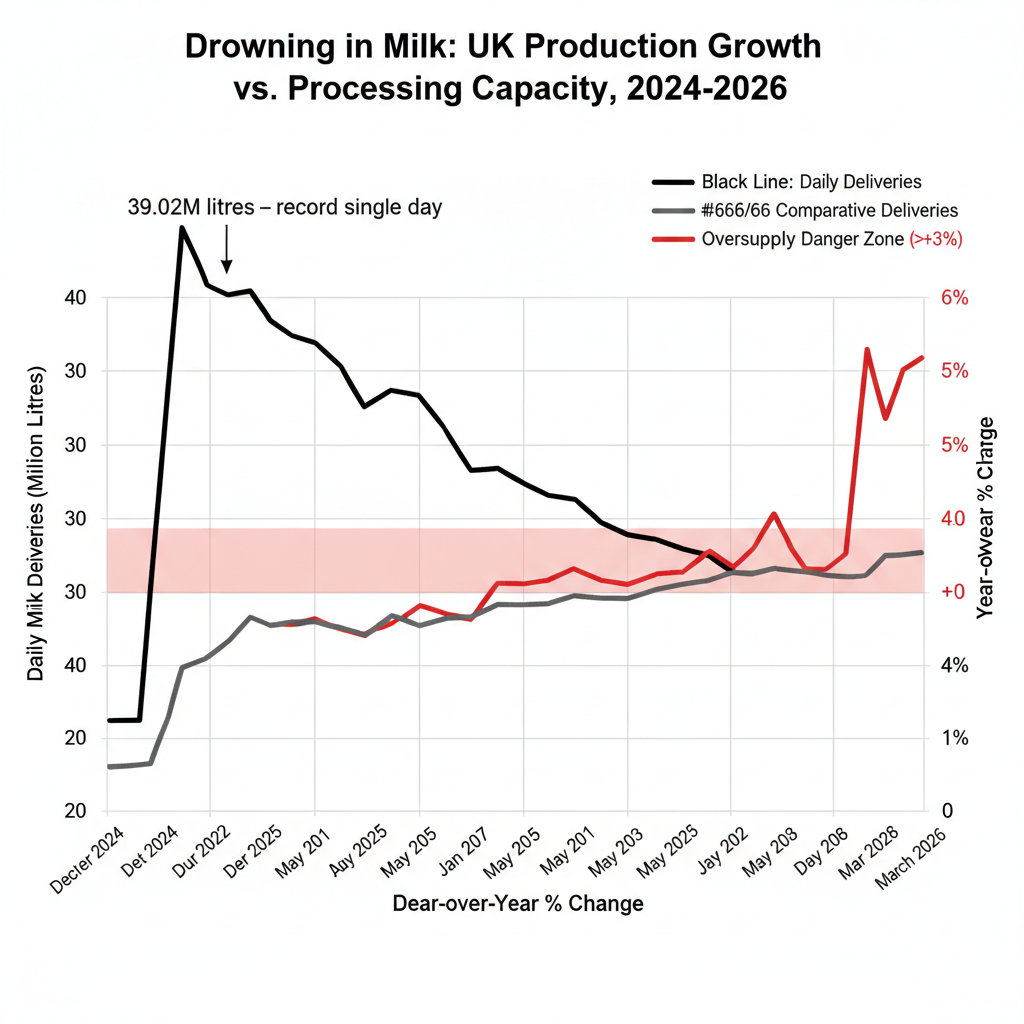

UK dairy entered 2026 drowning in milk. December 2025 deliveries averaged around 35.6 million litres daily—4.8% above the prior year, according to AHDB. Total GB production for 2025/26 is forecast at a record 13.05 billion litres. Spring flush 2025 peaked at 39.02 million litres on May 4—the highest single-day volume ever recorded.

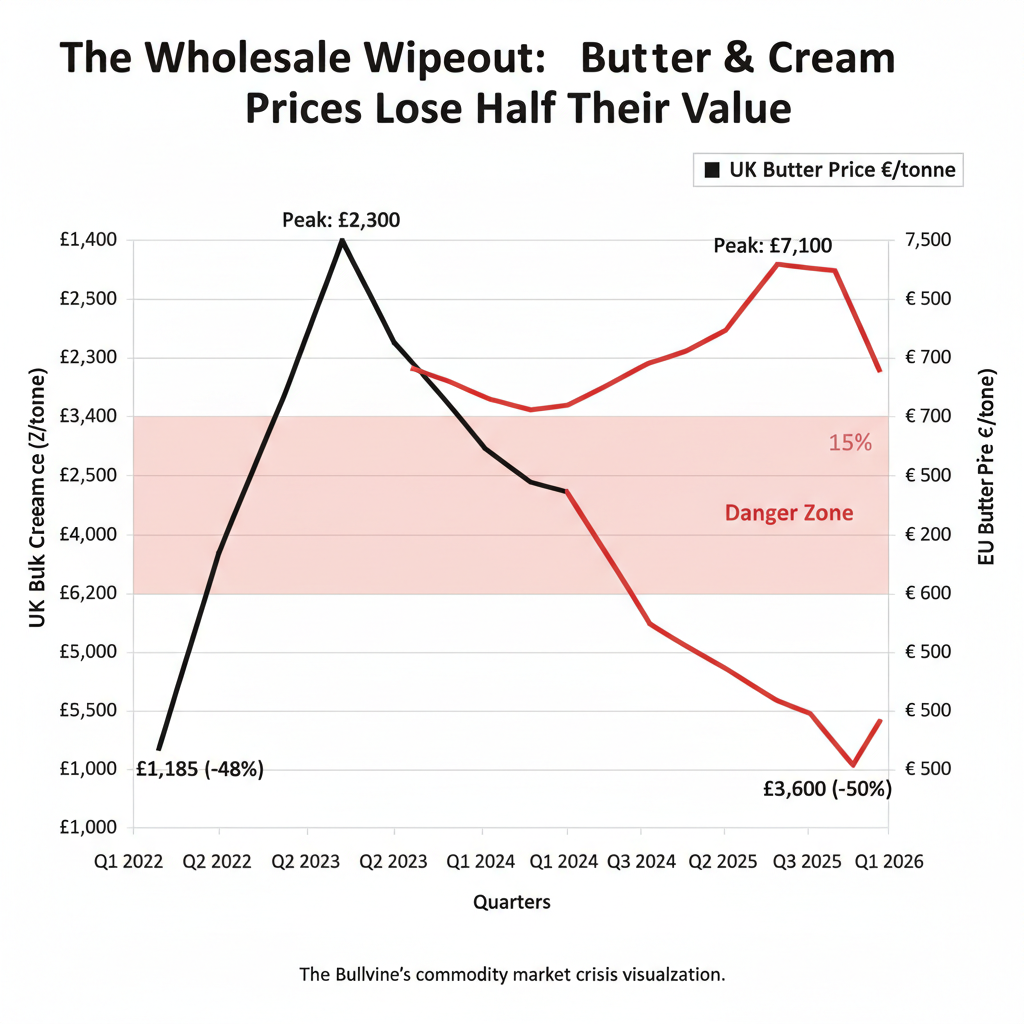

Wholesale markets buckled. Bulk cream cratered to £1,185 per tonne in January 2026, down 10% from December, per AHDB. UK wholesale butter averaged £3,600 per tonne for the month—AHDB notes it “has now lost over half of its value since the peak.” European butter slid below €4,000 per tonne in late January, down from over €7,000 at the 2022 high.

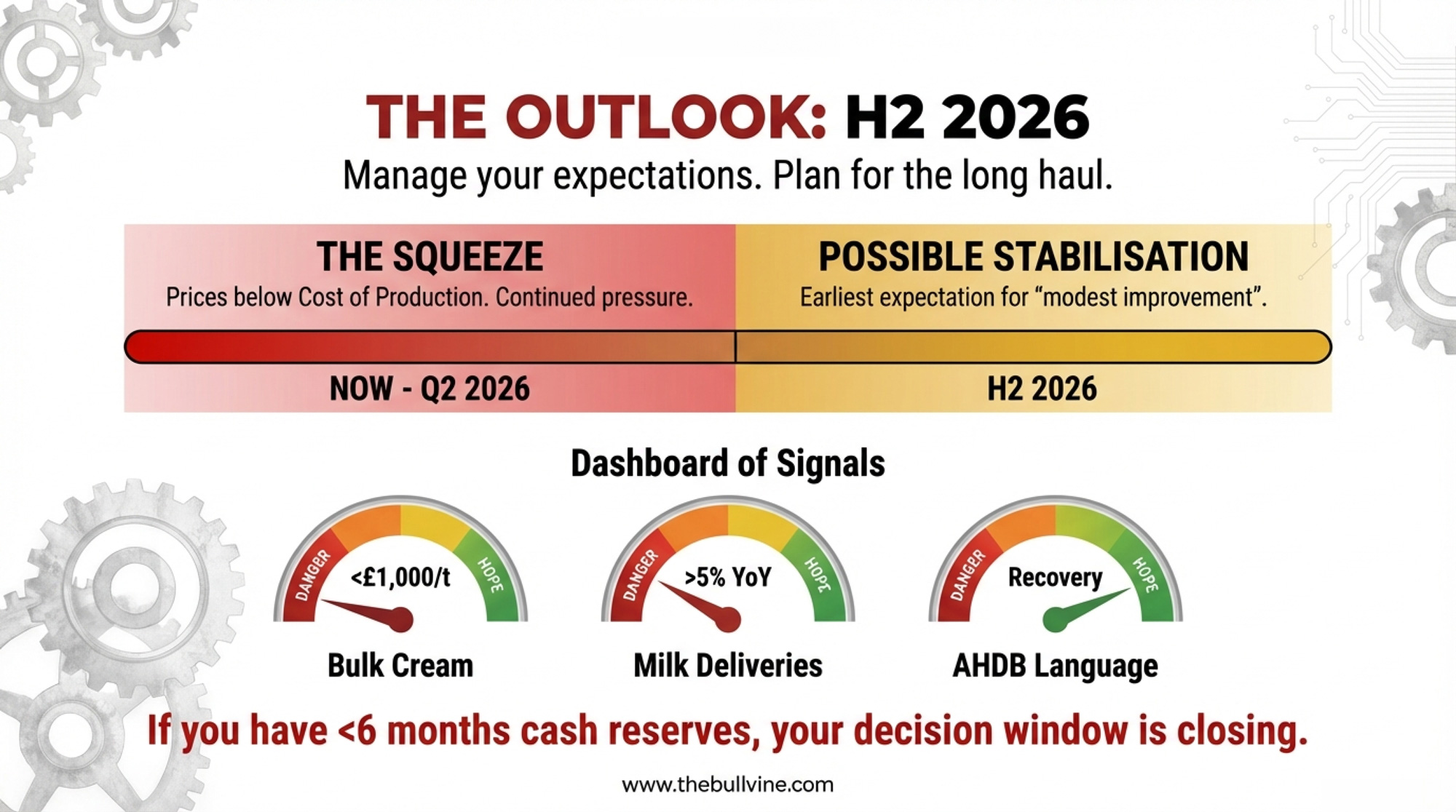

AHDB’s January 2026 outlook didn’t mince words: milk prices are “set to stay under pressure through the first half of 2026” with only “modest improvement” expected later. Rabobank’s Q4 2025 update pegs global supply growth at just 0.12% for 2026, with actual decline not expected until the first half of 2027.

FAS Scotland confirms it plainly: milk price was below the cost of production for most of 2025 and remains so heading into spring.

If your contract amplifies downturns, you’re staring down at least six more months of pain with no structural relief on the horizon.

A Global Problem, Not Just a UK One

While this analysis focuses on UK contracts and FDOM regulations, producers across the globe are fighting the same battle between discretionary and formula-based pricing.

In the US, the gap between Federal Milk Marketing Order Class III prices and actual processor pay has sparked renewed debate about order reform—with some co-ops offering cost-plus contracts while others stick to commodity-based formulas. EU producers face similar tensions as intervention prices sit well below production costs in many member states. The contract structures differ, but the fundamental question is identical: who absorbs the pain when markets turn?

UK farmers have FDOM. American producers have FMMO reform debates. EU farmers have CAP negotiations. None of these frameworks have yet solved the core imbalance: processors can pass risk down; farmers can only absorb it or exit.

Where the Money Actually Lands

The split between contract types has become stark.

Sainsbury’s Sustainable Dairy Development Group suppliers operate under cost-of-production models that flex with input costs. When feed and energy prices spike, the farmgate price rises. When wholesale markets collapse, the formula cushions the fall. These suppliers saw modest price bumps in early 2026.

Farmers locked into processor-discretionary deals—where pricing follows wholesale swings or processor margin targets—caught the full blow:

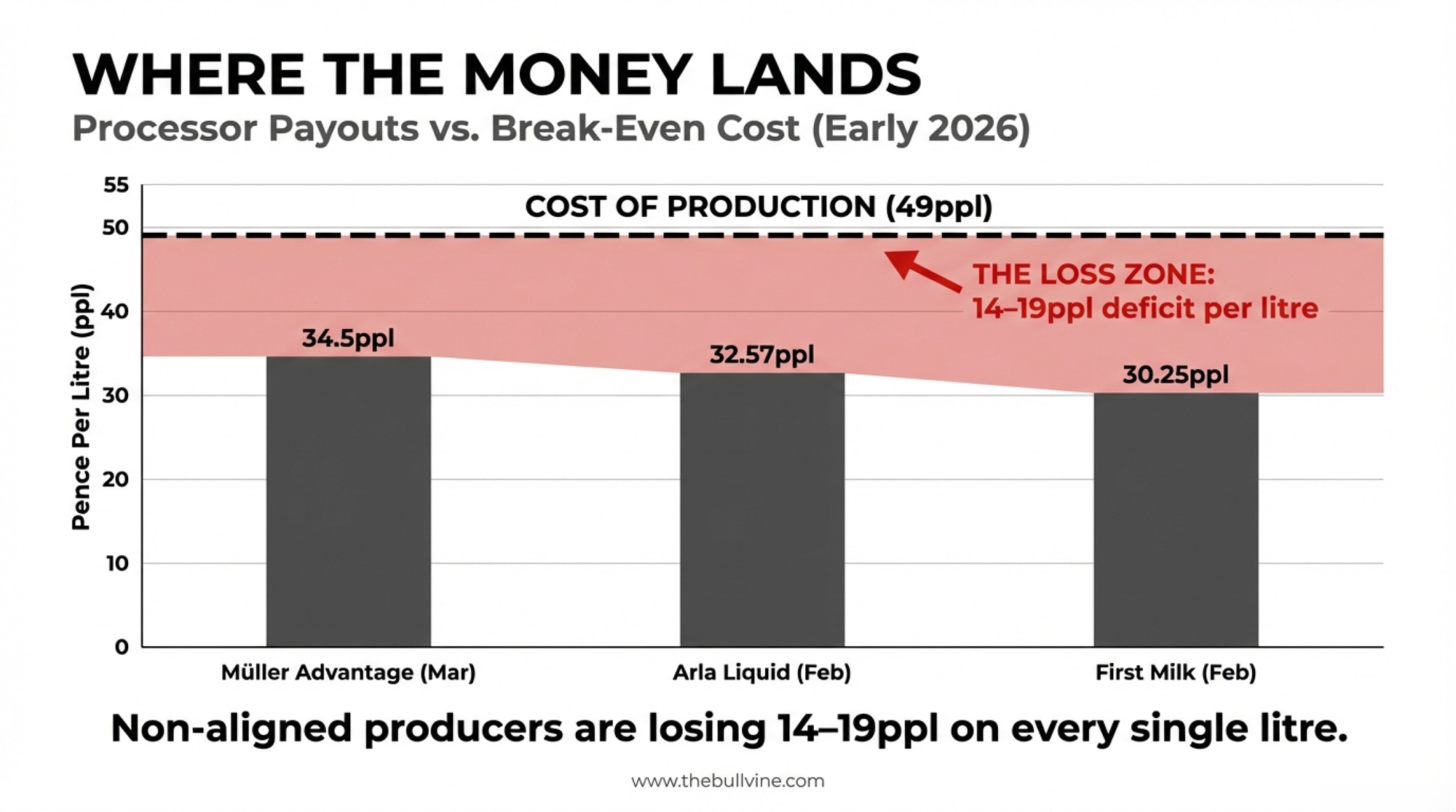

| Processor | Contract Type | Early 2026 Price |

| Müller Advantage | Manufacturing (March) | 34.5ppl |

| First Milk | Manufacturing (February) | 30.25ppl |

| Arla | Liquid (February, GB conventional) | 32.57ppl |

Set those against a cost of production near 49ppl, and many non-aligned producers are losing 14–19ppl on every litre.

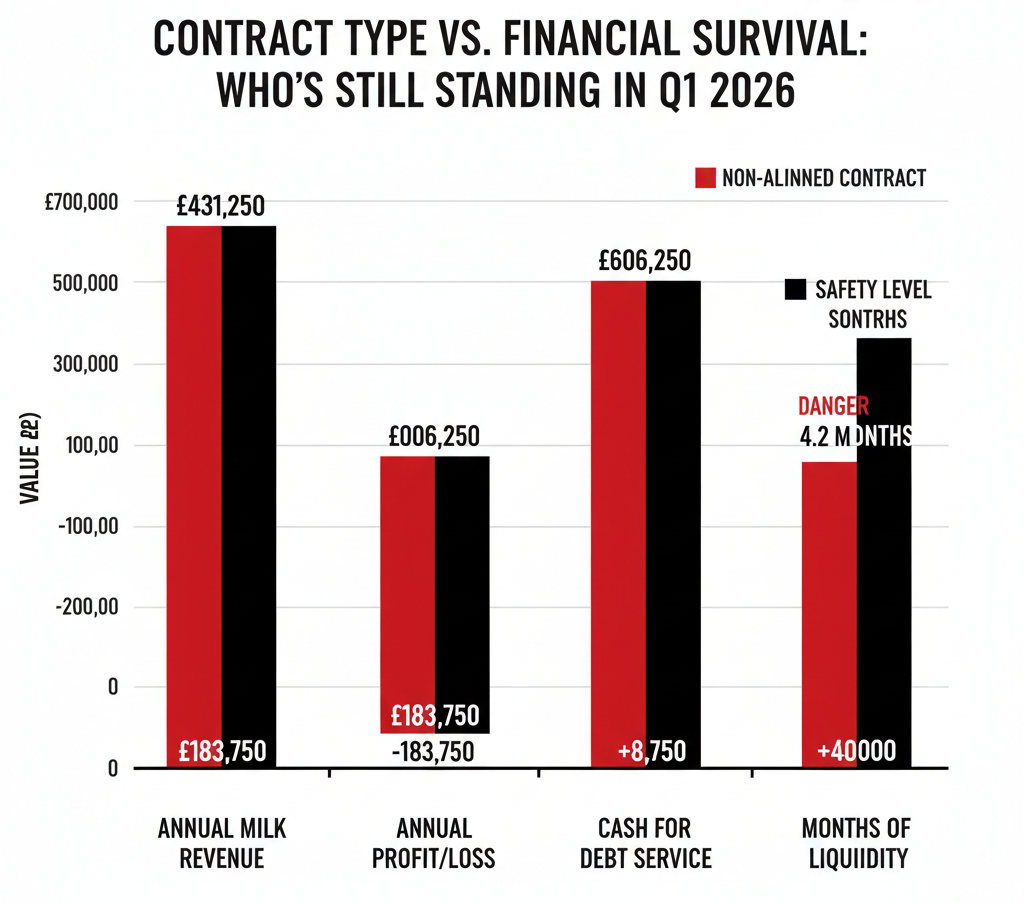

| Metric | Non-Aligned (Red) | Aligned Retail (Black) |

|---|---|---|

| Annual Milk Revenue | £431,250 | £606,250 |

| Annual Profit/Loss | -£183,750 | -£8,750 |

| Cash Available for Debt Service | -£50,000 | +£40,000 |

| Months of Liquidity Remaining | 4.2 months | 18+ months |

On 1.25 million litres, a farm stuck at 34.5ppl instead of cost-linked pricing is effectively giving up £175,000–£187,500per year compared with a neighbour whose contract moves with costs. At 1.5 million litres and a 14ppl loss, you’re looking at roughly £210,000 in negative margin before you pay a penny on capital or debt.

Switching sounds nice. But with synchronized cuts across processors, alternatives aren’t materially better for most farms right now. And FDOM’s 12-month notice requirement means any move you make today won’t take effect until 2027.

Producers from Southwest England to Yorkshire are living the same reality: identical market conditions, wildly different cheques depending on what they signed 12–24 months ago.

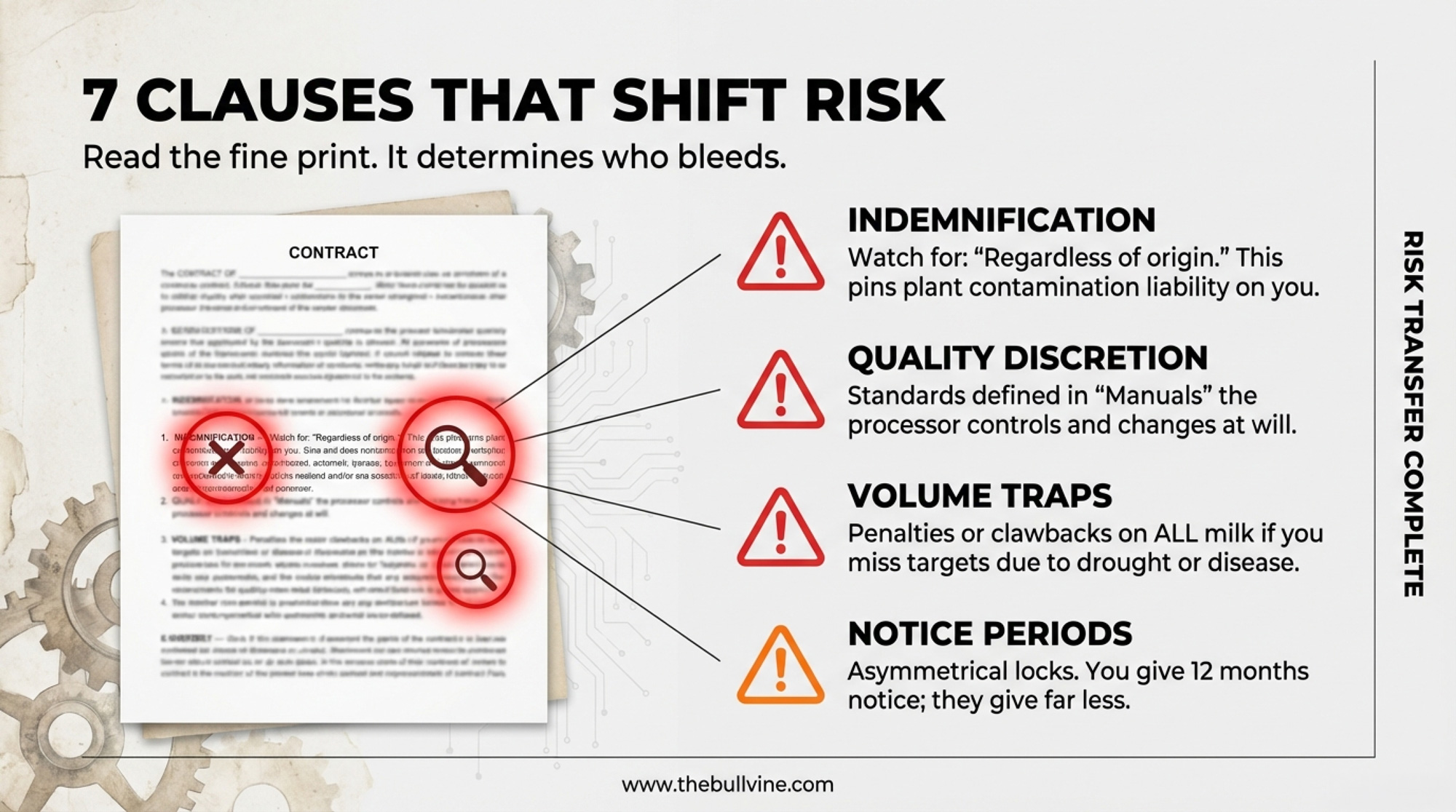

Seven Clauses That Shift Risk Onto Your Back

What separates a protective contract from a loaded gun isn’t the headline price. It’s the fine print.

| Clause | The “Red Flag” | Risk Level |

| Indemnification | “Regardless of origin.” | High |

| Quality Discretion | Processor-controlled manuals | High |

| Volume Traps | Clawbacks on total delivery | High |

| Delayed Payments | Loyalty bonuses forfeited on exit | Medium |

| Confidentiality | No carve-outs for advisors | Medium |

| Notice Period | 12-month asymmetrical locks | Medium |

| Dispute Resolution | Multiple steps before external review | Medium |

Indemnification scope is where real damage hides. Standard language covers losses from your breach or negligence—fair enough. Expanded versions using “regardless of origin” or “arising from or related to the milk supplied” can pin liability for contamination at processor facilities squarely on your operation.

Agricultural attorney Ross Janzen, dissecting US contracts for Progressive Dairy in 2018, flagged this pattern: direct-buy contracts may hold producers “directly liable, not only for their own milk, but milk from other producers or the entire plant.” The mechanics apply similarly to UK contracts.

Quality standard discretion creates similar exposure. If your contract defines requirements by referencing a “Quality Manual,” the processor can rewrite whenever they like, and your pricing can shift mid-term without triggering any formal amendment clause.

Volume commitment traps bite hardest during downturns. What happens when you fall short? Some contracts treat under-delivery—even from drought or disease—as a material breach, triggering price clawbacks on all milk delivered.

| Contract Clause | The “Red Flag” Language | Risk Level | What It Means When Prices Fall |

| Indemnification Scope | “Regardless of origin” or “arising from or related to” | HIGH | You’re liable for contamination at processor facilities—not just your milk, potentially entire plant batches. Legal exposure can exceed annual revenue. |

| Quality Discretion | “As defined in Quality Manual” (processor-controlled) | HIGH | Processor can rewrite quality standards mid-contract, triggering price penalties or rejection without contract amendment. Zero farmer input. |

| Volume Traps | Clawbacks or penalties on “total delivery” if minimums missed | HIGH | Miss volume targets (drought, disease, market exit)? Processor claws back pricing on all milk delivered, not just shortfall. |

| Delayed Payments | Loyalty bonuses or “end-of-year” payments tied to contract completion | MEDIUM | Walk away mid-contract? You forfeit 6–12 months of accrued payments—effectively a financial hostage clause. |

| Confidentiality | No carve-outs for “advisors,” “legal counsel,” or “lenders” | MEDIUM | Can’t share terms with solicitor, accountant, or bank without breach. Makes informed decision-making nearly impossible. |

| Notice Period Asymmetry | 12-month producer notice, 30–90 day processor notice | MEDIUM | You’re locked in for a year; they can exit or cut pricing in 90 days. Risk runs one direction. |

| Dispute Resolution Barriers | “Escalation process” requiring processor internal review first | MEDIUM | Multiple hoops before external adjudication. Designed to exhaust you before you reach ASCA or legal remedy. |

Your Contract Audit Checklist

Before your next contract conversation, nail down these eight items:

- [ ] Indemnification scope: Does the clause include “regardless of origin” or similarly broad language?

- [ ] Quality standards: Defined in the contract, or in external manuals, that the processor controls?

- [ ] Volume commitment remedies: What happens if you miss minimums due to factors outside your control?

- [ ] Payment timing: What chunk of your stated price depends on future behaviour?

- [ ] Notice period symmetry: How much warning do you owe versus what they owe you?

- [ ] Title transfer point: When does ownership move, and who carries risk during haulage?

- [ ] Confidentiality carve-outs: Can you share terms with your solicitor, accountant, and lender?

- [ ] Dispute resolution path: How many hoops between “I have a problem” and external review?

Four Realistic Paths Forward

You’re not going to strong-arm better terms out of your processor. Academic research on dairy supply chains shows that farmers’ bargaining power is well below that of processors. A 500-cow unit doesn’t rewrite standard contract language.

So what can you actually do?

Path 1: Audit for Intelligence

Contract auditing isn’t about renegotiating—it’s about knowing your exposure before the next price cut lands. Map how clauses interact. What happens if you trip the quality threshold while also missing the volume threshold?

Best for: Anyone who hasn’t done this in the last 12–18 months. Requires: 2–3 hours with your contract and a calculator. Downside: None—this is baseline due diligence

Path 2: Find Your Exit Number

Your exit price isn’t simply the cost of production. Cornell economists have shown the rational exit threshold often sits below variable cost because of “option value”—the potential gain from hanging on and catching a recovery. But debt changes that math fast.

The number that matters: At what milk price does cash flow go negative, including debt service? That’s your hard line.

Best for: Non-aligned contract holders carrying significant debt. Requires: Honest cash flow work with your accountant. Downside: Waiting for “confirmation” while cash drains out

Path 3: Position Without Committing

There’s groundwork you can lay before triggering any notice clock:

- Talk to other processors. Exploring alternatives doesn’t breach exclusivity—shipping milk elsewhere does. Options are thin in early 2026. But knowing that is intelligence.

- Run lender scenarios. “What happens if prices stay here through Q3?” Their answer tells you how much runway you actually have.

- Compress costs strategically. NFU Scotland, in a November 2025 advisory, encouraged farmers to “reduce output slightly—selling poorer performing cows while cull prices remain high” to ease cost pressure. But don’t just sell cows—sell your bottom 10% genetically to protect future recovery. When margins turn negative, the embryo budget and top-tier semen are often the first casualties. Make culling decisions that preserve your genetic trajectory, not just your tank space.

Best for: Producers with 6–12 months of cash left. Requires: Uncomfortable conversations with lenders. Downside:Cut too deep, and you hobble your recovery capacity

Path 4: Build a Paper Trail

If pricing looks opaque or inconsistent, document everything. Under FDOM, processors must respond to pricing queries within 7 working days. If they don’t, that’s something concrete for ASCA.

Best for: Anyone who suspects their contract breaches FDOM rules. Requires: Systematic logging of every price notification and query. Downside: The confidential route may produce no visible outcome; the formal route puts you on their radar

Signals to Watch Through Q3 2026

- Bulk cream leads the farmgate by 2–3 months. January’s £1,185/tonne—down 10% month-on-month—signals near-term pressure continues. AHDB sees “positive movements” starting but warns fats remain under “severe pressure.”

- SMP and cheddar show early stabilisation. AHDB reports SMP up £80 (5%) to £1,810/tonne in January; cheddar recovered £30 to hit £2,860/tonne. But AHDB cautions that “stabilisation should not be mistaken for recovery.”

- Milk deliveries versus year-ago gauge supply-side pressure. With volumes running nearly 5% above the prior year heading into spring flush, processing capacity stays strained through May.

- ASCA activity tells you whether the regulator has any bite. If formal complaints stay in single digits through April while prices sit below the cost of production, the framework isn’t working as Parliament intended.

Why Nobody’s Talking

Here’s the part that doesn’t show up in market reports: why you’re not hearing individual farmers’ stories.

The producers getting hit hardest—the ones sliding toward exit—are the least likely to speak publicly. In farming culture, financial distress still feels like personal failure. Going on record about contract pressure invites lender scrutiny, community judgement, and processor retaliation.

As NFU Scotland’s Bruce Mackie put it in December 2025: “The dairy supply chain depends on farmers being able to plan and invest with confidence. Sudden, unjustified price drops damage that confidence and threaten not just individual businesses but the resilience of Scotland’s rural economy and food security.”

ASCA built confidential channels precisely because farmers fear reprisals. That’s the right protection—but it also keeps the pain invisible. Processors see aggregate data across their supplier network. Individual farmers see only their own situation and wonder if they’re alone.

You’re not. The aggregate numbers—nearly 5% oversupply, butter down more than half, costs near 49ppl against prices in the low-to-mid 30s—represent thousands of operations running the same brutal calculations.

What This Means for Your Operation

If you’re on an aligned retail contract: Your immediate exposure is limited. Don’t waste the breathing room. Build cash reserves and pay down debt—the cushion you create now determines your options when conditions shift.

If you’re not aligned with 6+ months of cash, you’ve got time to watch. Track these triggers:

- Bulk cream dropping toward £1,000/tonne signals more farmgate pressure

- UK deliveries staying 5%+ above year-ago into spring signals capacity strain

- AHDB language shifting from “pressure” to “recovery” signals inflection

Book your lender scenario conversation before April 1.

If you’re non-aligned and have less than 6 months of cash on hand, the math is unforgiving. Run your exit threshold calculation this week. Have the lender conversation now. If two warning signs fire together—cash flow negative, cream still sliding, deliveries elevated—your decision window is closing fast.

Key Takeaways

- At current price and cost levels, the gap between aligned and non-aligned contracts can reach 14–15ppl—roughly £175,000–£187,500 a year for a 500-cow, 1.25M-litre operation.

- Contract auditing is intelligence, not leverage. You may not change the terms, but you can understand where the landmines are.

- Risk is shifted onto your books across seven areas: indemnification, quality discretion, volume penalties, delayed payments, confidentiality, notice asymmetry, and dispute barriers.

- Exit decisions come with a 12-month lag under FDOM notice rules. Staging preparation preserves options without starting the clock.

- Every credible forecast points to H2 2026 at the earliest for meaningful recovery. AHDB: stabilisation “should not be mistaken for recovery.”

- When culling to compress costs, cull genetically—not just economically. Protect your herd’s trajectory for the recovery.

- Cash runway is the bottom line. Under six months at current prices means fundamentally different choices.

Your contract didn’t create this oversupply. It didn’t crash butter prices. But it decides which side of that £175,000–£187,500 divide you’re standing on while you wait for conditions to turn.

Pull out your contract this week. Work through the checklist.

Which side of the gap are you on?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Why the Smartest Dairy Operators Are Unlocking Over $150,000 in Potential Returns While Others Get Blindsided by Market Chaos – Arms you with a specific ROI roadmap for automation and precision nutrition. You’ll gain concrete methods to capture $150,000 in hidden returns, turning operational expenses into a competitive advantage while neighbors wait for the market to recover.

- 2026 Dairy Rally Or Dead-Cat Bounce? The Risk and Margin Math Behind Today’s Wall of Milk – Exposes the “wall of milk” threatening 2026 margins and delivers the math needed to survive it. This strategy session breaks down global supply shifts, helping you position your operation to thrive when the current rally inevitably fades.

- Bred for $3 Butterfat, Selling at $2.50: Inside the 5-Year Gap That’s Reshaping Genetic Strategy – Reveals how to navigate the dangerous five-year lag between genetic selection and your milk check. You’ll gain a new selection strategy that prioritizes economic indices over volatile component premiums, future-proofing your herd’s long-term profitability.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.