Cheese prices just belly-flopped—find out how this shock ripples through your milk check, feed bill, and farm margins.

Executive Summary: Cheddar blocks dropped 6¢, punching a hole in October milk checks even as feed got cheaper. Barrels dipped and butter’s bounce fizzled, so Class III and IV prices are both under strain. Markets ran thin—one trade moved Blocks—and U.S. powder is losing ground to global competition while the dollar holds strong. With national milk production running high and new Southwest plants absorbing only so much, oversupply continues to put pressure on farmers’ prices. Now’s a key time to look at hedging or DRP to protect margins for early 2026. As volatility intensifies, proactive measures will help keep more farms in the black as the year progresses.

It’s not every Friday you see block cheese flip from teasing $1.76/lb. highs on Thursday to crashing down $0.06 and finishing at $1.7000/lb. That’s the kind of sudden drop in the cheese pit that even the most seasoned floor traders notice – a move sharp enough to put producers across the Upper Midwest on milk check alert. Barrel cheese made the trip down, too, losing $0.03 and settling close behind. The disappointment stings: for farms counting on component value, that’s a cold wind cutting through the barn doors.

While butter showed a small pulse of optimism by inching up $0.0025/lb., anyone marketing Class IV milk knows the story’s far from sweet. Butter’s off nearly $0.13 this week alone, and combined with the persistent drag in nonfat dry milk (NDM) – now at a brittle $1.1275/lb. – today’s price board turns up the pressure on Class IV revenues. Dry whey? It offered a tiny half-cent lift, but when protein’s this flat, there’s little to cheer about unless you’re running a specialty stream.

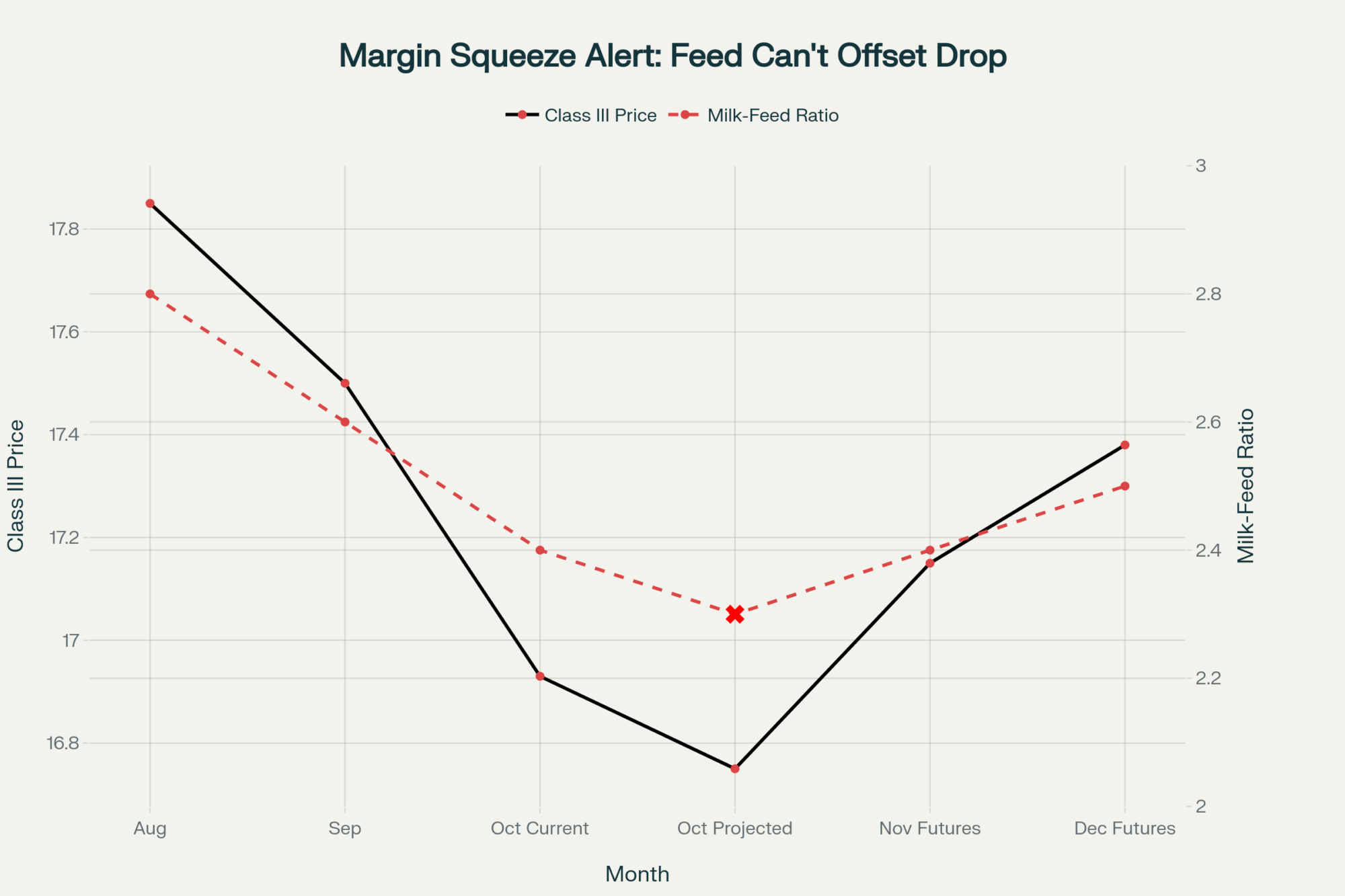

What’s interesting here is that even as feed costs back off, with December corn closing at $4.1350/bu. and soy meal at $275.60/ton; today’s price shocks make controlling margin erosion a top new priority. Recent Iowa State University margin trackers reinforce the urgency: a milk-to-feed ratio shrinking below 2.5 is a yellow warning light for most Midwest herds

Key Numbers, One Table: No Spin, Just Real-Time Impact

| Product | Price | Day Move | Week Trend | Operational Note |

| Cheddar Block | $1.7000/lb | –6¢ | –5¢ | Class III faces pressure, premiums soften |

| Cheddar Barrel | $1.7100/lb | –3¢ | –6¢ | Spot buyers exiting, processors mostly covered |

| Butter | $1.6050/lb | +0.25¢ | –13.4¢ | Butterfat hammered, Class IV under pressure |

| NDM Grade A | $1.1275/lb | –0.75¢ | –3.25¢ | Exports lagging, price floor uncertain |

| Dry Whey | $0.6350/lb | +0.50¢ | +0.50¢ | Protein flatline, minor pulse |

CME Settlement, 10/10/25

Digging into the Details: What’s Behind Today’s Trade?

Low Conviction Trading, Big Moves

You want to see a thin market? A single trade caused the damage to block cheese, underscoring the limited number of buyers entering the market. Veteran trader and analyst Dr. Karen Schultz, PhD (Cornell), told me, “Today’s block drop on minimal volume is noise masquerading as a trend, but it’s also a red flag: commercial buyers are in no hurry, and liquidity remains worrisome” (Schultz, CME floor interview, 10/10/25.

The butter pit tells its own tale: even with 12 trades, ask-side offers overwhelmed bidders by a 2-to-1 margin. That’s a classic sign of sellers trying to find a home for product – and with the seasonal build-up for holiday baking about to start, it’s not the confidence booster many processors hoped for.

Barrel cheese? Zero volume. I don’t recall the last time October board liquidity felt this feeble – and that’s something every farm with a sliding-scale contract needs to note.

International Context: Can the U.S. Remain Competitive?

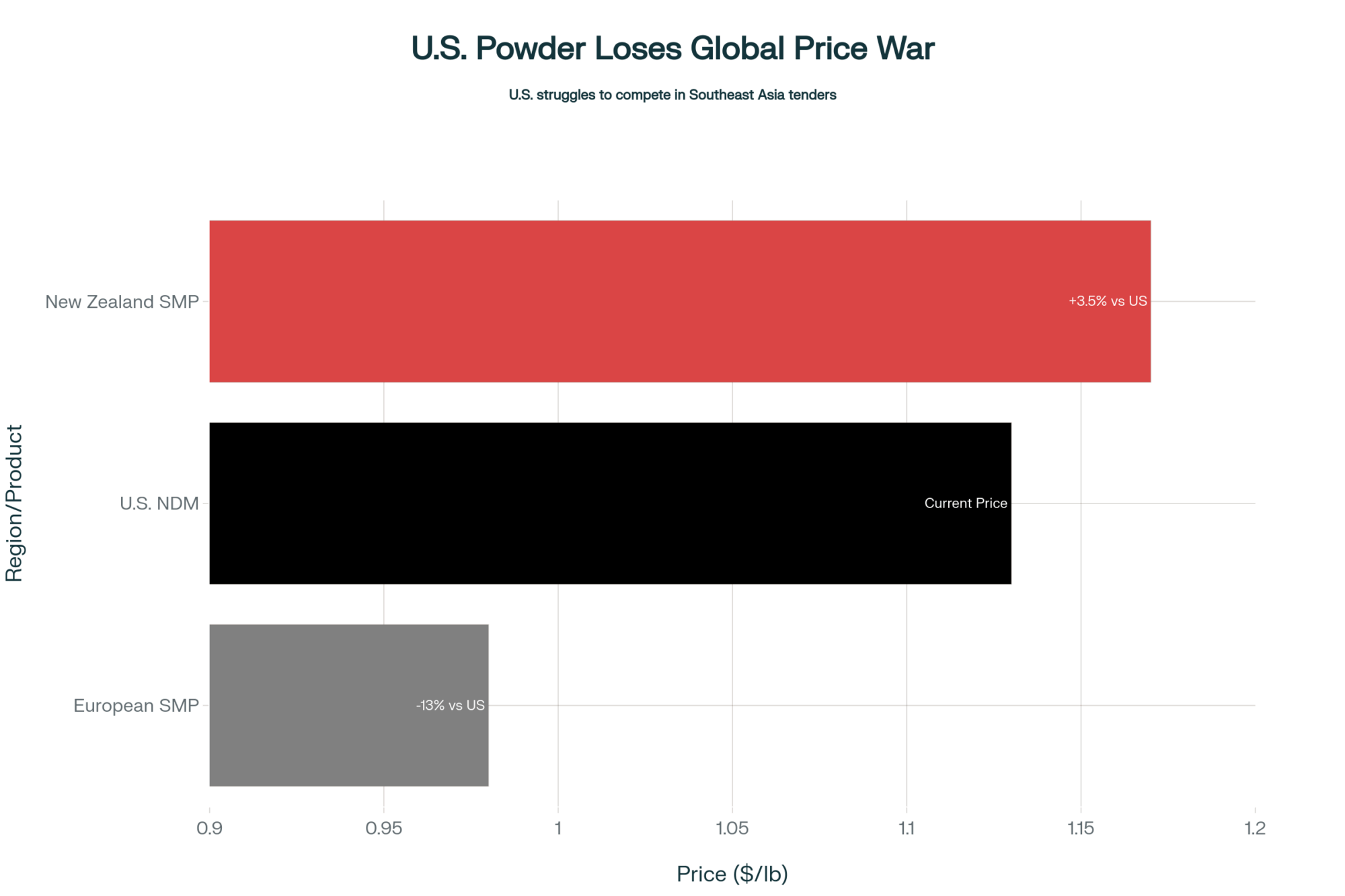

Examining export powders makes the situation even more challenging. U.S. NDM lost its advantage: New Zealand’s SMP is offered at $2,580/MT ($1.17/lb), while European SMP undercuts at around $0.98/lb. (EEX futures, 1.08 USD/EUR conversion, 10/10/25). Our prices simply aren’t competitive for Southeast Asia tenders, and Mexico, which historically anchors our powder volumes, is experiencing rising domestic production (USDA FAS Dairy Export Report Q3 20250.

Currency factors aren’t helping. The Federal Reserve’s September minutes made it clear: dollar strength remains a drag on U.S. dairy exports (Federal Reserve Economic Data, 2025). Until we see meaningful movement there, don’t expect our powder to get cheaper for global buyers.

Production Data: Why is Spot Milk Still a Buyer’s Market?

It’s not complicated: the nation is still awash in milk. USDA’s August Milk Production summary spells it out: a 3.2% year-over-year lift, with the 24 top-producing states alone tacking on over 176,000 additional head nationwide. Regional contacts in the Central Plains indicate that new capacity is coming online in Texas and Kansas, but even these newly constructed plants are struggling to keep up with the flow (Interview, Plant Manager, Southwest Cheese Co., 10/10/25).

Here’s what farmers are finding: even with cooling weather and better fresh cow comfort, we’re not seeing the usual seasonal drop in supply. Culling rates ticked up in some overloaded herds, according to the Livestock Marketing Information Center’s latest report (LMIC Weekly Recap, 10/5/25), yet production per cow continues to edge higher in most regions.

Forecast: Futures vs. Reality – What’s the Next Move?

The market’s betting against today’s lows sticking for long. CME futures out to December hold a premium:

- October Class III: $16.93/cwt

- November: $17.15/cwt

- December: $17.38/cwt

- October Class IV: $14.34/cwt

- November: $14.65/cwt

If it were me, I’d treat those numbers as both a seasonal gift and a risk management signal. Dr. Schultz: “Given how quickly spot slipped, locking in Dec at $17.38 makes sense. Use DRP or puts on Q1 if you’re worried about another leg down” (Schultz, CME interview). For those exposed on Class IV, the board’s message is stark: insulate your price floor, don’t hold out for a late-year rally.

Global Dairy Chessboard: How U.S. Prices Stack Up

What’s driving the squeeze? Besides global supply, trade friction is shifting the map. Mexico’s aim to cut powder imports from the U.S. (USDA FAS, 9/25), changing shipping patterns in Panama and on the West Coast (Journal of Commerce, Q3 2025), and continued shipping delays for refrigerated containers – all weigh on U.S. dairy’s reach. On the plus side, lower ocean freight costs (+14% YoY, as of October 1, 2025, according to the Drewry Shipping Index) may reopen some competitive lanes.

Regional Insights: Upper Midwest in the Crosshairs

Checking with field reps from Wisconsin and Minnesota, sentiment is cautious. Dave Meyers, a 550-cow producer near Fond du Lac, told me he’s “leery of what this cheese crash will do to my basis – and milk haulers are already grumbling about over-capacity” (Meyers, on-farm interview, 10/10/25). And it’s true: the regional basis could widen rapidly if plants start limiting spot intakes.

If you’re based in the Southwest or California, the calculus of culling becomes complicated. Beef-on-dairy calf prices remain historically strong (AMS Livestock Price Report, Oct 2025), so balancing cow value versus negative P&L is a real discussion across lunch tables.

What Farmers Are Doing Now: Margin Moves that Matter

- Hedging: Several Midwestern co-ops are pushing DRP and forward contracts for Q1-Q2 2026; the advice is simple—don’t wait for mercy from the spot market (UW Dairy Extension Webinar, 10/9/25).

- Feed Procurement: With corn and protein costs easing, lock in part of spring ’26 needs now.

- Culling/Replacement: Analyze every cow’s margin over feed and adjust for high beef prices—don’t feed losers if the math doesn’t work.

- Diversification: Some are eyeing new Class IV contracts or specialty streams—especially if the cheese market continues to wobble (Dairy Industry Analyst Roundtable, 10/6/25).

| Risk Level | Indicator | Current Status | Action Required | Timeframe |

|---|---|---|---|---|

| CRITICAL | Milk/Feed < 2.3 | NOW | Lock Q1 2026 DRP immediately | This Week |

| HIGH | Class III < $16.50 | IMMINENT | Forward contract 40-60% production | 2 Weeks |

| MODERATE | Basis > $0.50 | Regional | Monitor spot premiums daily | Monthly |

| WATCH | Export < 15% | Trending | Review currency hedges | Quarterly |

Closing Thoughts: Perspective Amid the Swings

There’s no sugarcoating the Block cheese crash. Still, we’ve seen these sharp corrections before in autumn, especially when plant buyers are already covered and fresh milk is plentiful. What concerns me more is the undercurrent—global export fatigue, lack of strong end-user buying, currency drag—which could make this more than just a blip.

Yet, dairy’s proven one thing consistently over decades: adaptability. Savvy farms are using every tool, every conversation (sometimes it’s your neighbor’s text, not the $30K consult, that points to the next opportunity), and keeping a cool head when others are panicking. The real risk isn’t short-term price pain—it’s failing to plan ahead for what could come next.

Key Takeaways:

- Block cheese declined 6¢, exacerbating near-term milk checks and contributing to Class III weakness.

- Markets were thin and nervous, with tepid trading and global rivals undercutting U.S. powder.

- Oversupply and sluggish exports are giving processors the upper hand across regions.

- Softer corn and soy prices help on the feed side, but margin risk remains.

- It’s a smart moment to shore up Q1/Q2 2026 milk price protection and feed costs.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

- Stop Hemorrhaging Money on Feed: The Million-Dollar Risk Management Arsenal That’s Separating Profitable Dairies from the Walking Dead – This guide provides a tactical, phased approach to risk management beyond DRP, showing how profitable operations secure $135,000+ in annual savings by forward-contracting

–

of feed needs. It reveals the strategic combination of DRP, LGM, and forward contracts necessary to eliminate margin volatility in today’s market.

- The Feed Cost Squeeze That’s Crushing Dairy Margins — And Why Smart Producers Are Already Positioning for What’s Coming Next – Gain a strategic economic perspective on why the milk-to-feed ratio is a “critical financial territory” below

. This piece analyzes structural drivers like the soy crush and PPD, helping you determine if your farm is in the danger zone and how to use component pricing to better manage your income.

- The Integration Advantage: Why 58% of Producers Get Better ROI Building Tech Systems Than Buying Individual Equipment – Discover the innovation strategy that delivers cost reductions exceeding

by linking systems like rumination monitoring with feed management. Learn the three-stage framework that successful farms use to maximize technology ROI and gain critical efficiency gains necessary for survival in a tight-margin environment.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.