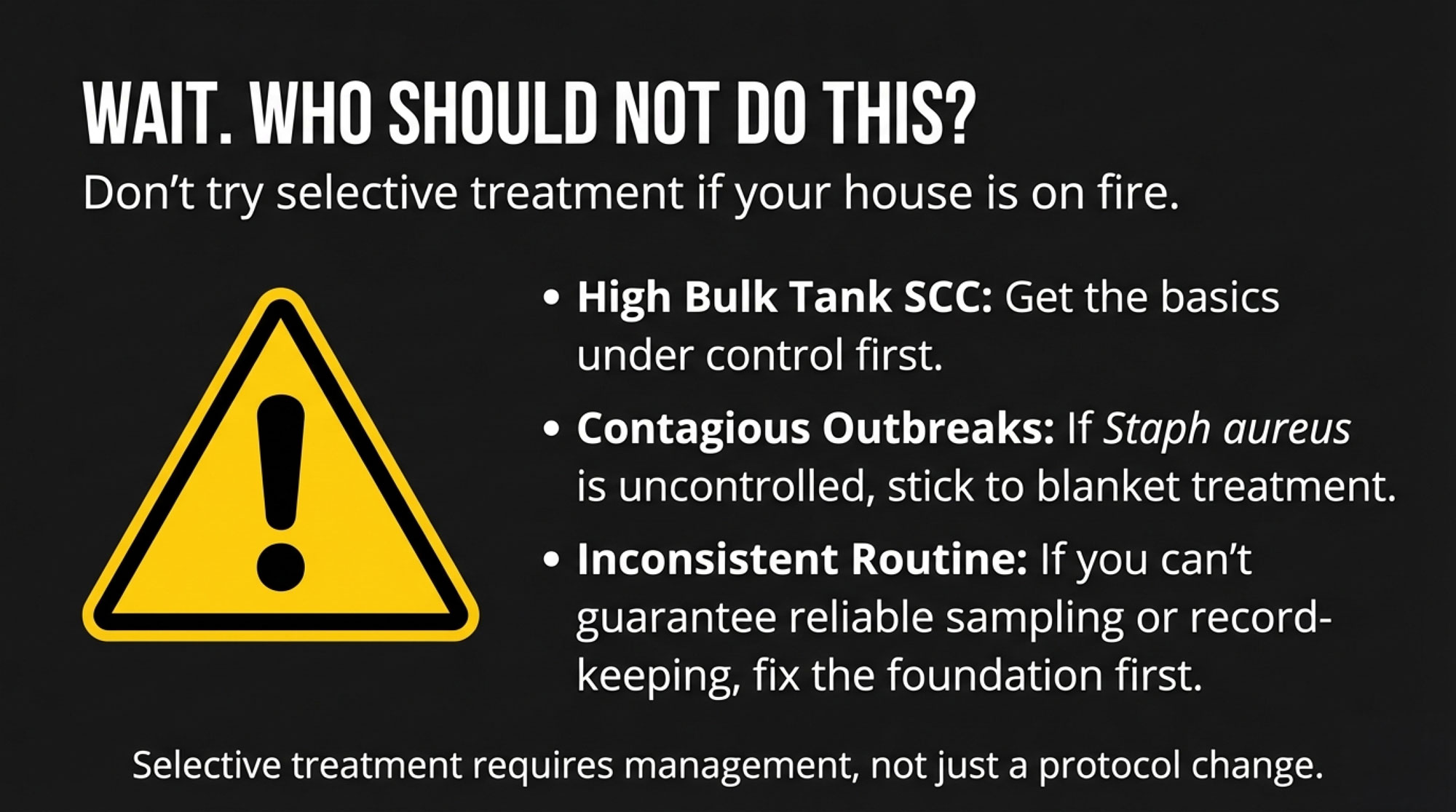

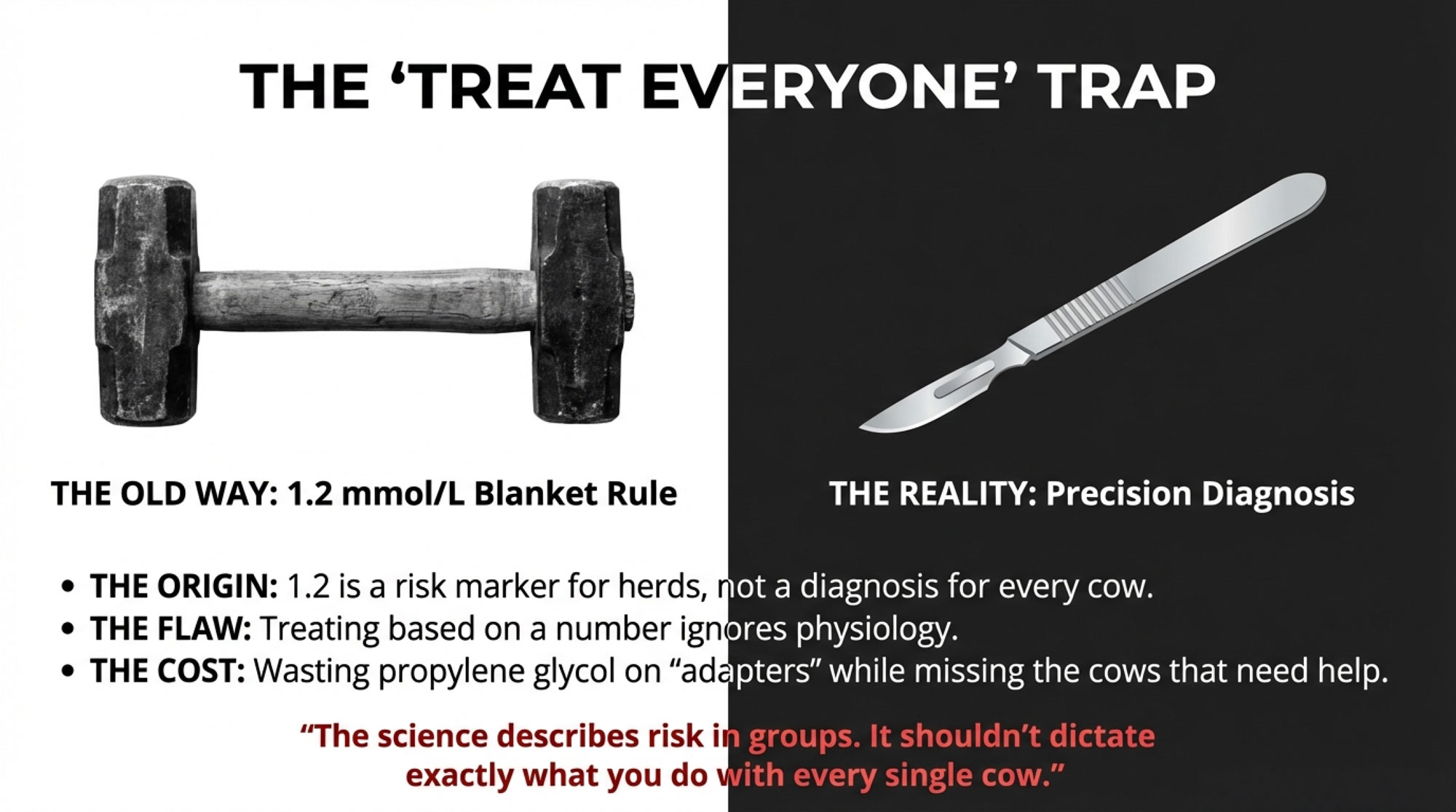

Written SOP on the wall? A 2024 study found that herds with SOPs but no training actually had higher SCC than herds with no SOP at all.

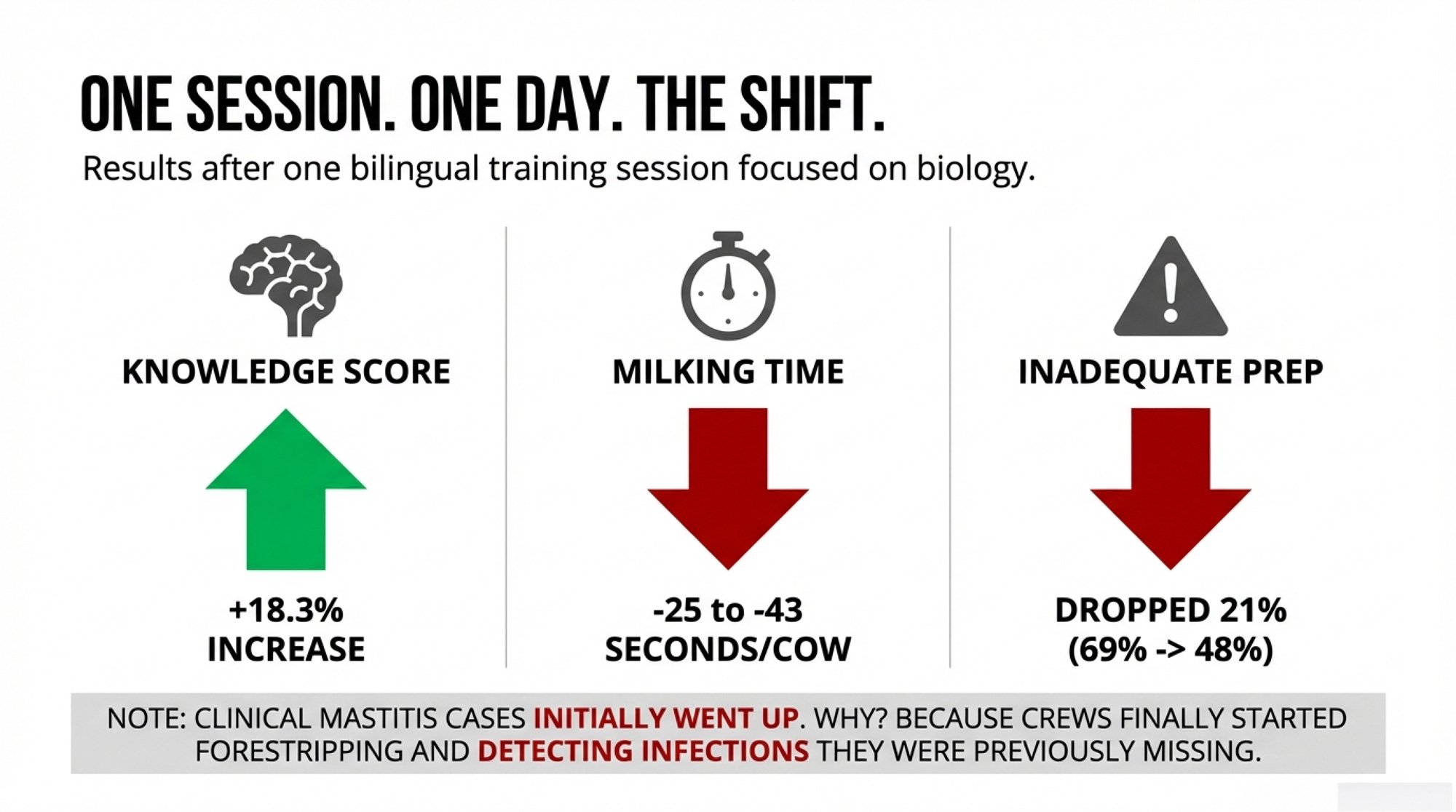

Executive Summary: Most dairies already have written milking SOPs, but Rodriguez’s 16-herd study in Michigan and Ohio showed the people in the pit only averaged 49.3% on a basic routine quiz — and that gap was costing money. One bilingual training session per farm moved knowledge scores to 67.6%, cut inadequate prep from 69% to 48%, reduced missed post-dip coverage, and shaved 25–43 seconds off milking time per cow while stabilizing SCC trends. When you put those shifts beside real-farm results — like an 850‑cow Wisconsin dairy turning a $12,500 training spend into roughly $78,000 in first‑year return while dropping SCC from 245,000 to 175,000 — training stops looking like a “soft” expense and starts penciling out as a $55–$73‑per‑cow‑per‑year opportunity on a 300‑cow herd. The article also leans into the uncomfortable finding that herds with written SOPs but no training actually had higher SCC than herds with no SOP at all, and it ties that to a 38.8% annual turnover rate that constantly erodes protocol compliance. Using national SCC premium grids, mastitis cost data, and regional wage benchmarks, it walks readers through barn math they can plug their own numbers into instead of guessing at training ROI. The piece closes with a four‑path playbook — from UW’s MQUW train‑the‑trainer program to free bilingual online modules and a 30‑day parlor audit — so producers can decide how far to go in formalizing milker training and what kind of return they should expect in their own parlor.

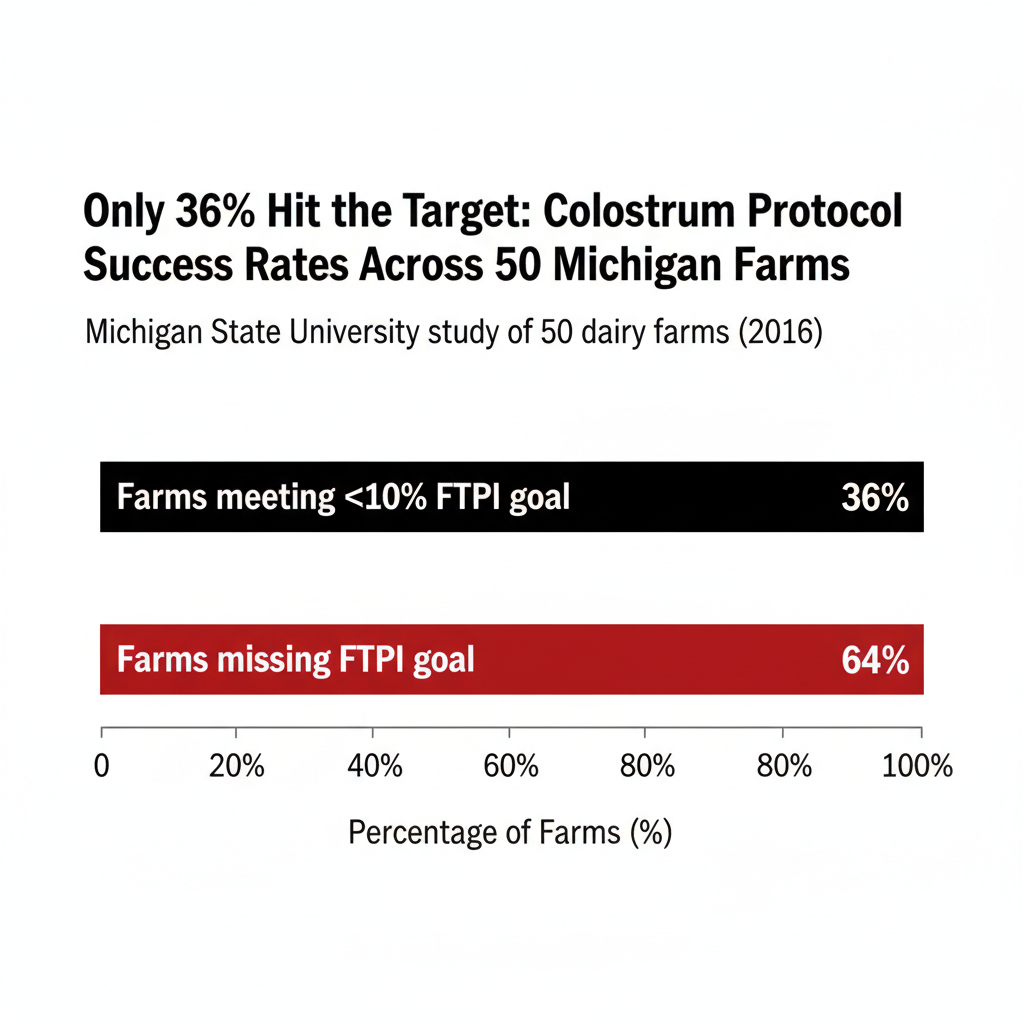

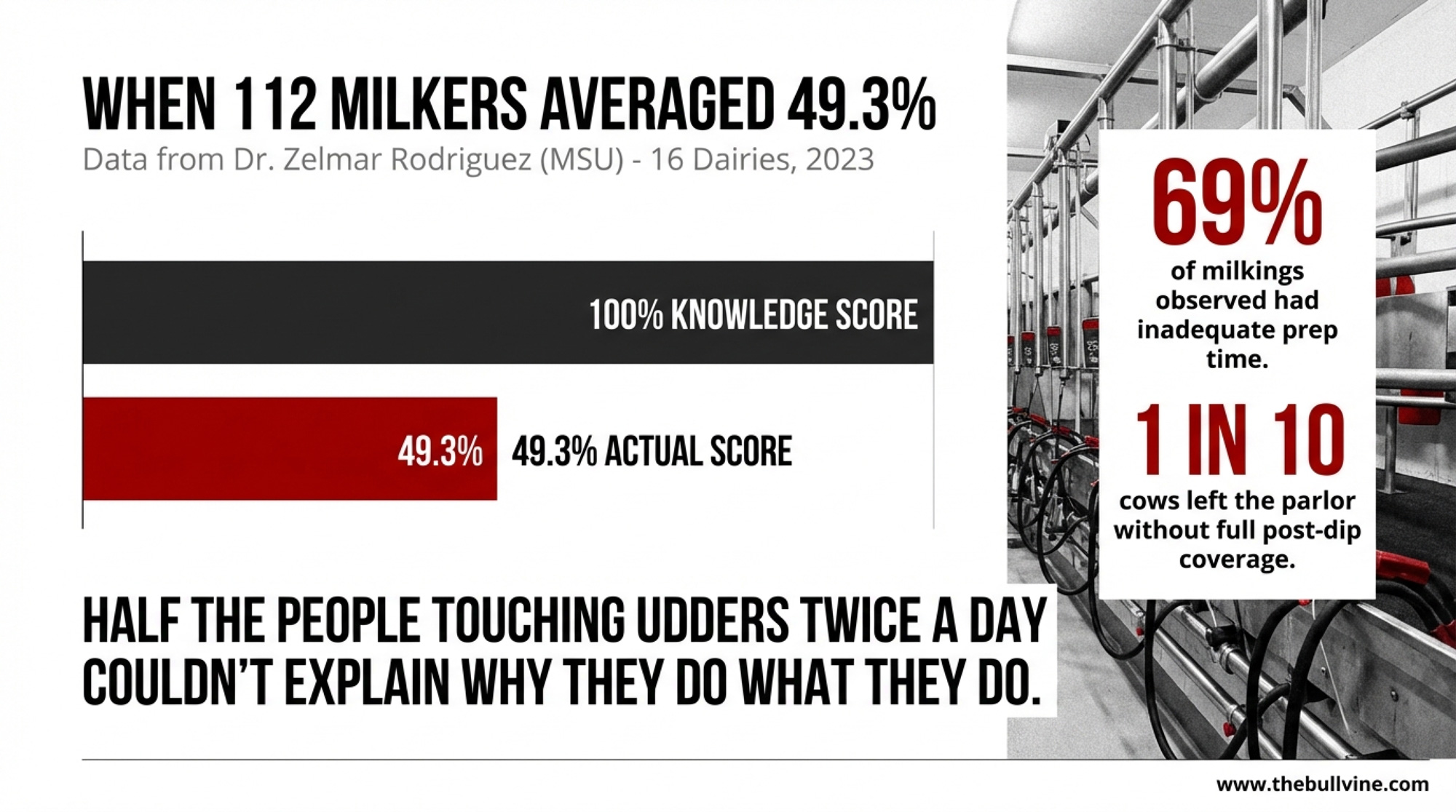

The average score on a basic milking-routine knowledge quiz across 112 parlor workers? 49.3%. That’s what Zelmar Rodriguez — a dairy veterinarian and assistant professor at Michigan State University’s College of Veterinary Medicine — found when he evaluated 16 Michigan and Ohio dairies totaling 17,205 cows between April and September 2023. Half the people touching udders twice a day couldn’t explain why they do what they do. And Rodriguez’s data shows that the gap has a price tag — in SCC premiums lost, mastitis cases missed, and parlor minutes wasted on every shift.

Not a failure rate, either — a group average. Plenty of milkers scored well below that line. “It’s incredible the difference among employees and their learning process. The gap is huge,” Rodriguez said on the Dairy Science Digest podcast in December 2024. These weren’t small pasture herds. Median herd size was 1,101 cows, ranging from 280 to 2,330 lactating, with an average of 15 employees per farm. Study participants were 82% male and 74% Spanish-speaking. Rodriguez told Dairy Global: “People need to know why they have to do what they have been told to do”. His data says roughly half the people in the pit don’t.

Your Written SOP Might Be Making Things Worse

Here’s the part that should make you look at your own parlor wall a little differently.

A 2024 study by Farre and colleagues — published in Veterinary Sciences by researchers from SEGES Innovation in Denmark, the University of Copenhagen, and Wageningen University — surveyed 88 Danish dairy herds with hired employees and parlor or rotary systems. They split farms into three groups: no written milking SOP, a written SOP with no structured training, and a written SOP actively used in training. The results flipped expectations. Herds with a written SOP and no training performed worse than herds with no SOP at all — BTSCC was 21,600 cells/mL higher,and new infection risk was 0.15 percentage points higher. Only herds that actually trained milkers on their SOP saw improvement: a 0.16 percentage-point drop in new infection risk.

Herd Type

Bulk Tank SCC Change

New Infection Risk Change

No written SOP

Baseline

Baseline

Written SOP, No Training

+21,600 cells/mL

+0.15 percentage points

Written SOP + Active Training

Improved

−0.16 percentage points

A binder in English on a farm where most of the crew speaks Spanish isn’t training. It’s wallpaper. New hires figure out within a week which rules on the wall are “real” and which ones everyone ignores. Then they follow the veteran milker, not the laminated sheet.

Rodriguez’s 16 herds fit that pattern. SOPs were posted. Equipment functioned. But when he timed what actually happened in the pit, 69% of milkings fell short on preparation time, and about 1 in 10 cows left the parlor without full post-dip coverage. The routine changed with the crew, not the cow.

One Session. One Day. Here’s What Moved.

Getting farms to sign up was its own challenge. “It wasn’t as easy to get study participants as I thought it would be,” Rodriguez admitted. “They all would say, ‘We just don’t have time'”. Owners came around once they learned the training would only take about an hour.

Each farm got one structured training session — bilingual, practical, and built around explaining the biology behind each step of that farm’s milking routine. Rodriguez used the National Mastitis Council’s free online resources to draft a curriculum focused on mastitis identification, risk factors, and proper milking procedures. During the pre-assessment, researchers captured photographs of the parlor being worked on — this helped participants visualize their own farm and better relate to the concepts. Workers and managers reviewed the parlor evaluation together and agreed on adjustments based on Rodriguez’s observations during his first visit.

The crews responded. Employees rated the training 4.5 out of 5 for practical use on their farm. Most were milking technicians (61.1%), and 70% had been on the job for less than 1 year, with a median tenure of just 9 months. “We can’t expect employees to come in with this knowledge,” Rodriguez said. These weren’t lifers. They were the people you’re usually hoping will just “pick it up” from watching.

One practical lesson surfaced everywhere. “Confusion around how to handle abnormal milk was one question that bubbled to the surface on every farm enrolled,” Rodriguez reported. “It is critical that owners or parlor management are present at the training to answer questions just like these that are a bit subjective and vary from farm to farm”.

On the follow-up visit, Rodriguez ran the same checks again:

Metric

Before

After

Change

Knowledge quiz score

49.3%

67.6%

+18.3 points

Milkings with inadequate prep

69%

48%

−21 points

Insufficient post-dip coverage

9.8%

5.9%

−3.9 points

Pre-dip contact time

Below target

+9 sec/cow

Toward 30s target

Proper lag time (60–120 sec)

Baseline

+20% compliance

Improved

Milking time per cow

Baseline

−25 to −43 sec

Fewer re-attachments

One thing caught attention: clinical mastitis cases went up after training. Sounds like bad news — until you think about forestripping. Once milkers actually started stripping out and looking, they caught abnormal milk that had been going straight into the tank.

Two Farms That Actually Ran the Numbers

Before you dig into per-cow math, it helps to see what actual farms saw when they swapped “watch and learn” for real training.

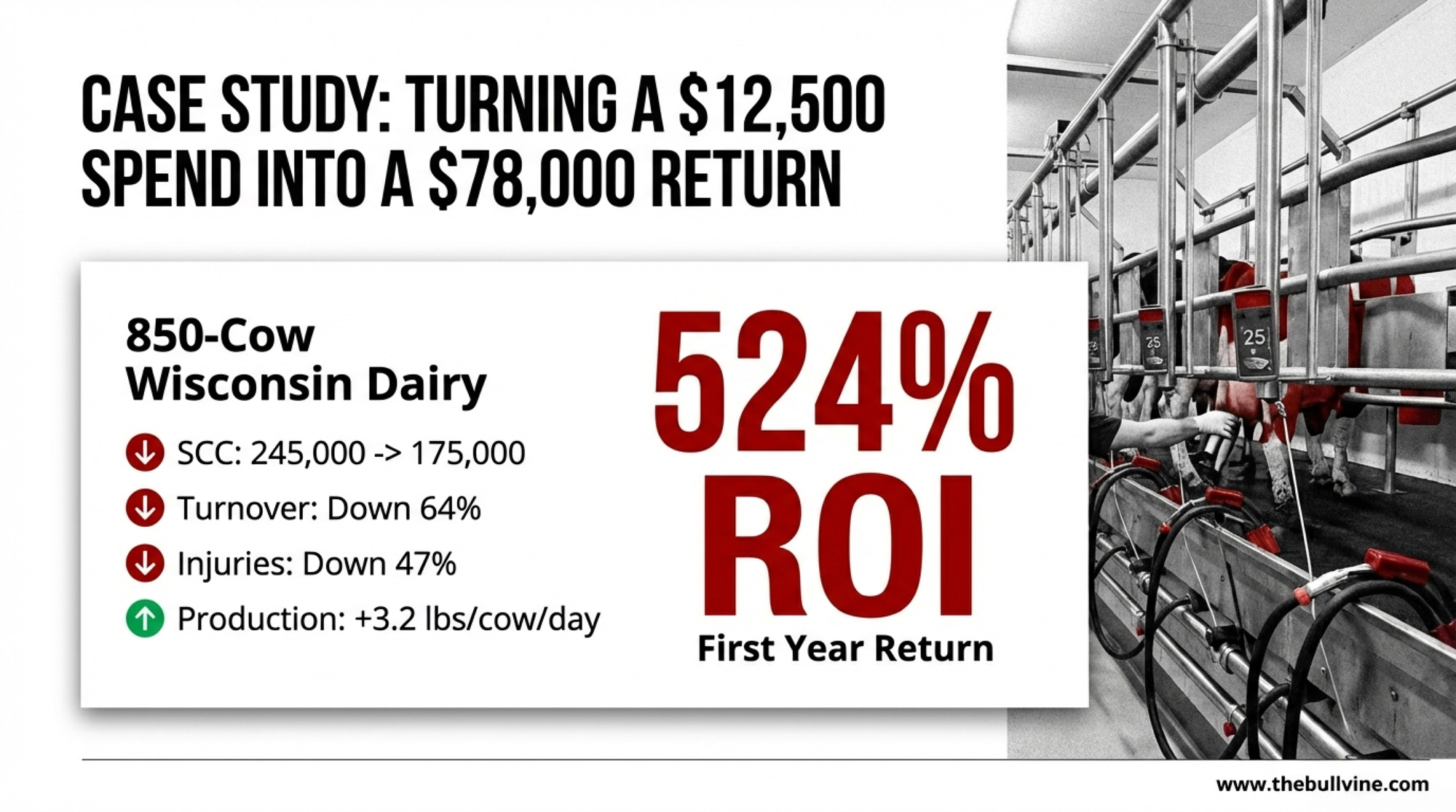

In 2022, an 850-cow Wisconsin dairy invested $12,500 in a bilingual training overhaul — agricultural Spanish classes for management, bilingual signage and SOPs, and monthly bilingual safety meetings with a professional translator.

Metric

Result

SCC

245,000 → 175,000

Employee turnover

Down 64%

Workplace injuries

Down 47%

Production

Up 3.2 lb/cow/day

First-year return

~$78,000 (524% ROI on $12,500)

A second Midwest dairy worked with a Hispanic employee training service. Over nine months, SCC dropped from 325,000–350,000 into the sub-200,000 range. Employee turnover fell from one to two departures a month down to one departure in six months on a 20-person crew.

Farm

Investment

First-Year Return

SCC Change

Turnover Change

Wisconsin 850-Cow

$12,500

$78,000 (524% ROI)

245K → 175K

Down 64%

Midwest Dairy

Not disclosed

Not disclosed

325K → <200K

2/month → 1/6 months

Neither farm saw a magic overnight turnaround. But once milkers understood why they were doing what they’d always been told to do, protocol drift slowed. And the numbers moved.

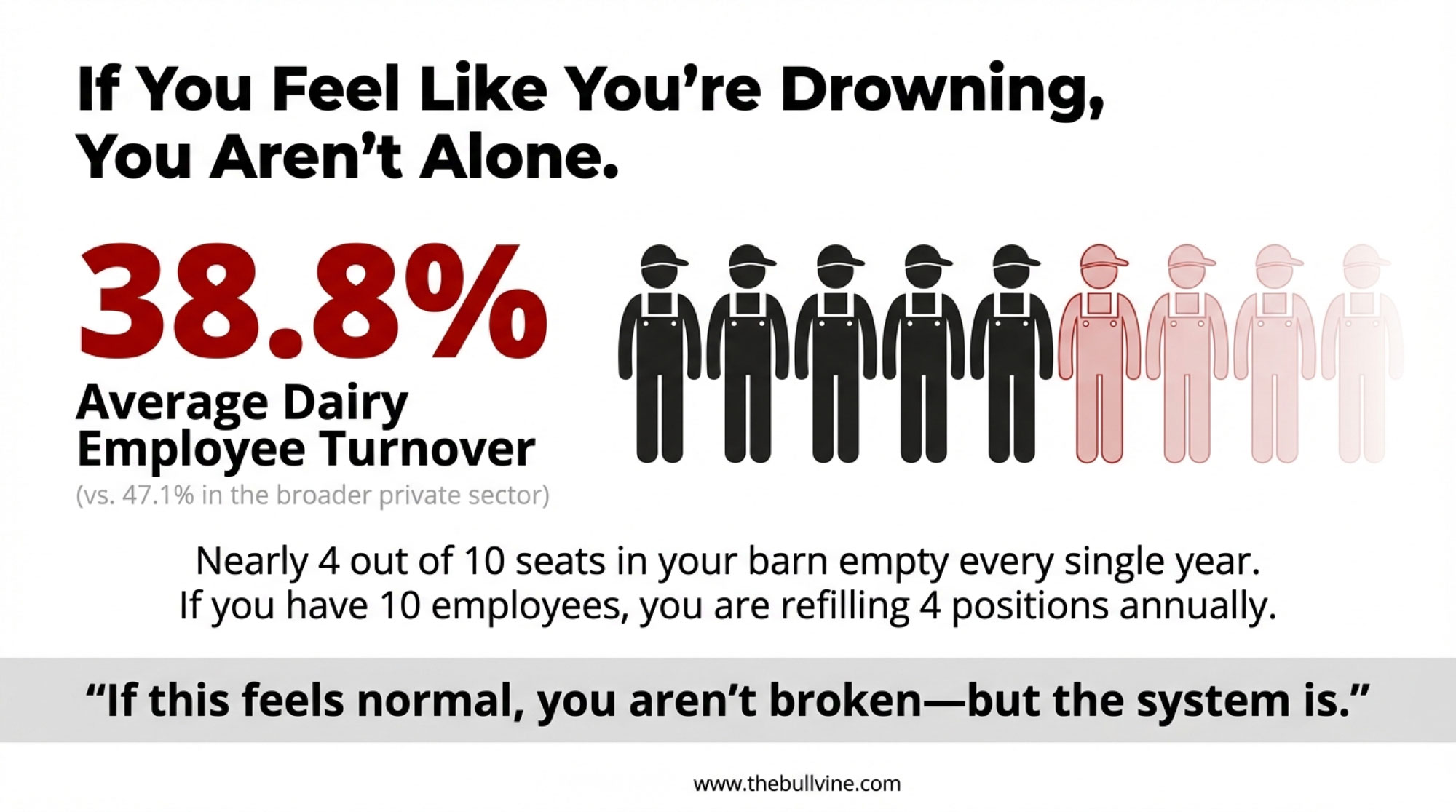

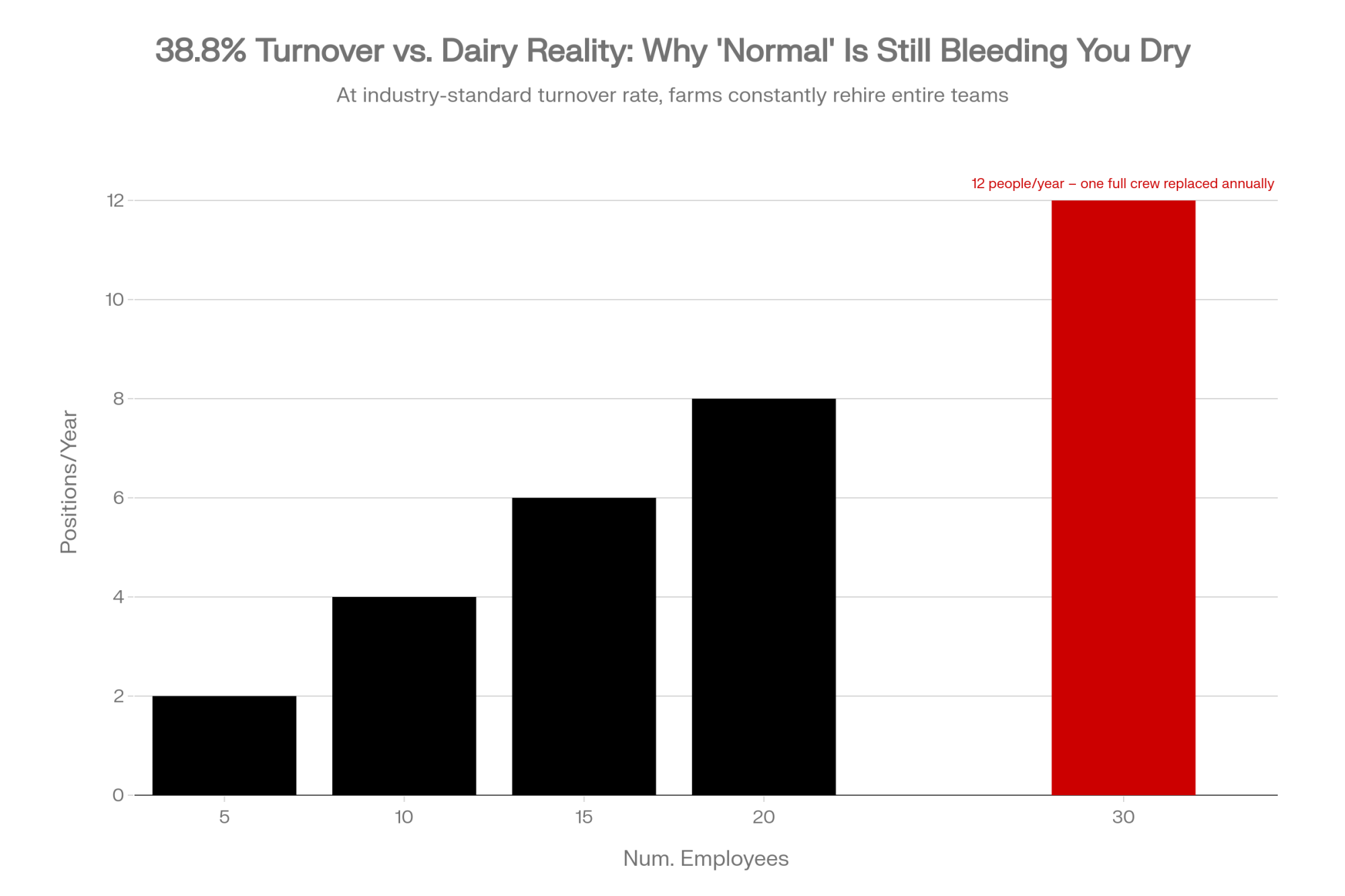

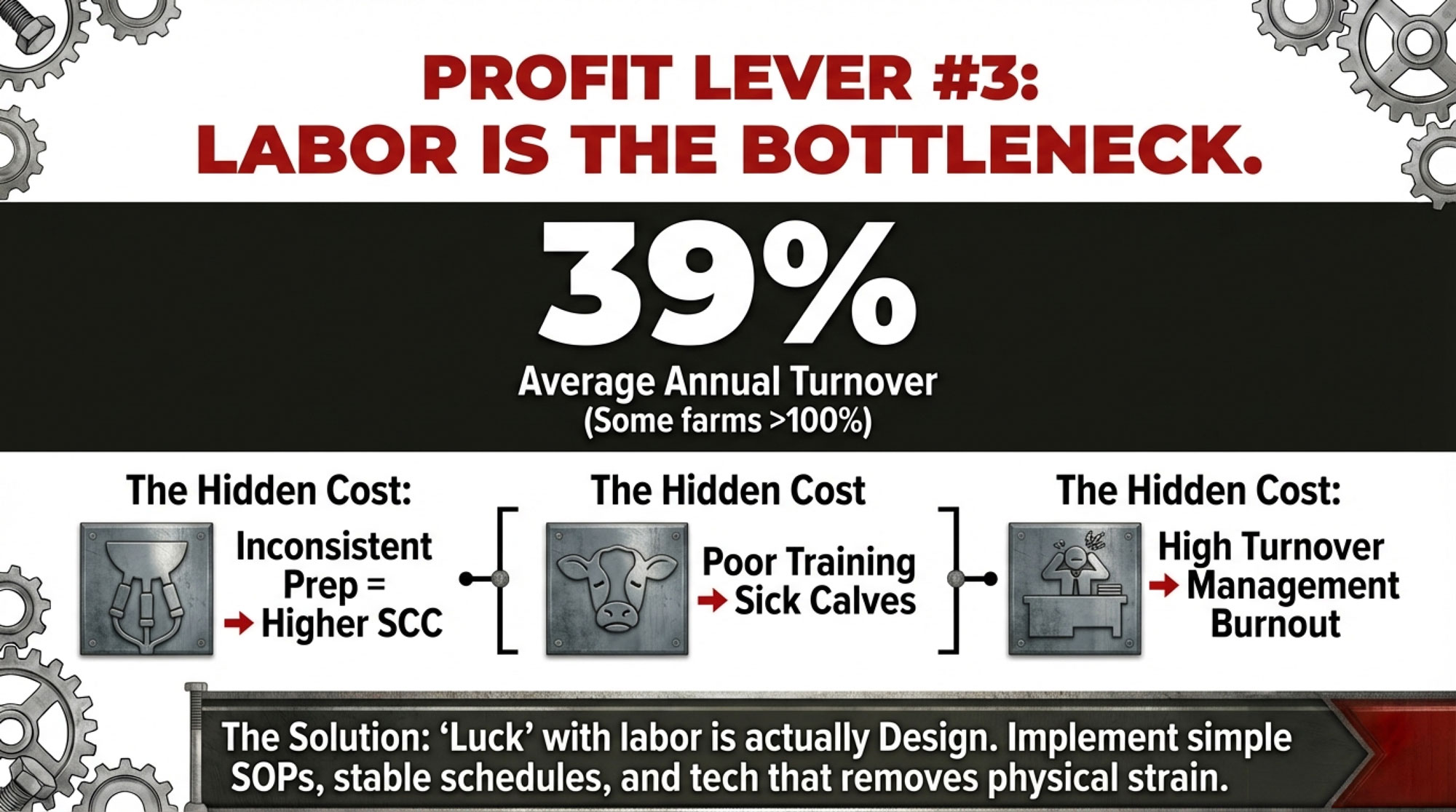

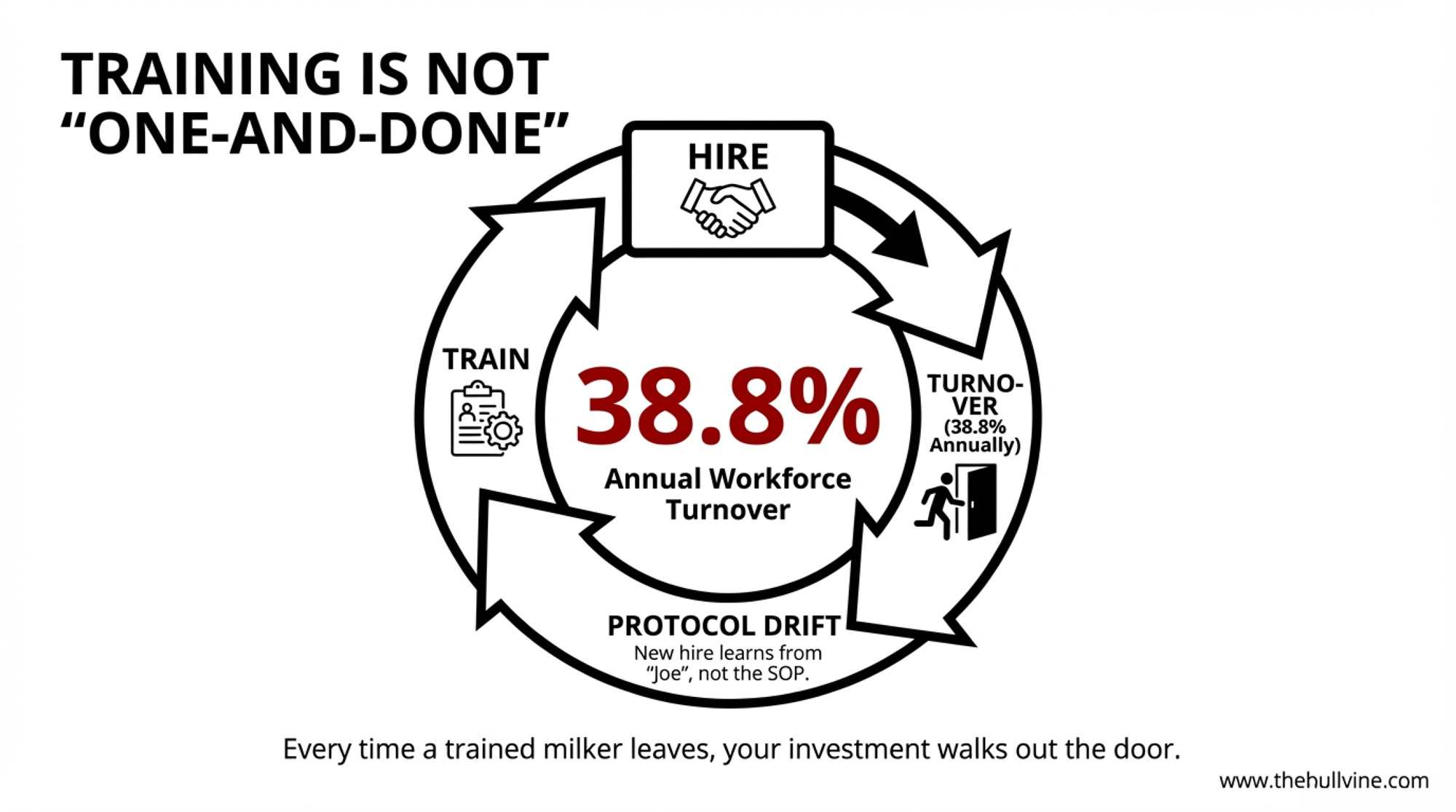

Here’s the part that makes training a rolling cost, not a one-time fix. Nationally, dairy operations turn over 38.8% of their workforce every year. Nearly 4 out of 10 parlor positions are refilled annually.

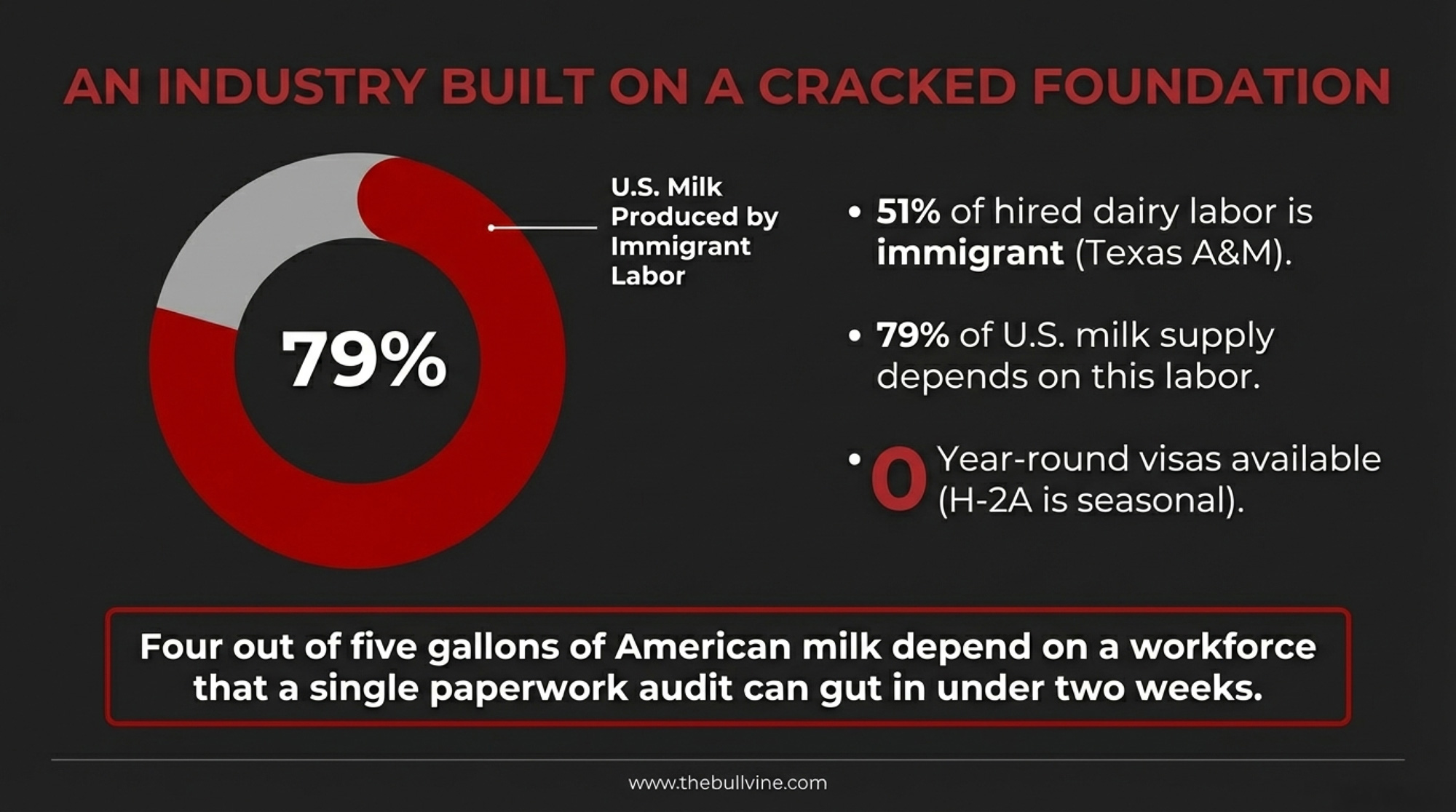

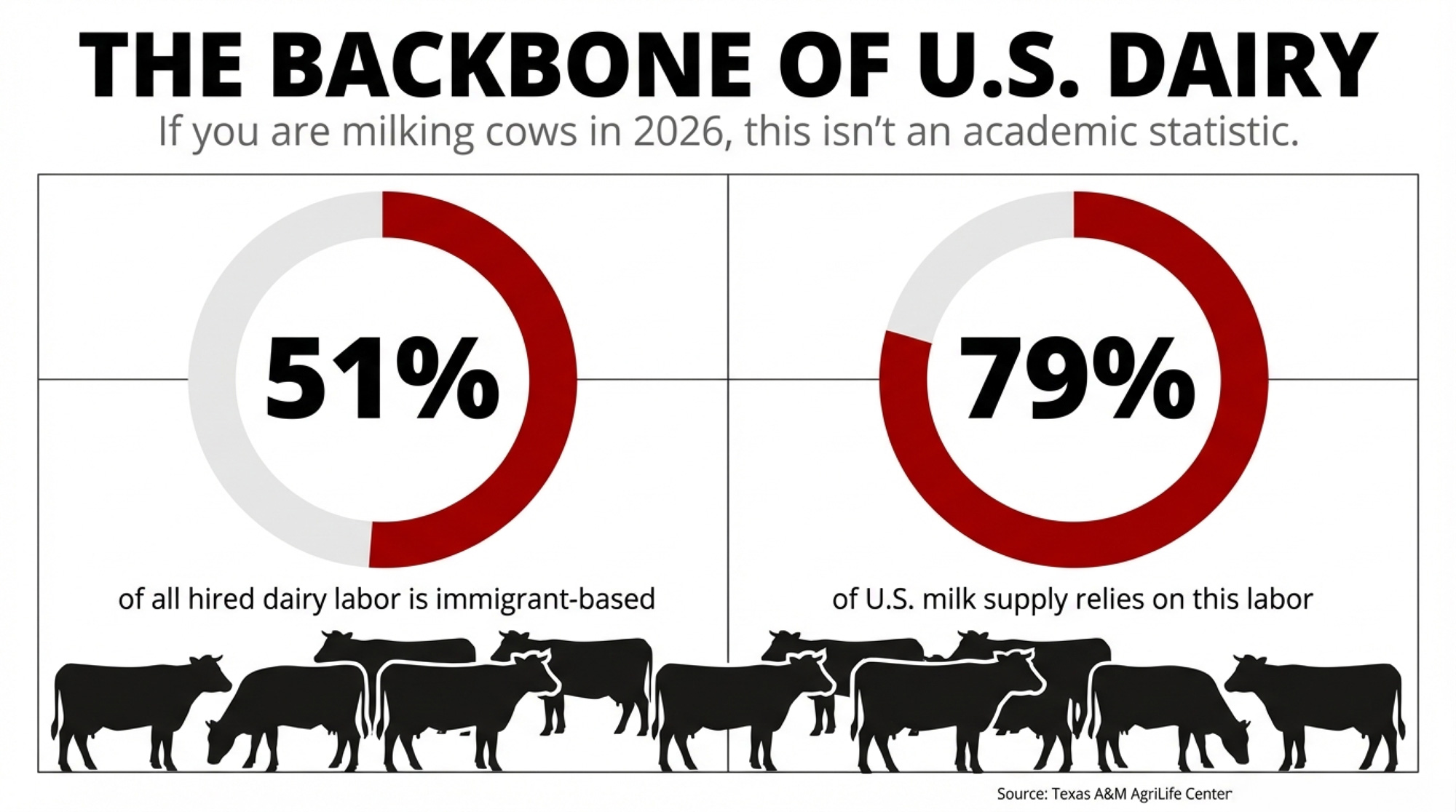

Every time a trained milker leaves, your investment walks out the door — and whoever fills that spot learns more from the coworker beside them than from anything posted on the wall. Think about that next time someone frames dairy’s labor problem as a matter of finding “better” workers. It’s not. It’s about training the workforce you actually have. Immigrant labor provides 51% of all U.S. dairy workers, and dairies employing immigrant labor produce 79% of the milk supply. Jorge Delgado, the on-farm dairy specialist who oversees Alltech’s Training, Talent Development, and Retention Program, said in a February 2024 statement: “Better education and training not only bolster the workforce’s efficiency but also safeguard milk markets and assure consumers that the industry prioritizes animal welfare through rigorous worker training”.

How Much Does Milking Training Actually Save Per Cow?

Rodriguez charted bulk tank SCC over time and saw the trend flatten after training — the seasonal upward creep in BTSCC stopped. Not the dramatic plunge that wins a plaque. But enough to keep herds inside their quality premium range rather than sliding out.

Nationally, the average DHI test-day herd SCC was 181,000 cells/mL in 2024 — the same as in 2023, according to CDCB. Genetics on somatic cell score keep improving. If the national average isn’t budging, the bottleneck isn’t in the semen tank. It’s in the parlor.

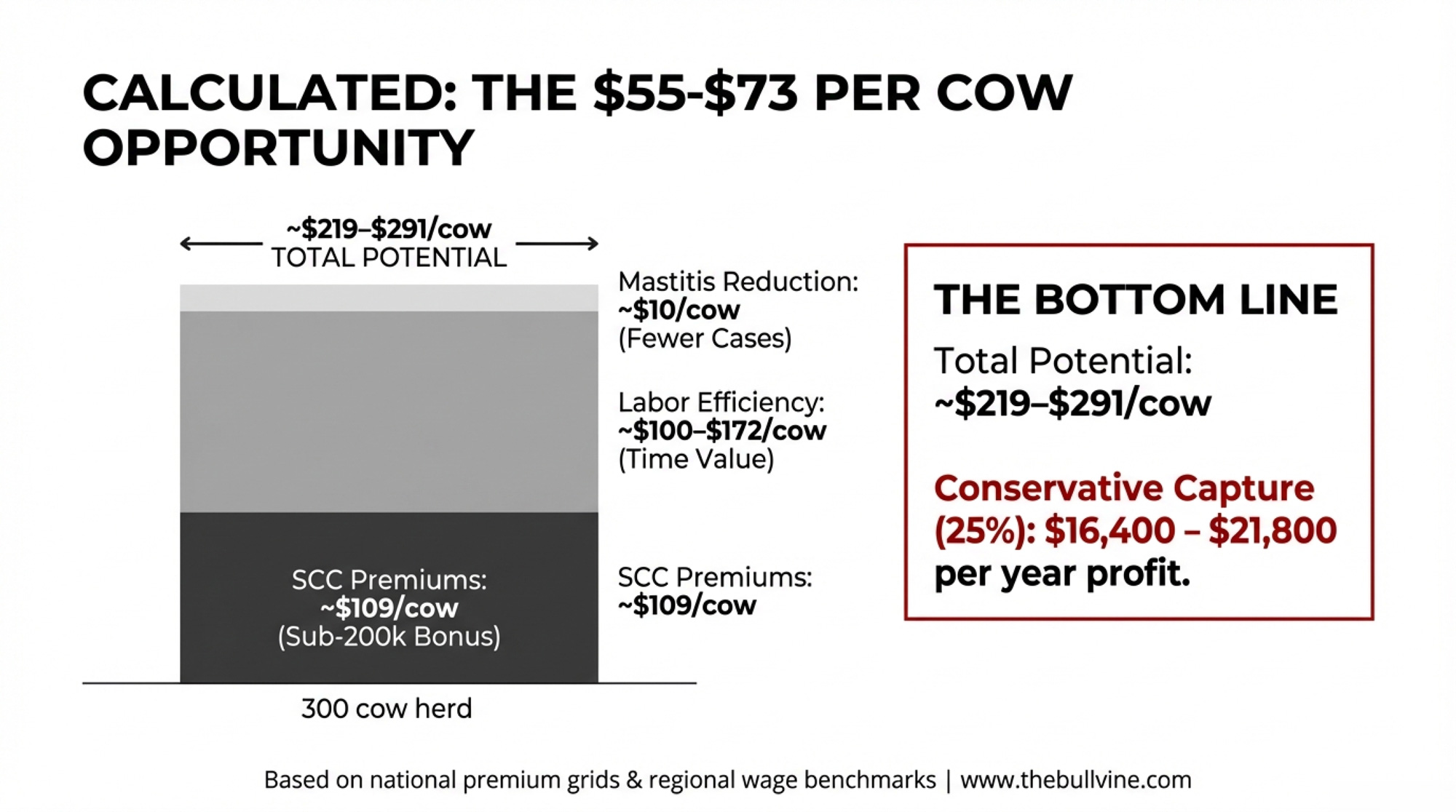

Here’s the barn math on a 300-cow herd shipping 75 lb/cow/day. Swap your own numbers into any line.

Line 1: SCC Premium Protection

Four Federal Milk Marketing Orders adjust milk payments for SCC using a per-1,000-cells/mL variation from a 350,000 baseline tied to monthly cheese prices. Co-ops and processors stack their own quality premiums on top. Herds consistently shipping sub-200,000 SCC milk see premiums in roughly the $0.40–$1.00/cwt range, depending on processor and region.

Your math (conservative, $0.40/cwt): 300 cows × 75 lb/day × 365 days = 8,212,500 lb = 82,125 cwt 82,125 cwt × $0.40 = $32,850/year≈ $109/cow/year in premium income kept or lost

If your co-op’s grid pays closer to $1.00/cwt for sub-150K milk, triple that line.

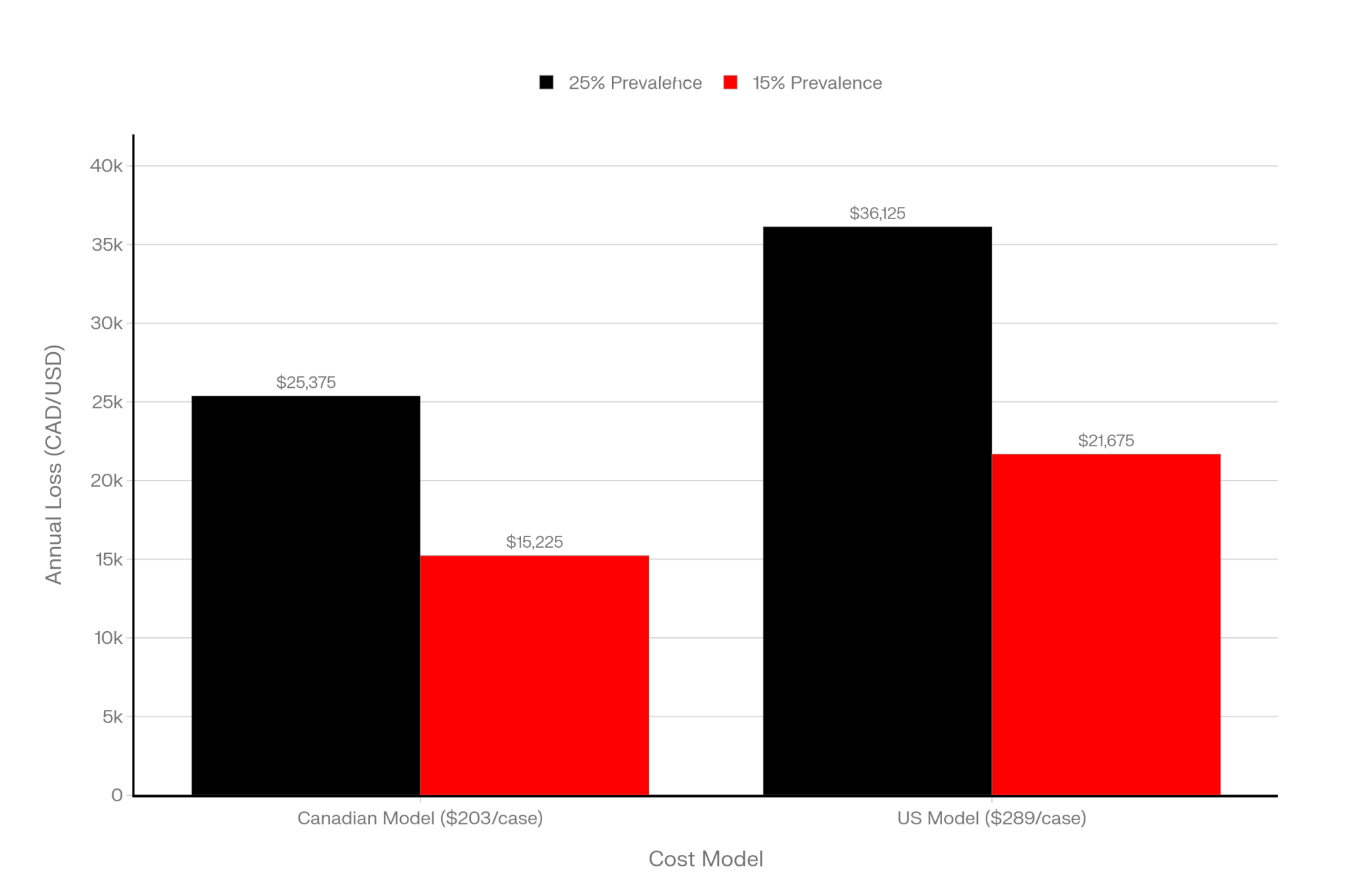

Line 2: Mastitis Cost Reduction

In a separate study, Pamela Ruegg’s group at MSU examined the actual costs of clinical mastitis cases on 37 commercial dairy farms in Wisconsin. Average direct cost: $192 per case, with a range of roughly $120 to $350depending on the farm. Discarded milk accounted for 53–80% of those direct costs. USDA’s NAHMS Dairy 2014 study — the most recent nationally representative data — found clinical mastitis in 24.8% of cows.

Your math (300-cow herd at national average): 300 cows × 24.8% = ~75 cases/year. If improved compliance trims incidence from 20% to 15%, 15 fewer cases × $192 = $2,880.Total: ~$2,880/year ≈ $10/cow/year

A note on that 20%: Rodriguez’s study actually showed clinical mastitis cases going up after training — because crews were finally detecting them through forestripping. The case-reduction math is a projection of what should happen over 6–12 months as better detection leads to earlier treatment and fewer chronic infections. Track your own before-and-after numbers rather than assuming this figure.

Separately, Ruegg found that each unnecessary treatment day costs about $65 in discarded milk and drugs. If you and your vet tighten treatment protocols alongside parlor training — a different conversation, but one that pairs well with what we covered in our mastitis overtreatment piece — the savings stack.

Line 3: Labor Efficiency

Two sources report different figures for the milking time reduction Rodriguez measured, and both are credible. MSU’s own summary and the Dairy Global report both show a 25-second reduction per cow — attributed specifically to fewer re-attachments. Hoard’s Dairyman, reporting on Rodriguez’s December 2024 appearance on the Dairy Science Digest podcast, cites an average reduction of 43 seconds per cow, with no change in employee performance. The broader figure may reflect total milking time savings, including prep efficiency gains alongside re-attachment reduction.

Your math (300-cow, 2× herd — conservative, using 25 sec): 25 sec × 300 cows × 2 milkings = 250 min = 4.17 hours/day 4.17 hrs × 365 = 1,521 hours/year 1,521 hrs × $19.70/hr (USDA Lake Region livestock wage, May 2025) = $29,960≈ $100/cow/year in time-value

If the 43-second figure applies to your operation: 43 sec × 300 cows × 2 milkings = 430 min = 7.17 hours/day 7.17 hrs × 365 = 2,617 hours/year 2,617 hrs × $19.70/hr = $51,555≈ $172/cow/year in time-value

Honest catch: “time-value” doesn’t automatically land in your checking account. Crews get paid for the shift, not by the minute. That time becomes real money when you can milk more cows with the same hours, cut overtime, or eventually trim scheduled labor. A 2022 Cornell-led study by Alanis, Virkler, and colleagues — published in JDS Communications— evaluated milking training across 15 farms in northern New York and found equipment-related problems that milkers should have detected and reported on 14 of 15 farms, with inadequate milking routines flagged on 13 of 15. That’s the kind of inefficiency where saved seconds start converting to real dollars once the crew knows what to watch for.

Nobody captures every dollar. But even a quarter — $55 to $73/cow, or $16,400 to $21,800/year on 300 cows — comes in against a training spend that tops out around $6,000. The 25% figure is editorial judgment, not a study finding. Your actual capture depends on how consistently you maintain the new routine through turnover cycles.

What Does a Structured Milking Training Protocol Look Like?

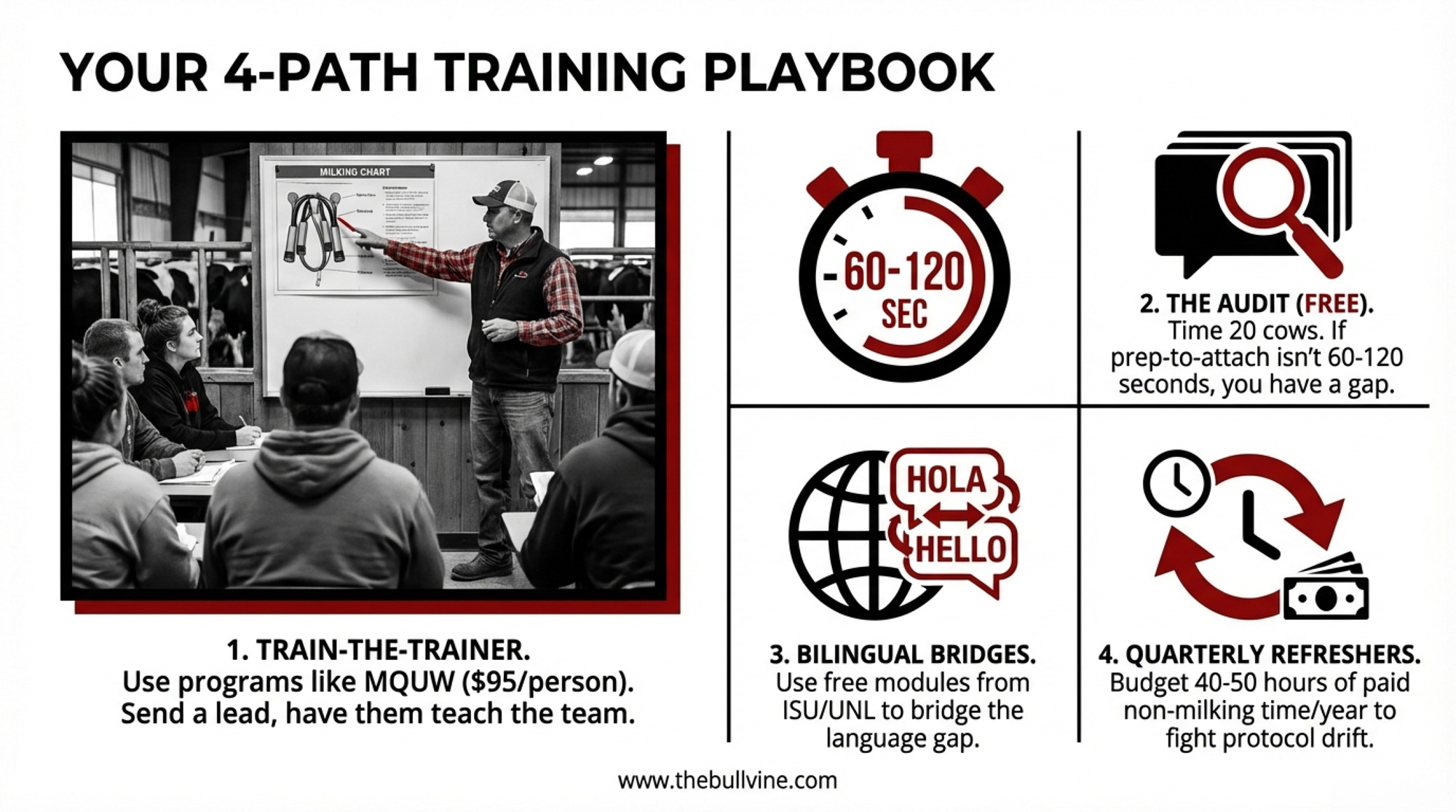

UW–Madison’s Milk Quality from the Udder World (MQUW) trainer certification program runs $95 per person. That covers a self-paced online course (about 2 hours across five modules), a one-day in-person workshop, lunch, laminated parlor training materials with QR codes linking to short educational videos, and certification. Sessions run in English one day and Spanish the next.

Location

Spring 2026 Dates

Luxemburg

Feb 18–19

Madison

Mar 18–19

Abbotsford

Apr 1–2

Fond du Lac

Apr 7–8

De Soto

Apr 29–30

(The Luxemburg session begins February 18 — check dairy.extension.wisc.edu for remaining seats. Four more sessions run through April 30.)

It’s a train-the-trainer model. You send your parlor manager, a bilingual lead, or maybe yourself—and they bring the knowledge home to coach everyone else. Rodriguez himself used the NMC’s free online resources to build his curriculum. On-farm, the pattern is simple: explain the biology, demonstrate on actual cows in your setup, then stand in the pit and coach real-time until the new routine holds.

Realistic annual training budget (300-cow herd, 15 milkers)

Item

Cost

MQUW fees — 3 trainers × $95

$285

Wages + travel for trainer attendance

$1,000–$1,500

On-farm rollout (trainer time + milker hours during coaching)

$2,000–$3,000

Quarterly refreshers (fight turnover drift)

$1,000–$2,000/yr

Total

$2,000–$6,000

Most of that is your own payroll, not program fees.

Can’t get to Wisconsin? Iowa State University Extension and the University of Nebraska–Lincoln Dairy Extensionbuilt a free online milker training program in English and Spanish at go.iastate.edu/milkertraining. Each module has Spanish-language videos with English subtitles and quizzes in both languages with Spanish audio. The Alltech–FARM Program also launched bilingual cow-handling modules in 2024 that cover stockmanship fundamentals. Neither replaces someone standing beside a new milker in your pit — but both are a massive step up from “follow Joe.”

Farms with 3+ milkers, bilingual crews, need for repeatable internal training

Free Bilingual Online Modules (Iowa State/UNL)

$0

Self-paced (videos + quizzes in English/Spanish)

Step-by-step videos, quizzes, certificates

Bridge option for farms that can’t attend in-person training this year

DIY 30-Day Parlor Audit

$0

3 milkings across shifts (stopwatch + notepad)

Baseline data: lag time, post-dip coverage, re-attachments, forestrip compliance

Immediate baseline before committing to training spend—start here

On-Farm Custom Training (Rodriguez Model)

$2,000–$6,000/year

1-hour initial session + quarterly refreshers

Bilingual, farm-specific, coached in your parlor, ongoing reinforcement

Farms ready to formalize training as a rolling annual investment

What This Means for Your Operation

Path 1: Enroll in a train-the-trainer program like MQUW — the $285 path. Makes the most sense if you’ve got more than one person milking and you want the routine done the same way on every shift. At $95 per person for a full day, it’s one of the lowest-cost ways to address parlor consistency. The catch: if your only certified trainer quits, your training program walks out the door. Send at least two people — three if you can — so you’re not starting from zero when turnover hits. And don’t assume robotic milking gets you off the hook. It just shifts the training need from unit attachment to software, alerts, and cow management.

Path 2: Start with a parlor audit this month — no cost, immediate baseline. Grab a stopwatch and a notepad. Spend three consecutive milkings in the parlor across different shifts. Time at least 20 cows per milking from first touch to unit attachment. Score post-dip coverage: full, partial, or missed. Count how many cows aren’t forestripped at all. By the end of that week, you’ll know whether lag time falls within the 60 to 120 seconds that NMC, University of Minnesota Extension, and Penn State Extension all recommend from first tactile stimulation to unit attachment. Frame it for your crew as “we’re checking our system, not checking up on you”—or you’ll create pushback before you even talk about training.

Path 3: Use free bilingual resources as a bridge. If MQUW is out of reach this year, the Iowa State/UNL online milker training gives you step-by-step videos and quizzes in both languages. Neither replaces farm-specific coaching in your parlor. But they’re a real step up from dropping a translated SOP on the breakroom table and hoping it sticks.

Path 4: Post micro-metrics and run quarterly refreshers. Training isn’t one-and-done — especially with 38.8% annual turnover. After your initial push, pick a few visible numbers: prep-time compliance rate, average lag time, dip coverage percentage, and re-attachments per 100 cows. Post them where your crew sees them. Plan a 30–45-minute refresher for each crew every quarter. Maybe 40–50 hours of paid, non-milking time per year across your whole milking staff to keep everyone aligned. Skip the refreshers? Within a couple of turnover cycles, your crew looks a lot like Rodriguez’s study group did on day one.

Key Takeaways

If your herd SCC has stayed flat or crept up while your SCS genetics have improved, the gap is probably in the parlor, not the semen tank. The national DHI average has remained at 181,000 cells/mL over the past 2 years. Pull your last three DHIA tests and see if your trend is any different.

If you’ve got a written milking SOP that nobody has formally trained on in the past 12 months, the Farre et al. (2024) research says you might actually be worse off than having no SOP at all. A binder nobody understands teaches your crew that written rules don’t matter.

Within the next 30 days, run your own stopwatch test. Time 20 cows’ prep-to-attachment intervals on two different shifts. The NMC-recommended target is 60 to 120 seconds from first stimulation to unit attachment. If a significant share of your cows fall outside that window, training — not equipment — is probably where your next dollar should go.

Budget $2,000 to $6,000 per year for structured milking training on a 300-cow herd and compare that to what you spend on genetics, nutrition, and facilities that all depend on consistent milking to pay off.

The Bottom Line

When’s the last time you stood through a full milking in your own parlor and didn’t touch a unit — just watched what actually happens, step by step, across shifts?

Rodriguez did that on 16 farms, scored 112 workers, and measured the gap between what farms thought their milking routine looked like and what was actually happening in the pit. Your bulk tank already knows how consistent your milking routine really is. The question is whether you’re ready to stand in the pit, run the stopwatch, and find out what it would take to close that gap on your operation.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

The 90-Second Milking Window That’s Paying $126,000 – and Beating Every Robot – You’ll gain a surgical method for auditing pit efficiency and capturing six figures in “lost” milk without buying a single robot. This breakdown delivers the exact protocols and ROI math to turn parlor drift into measurable profit.

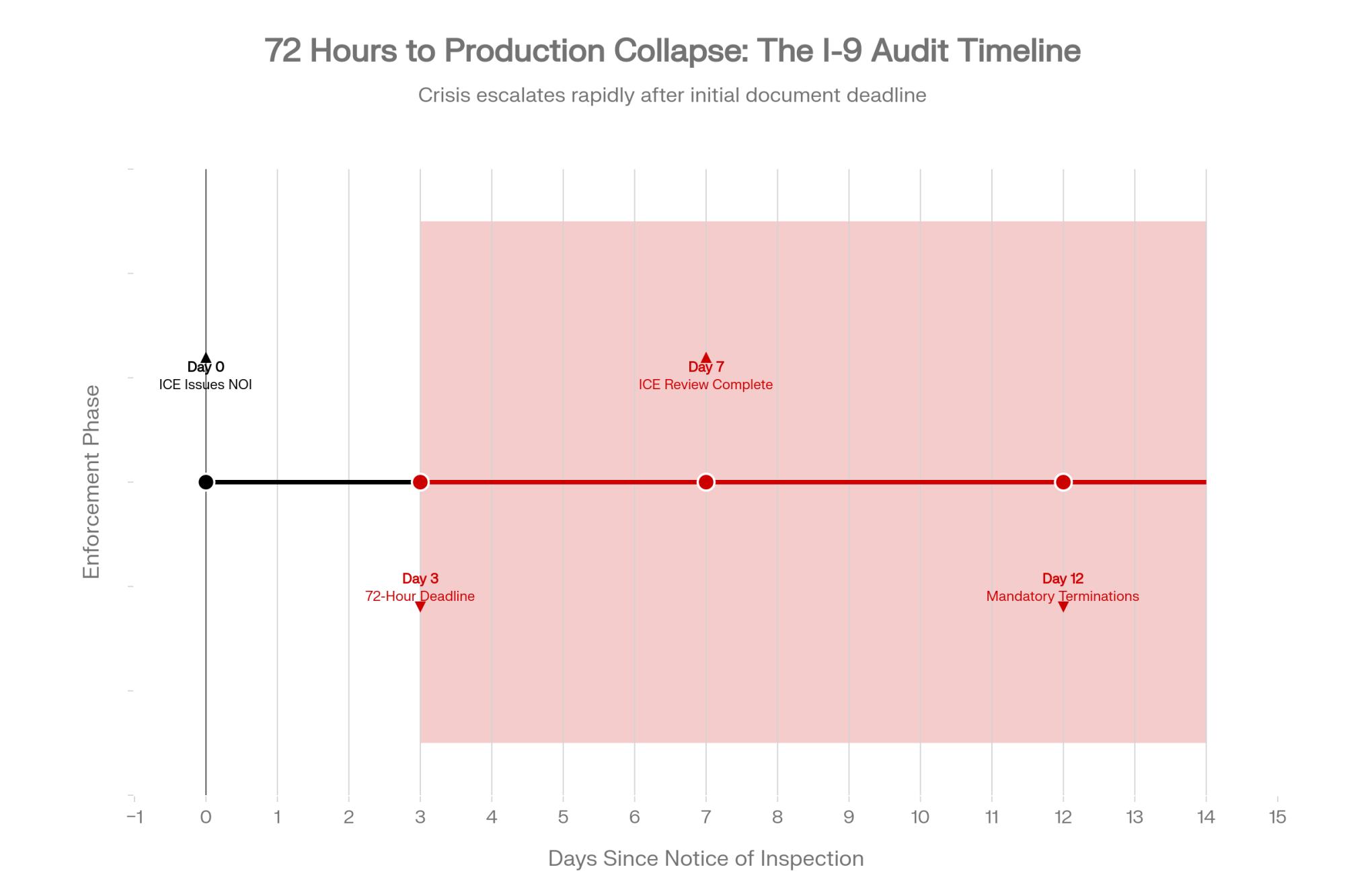

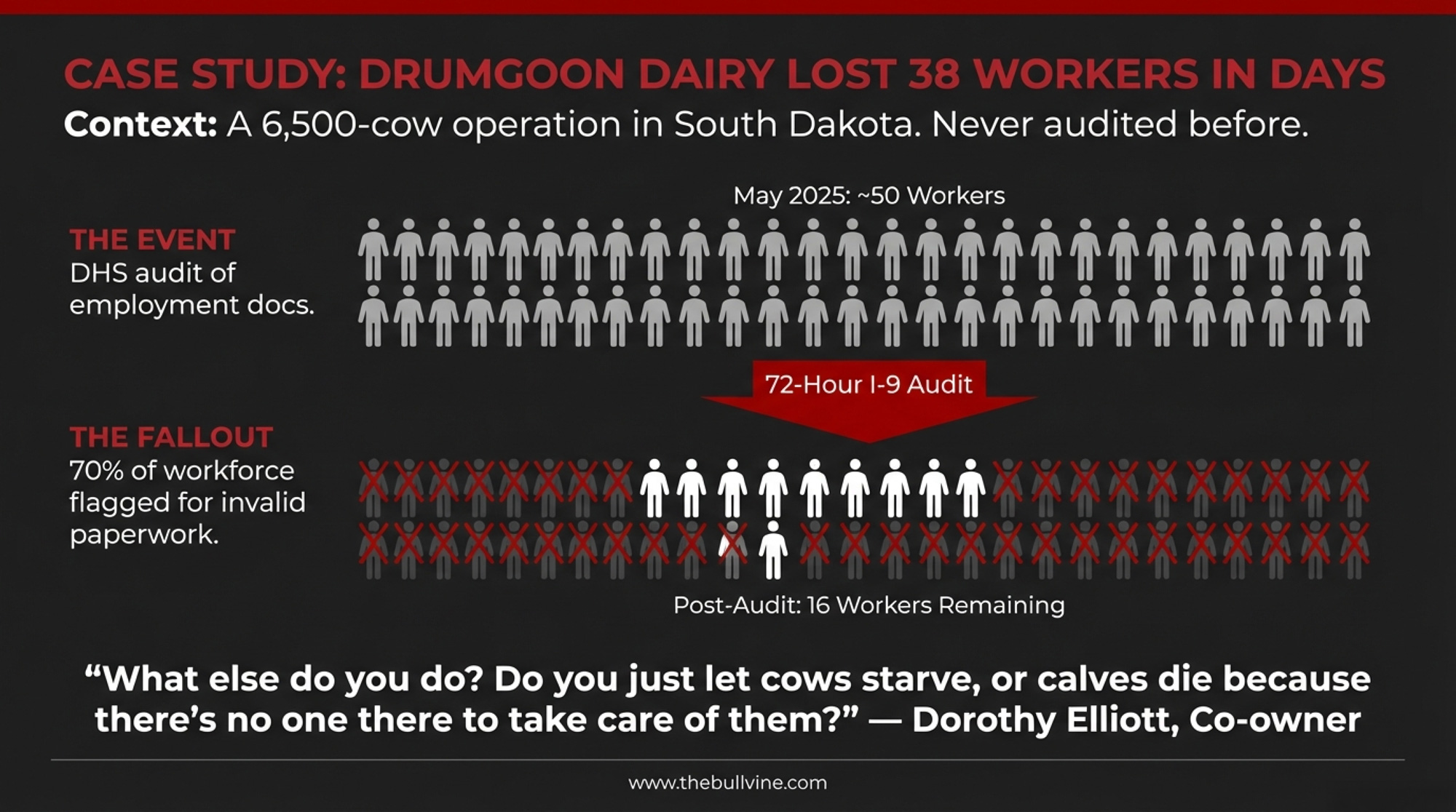

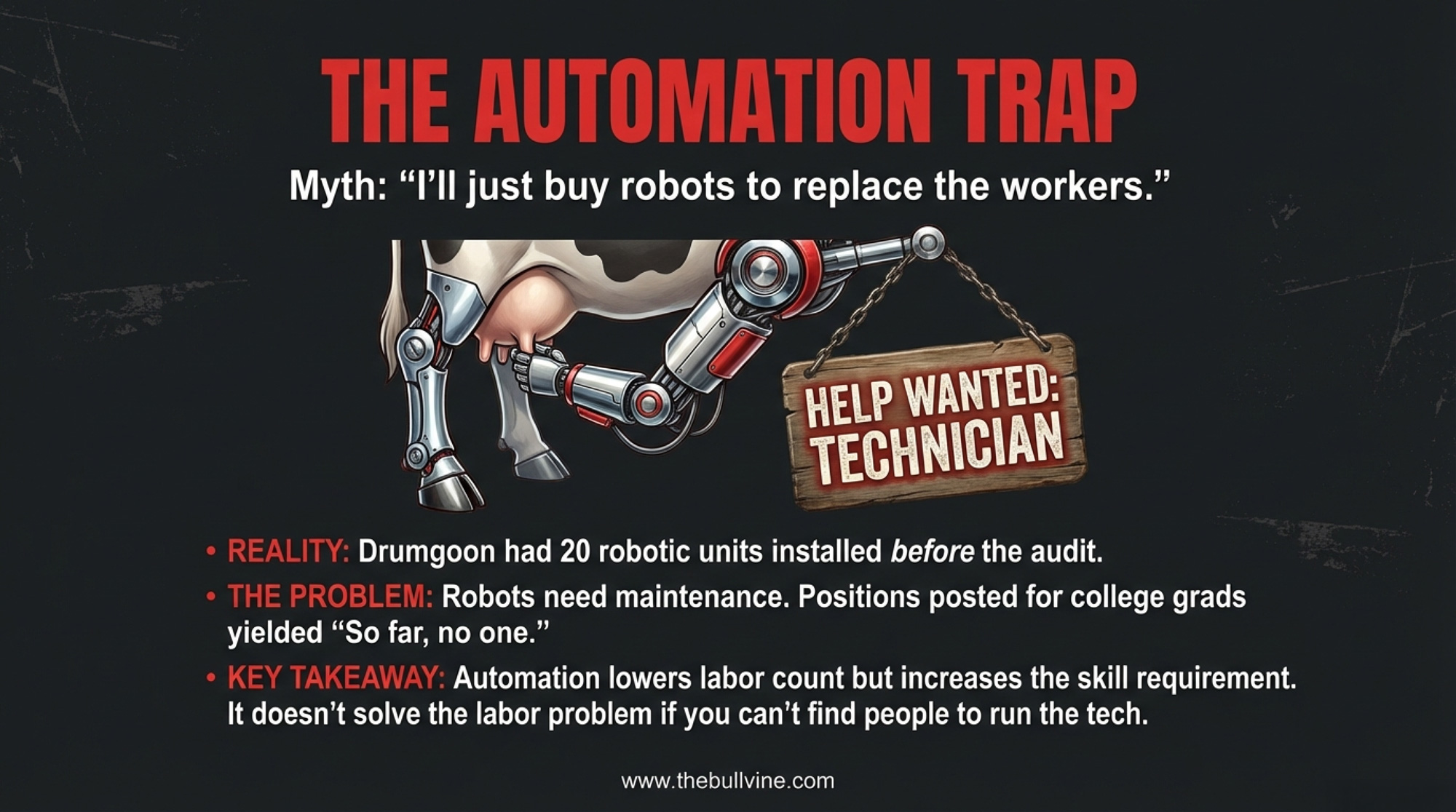

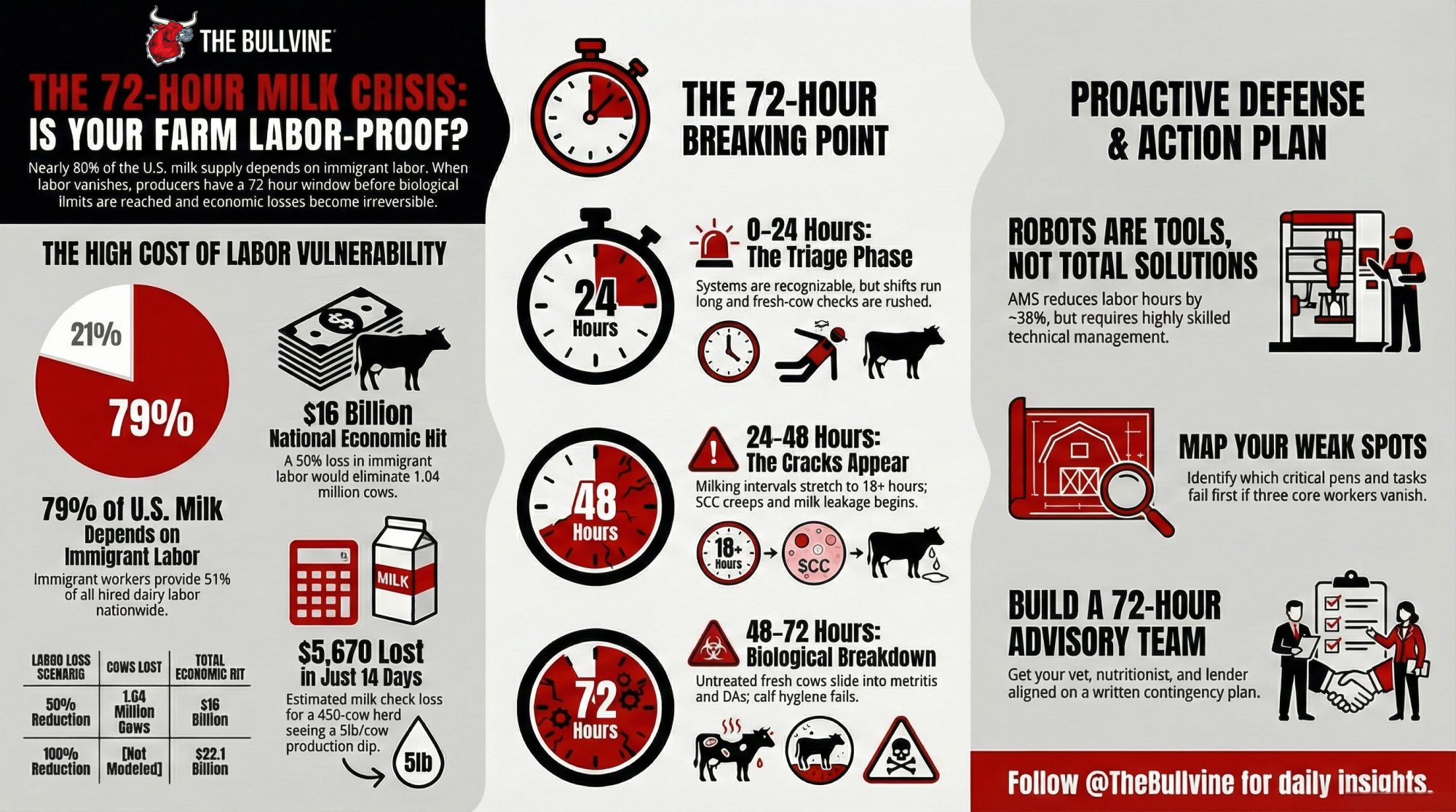

79% of U.S. Milk Runs on Immigrant Labor. If Yours Vanishes, You Have 72 Hours. – This reveals the brutal reality of our industry’s workforce dependence and arms you with a 72-hour survival strategy for labor shocks. You’ll position your operation to weather policy storms while protecting the milk volume currently at risk.

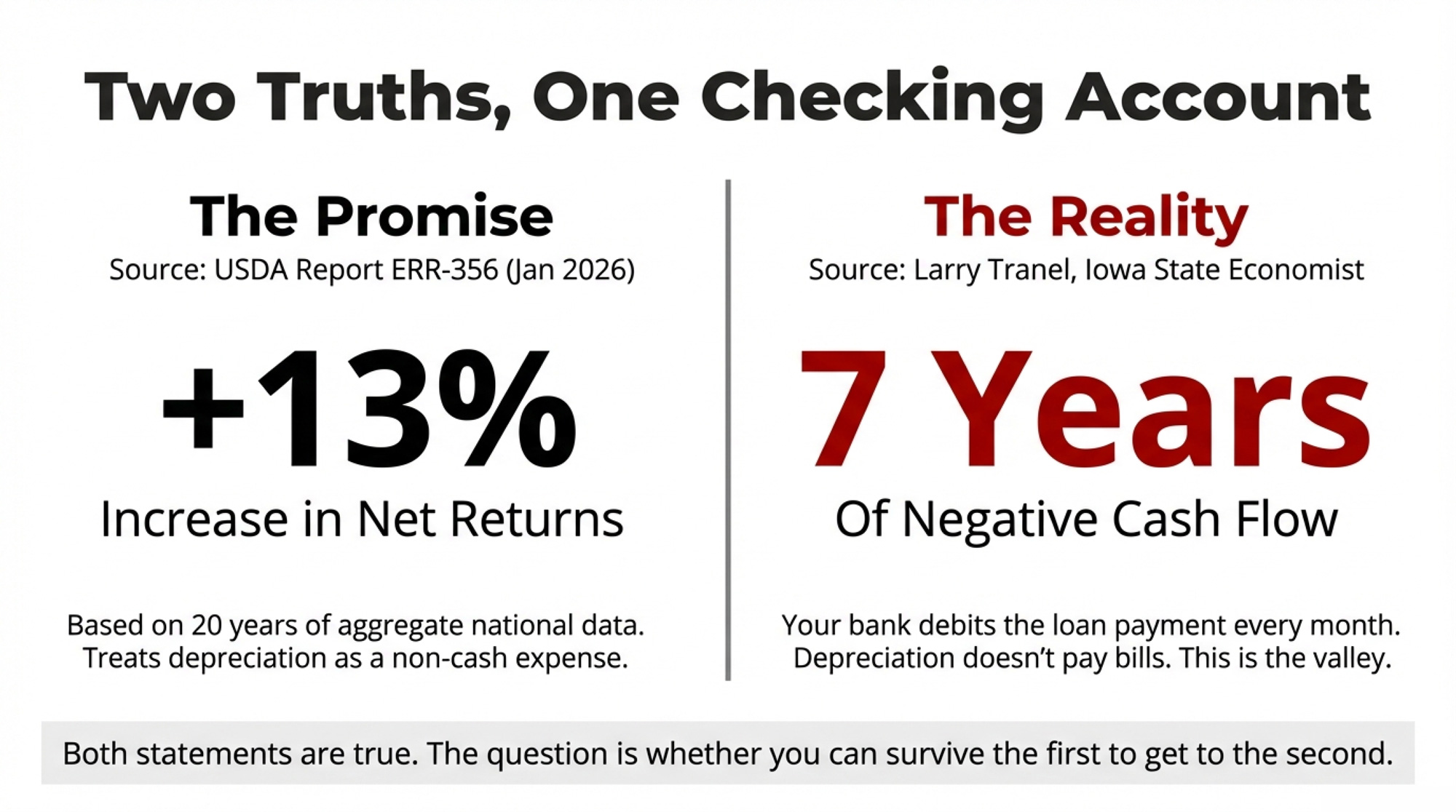

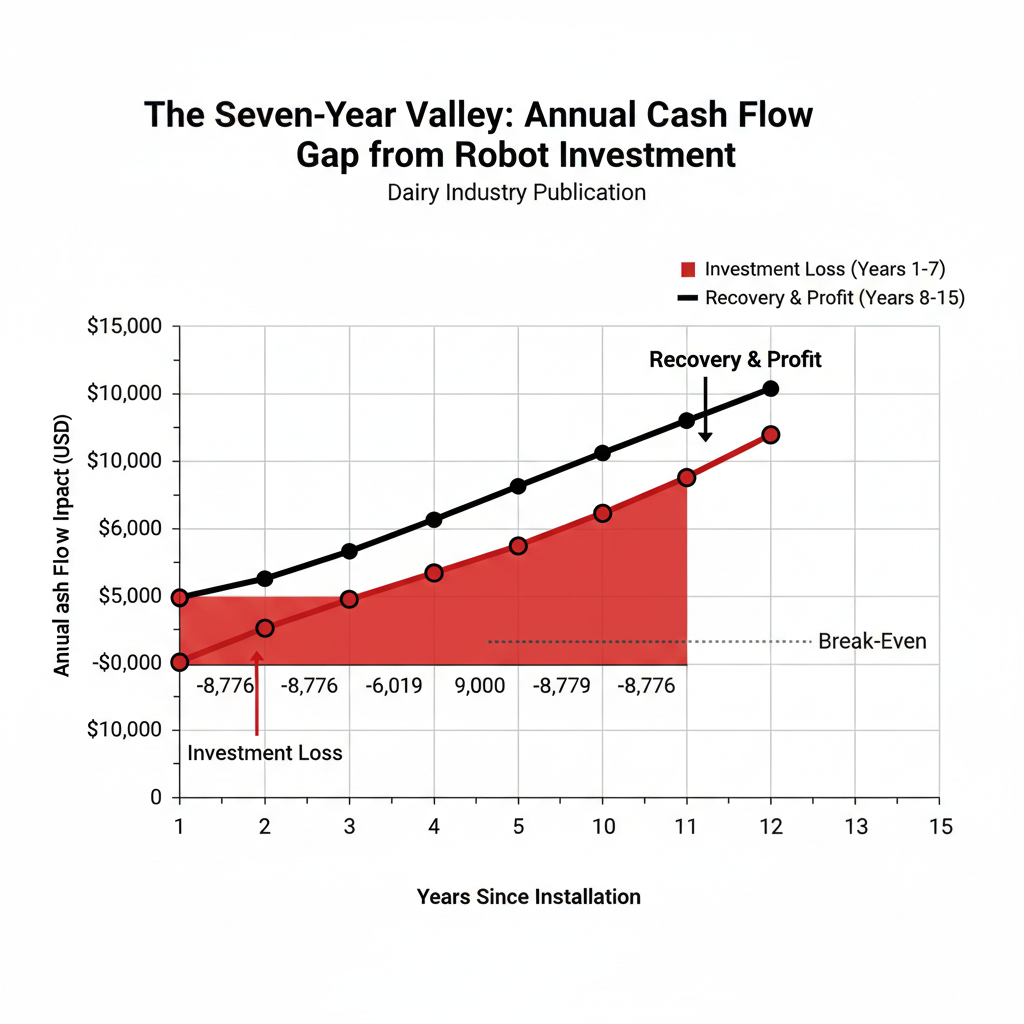

Robotic Milking Pays 13% More – After 7 Years of Red Ink – This exposes the gap between trade-show promises and actual barn-floor returns on robotic milking. It delivers verified payback periods and management thresholds, helping you decide if automation is a survival tool or an expensive mistake for your herd.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

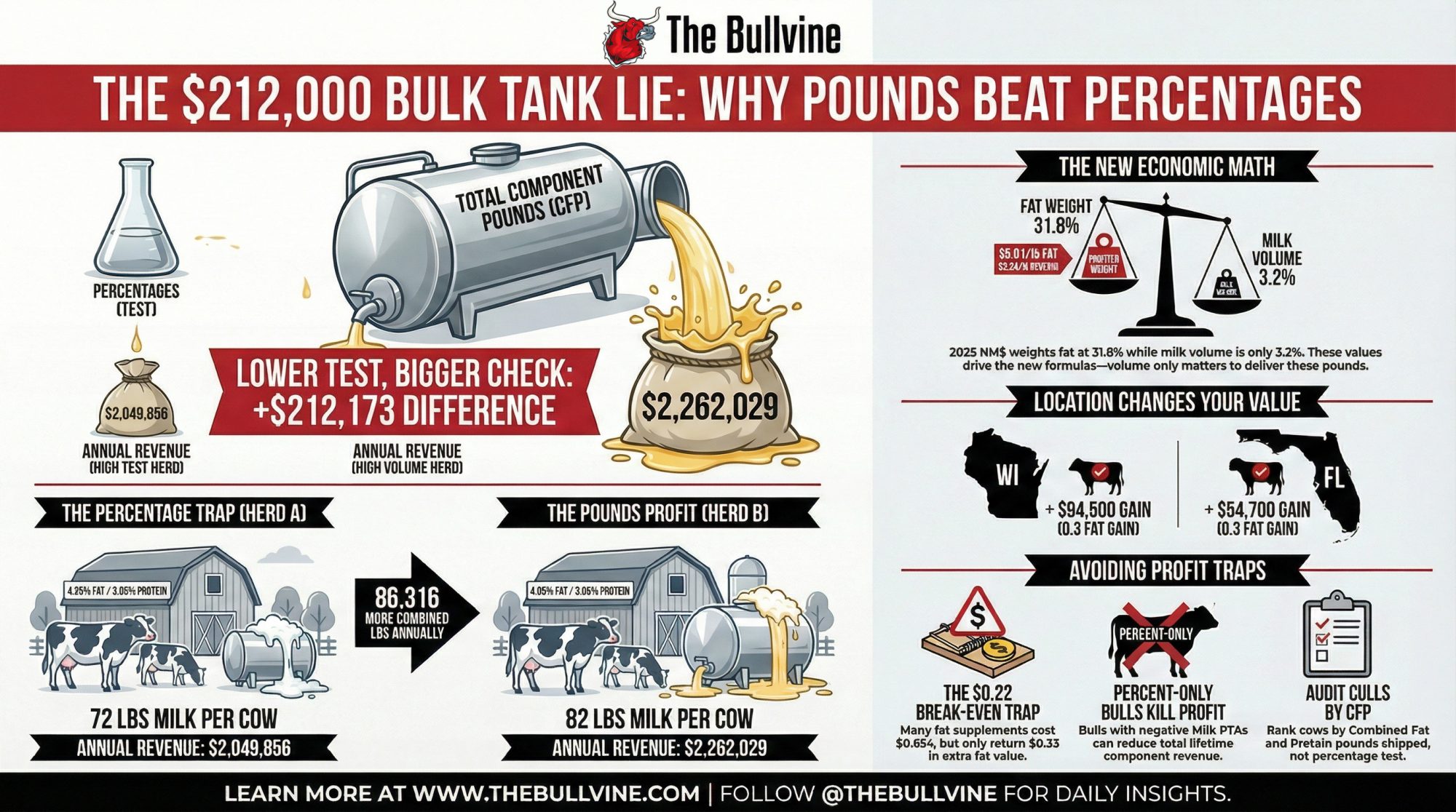

A lower-test herd shipped $212,000 more than its 4.25% neighbor. If you’re chasing percentages, this barn math is your wake-up call.

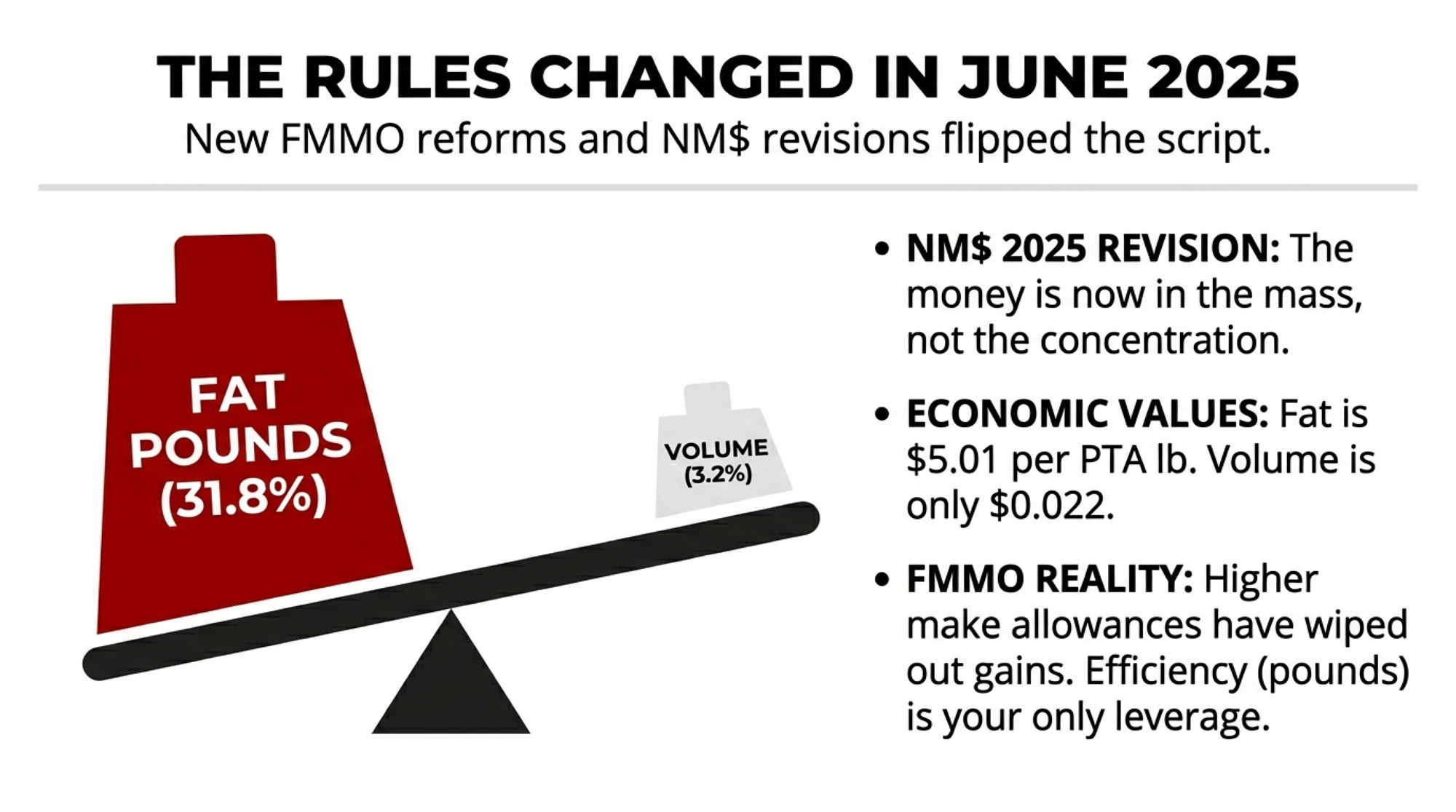

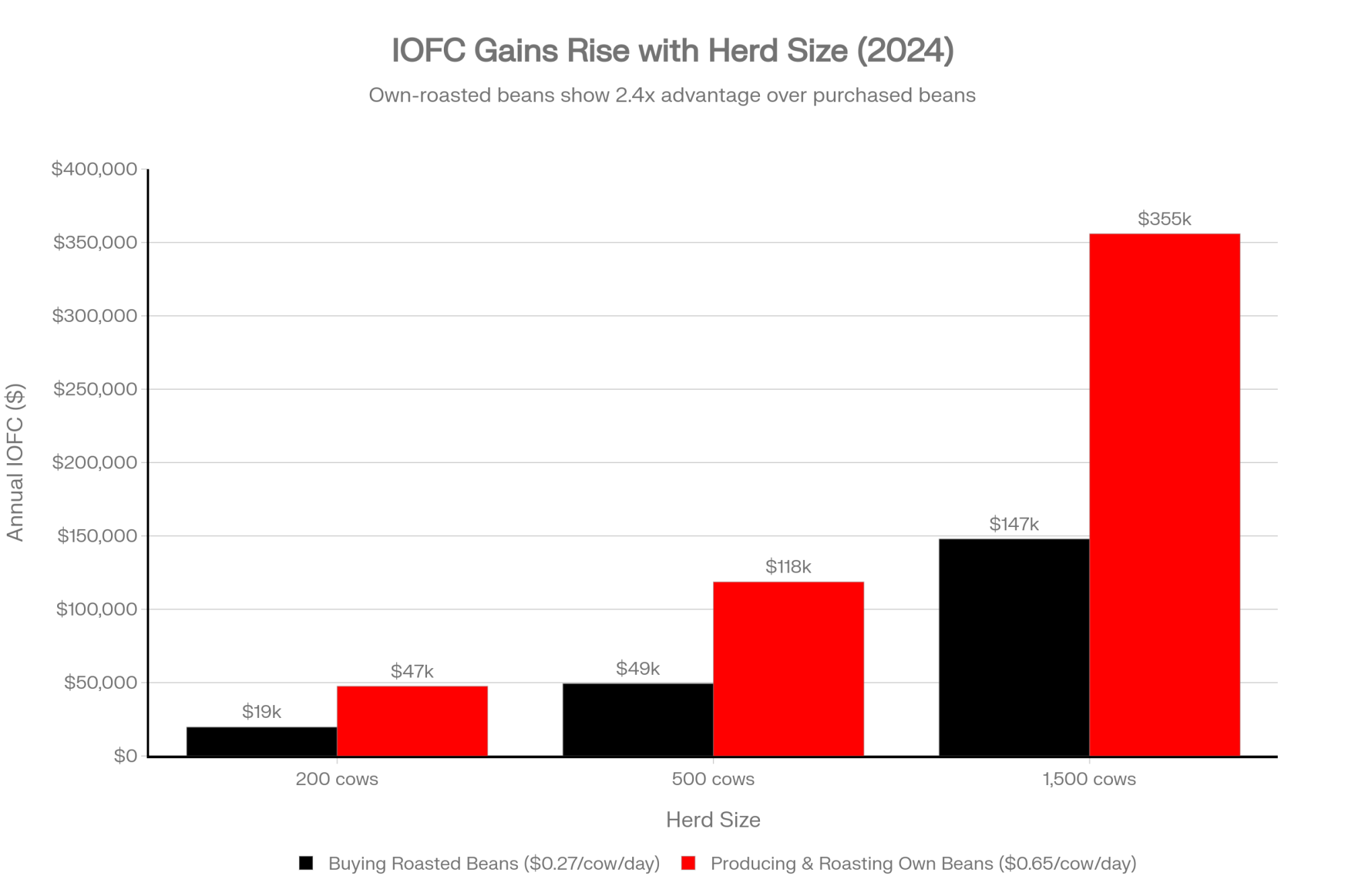

Executive Summary: June 2025 FMMO reforms and the 2025 NM$ revision have flipped the script so that fat and protein pounds shipped, not test percentages, drive your milk check. A side‑by‑side model of two 500‑cow Upper Midwest herds shows the lower‑test herd (4.05% fat at 82 lbs) shipping $212,000 more fat and protein value per year than a 4.25% herd at 72 lbs, using the USDA’s NM$ planning prices. NM$ now gives 31.8% weight to fat and only 3.2% to volume, which means “percent‑only” bulls with negative Milk PTAs can quietly cut lifetime component revenue even when their proofs look good on fat percentage. On the ration side, C16:0 supplement programs that add +0.10 fat test often cost three to four times more than the extra fat is worth once you do the barn math at $0.65–$1.00/cow/day. Your federal order then decides how much of that value you actually see: the same 0.3‑point fat gain is worth roughly $94,500 in a Wisconsin MCP plant but closer to $54,700 in a fluid‑heavy Florida order. The article walks through these calculations step by step and finishes with a four‑point playbook — track CFP, cull on pounds, match spending to your order, and pick sires on component pounds — so you can stress‑test your own numbers instead of trusting what the bulk tank report says.

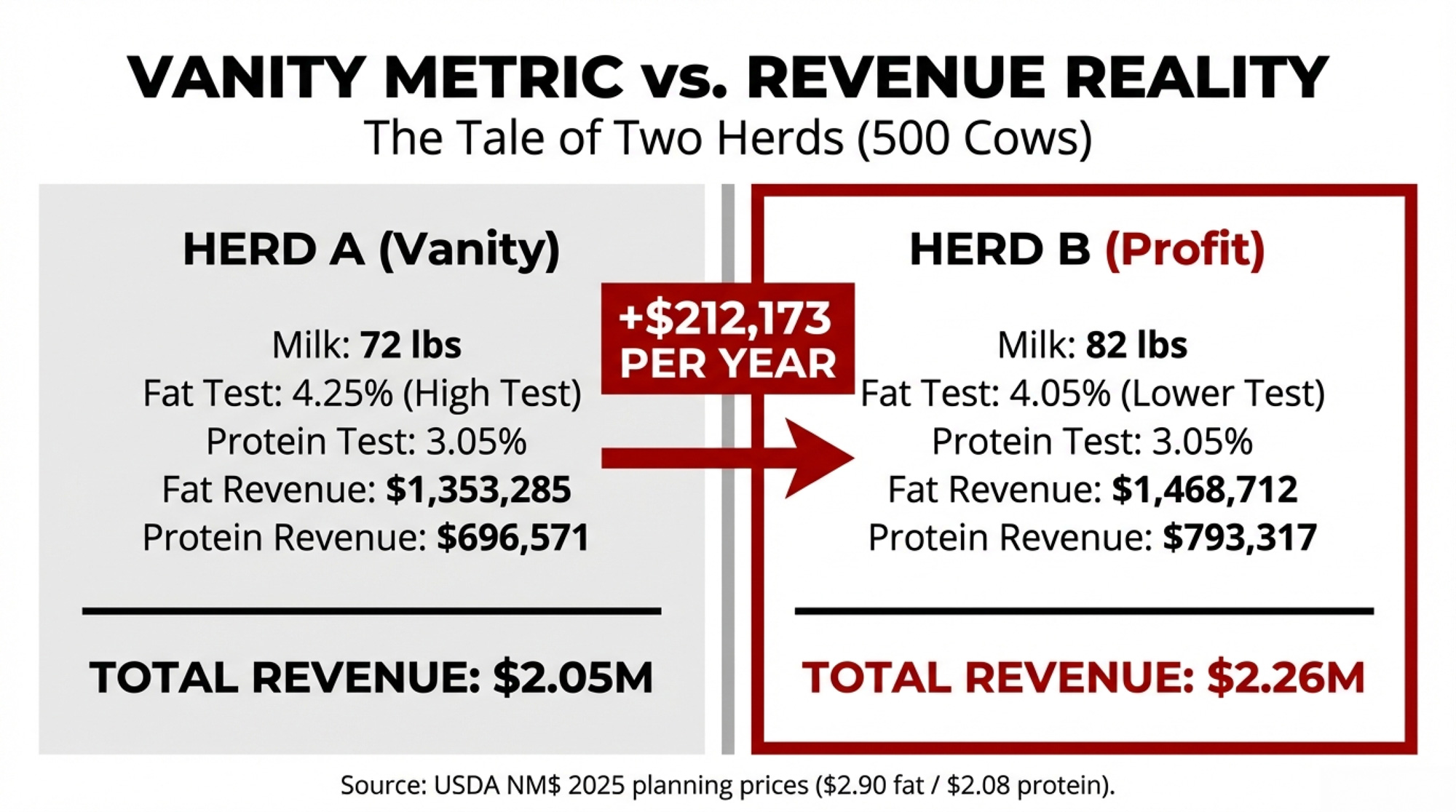

A 500-cow Upper Midwest dairy can leave $212,000 in combined fat and protein revenue on the table by chasing a higher bulk tank test instead of shipping more component pounds. That’s not a hypothetical — it’s what the math shows when you model two herds side by side using USDA’s own NM$ planning prices.

A nutritionist working with herds in the region described the pattern: a 500-cow operation watches butterfat climb from 3.9% to 4.1% over six months. Everyone celebrates. Then somebody runs the real numbers — 78 lbs/day at 3.9% versus 74 lbs/day at 4.1% — and realizes they’re shipping nearly identical fat pounds. The test improved. The milk check didn’t.

What June 2025 Changed — And What It Cost

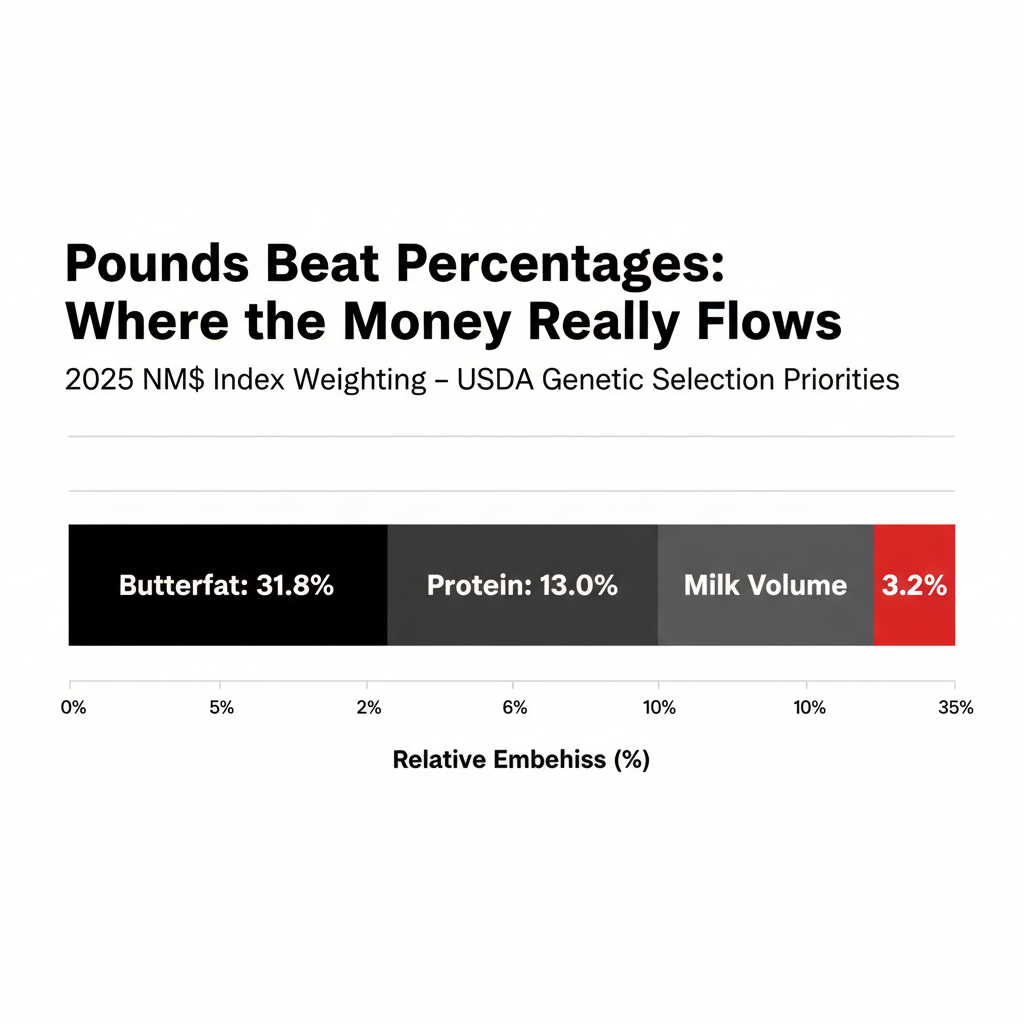

USDA’s April 2025 Net Merit revision pushed butterfat to 31.8% relative emphasis in NM$ — up from 28.6% in 2021 (VanRaden et al., NM$8 and NM$9). Protein carries 13.0%. Milk volume? Just 3.2%. The economic values are blunter still: fat at $5.01 per PTA pound, protein at $3.33, volume at $0.022.

Then the FMMO reforms hit on June 1, 2025. AFBF economist Daniel Munch calculated that in the first three months, producers lost more than $337 million in combined pool value — class price reductions of 85 to 93 cents per hundredweight depending on the order (AFBF Market Intel, September 2025). As Munch told Brownfield Ag News, the higher make allowances “more than wipe out” the gains from other reforms.

Upper Midwest Order 30 absorbed the worst of it. Roughly 69% of pooled milk went to Class III cheese in October 2025, with just 11.3% to Class I fluid (FMMA30 Dairy News, November 2025). That heavy cheese utilization means component value flows directly to producers — but the make allowance increase hit just as directly.

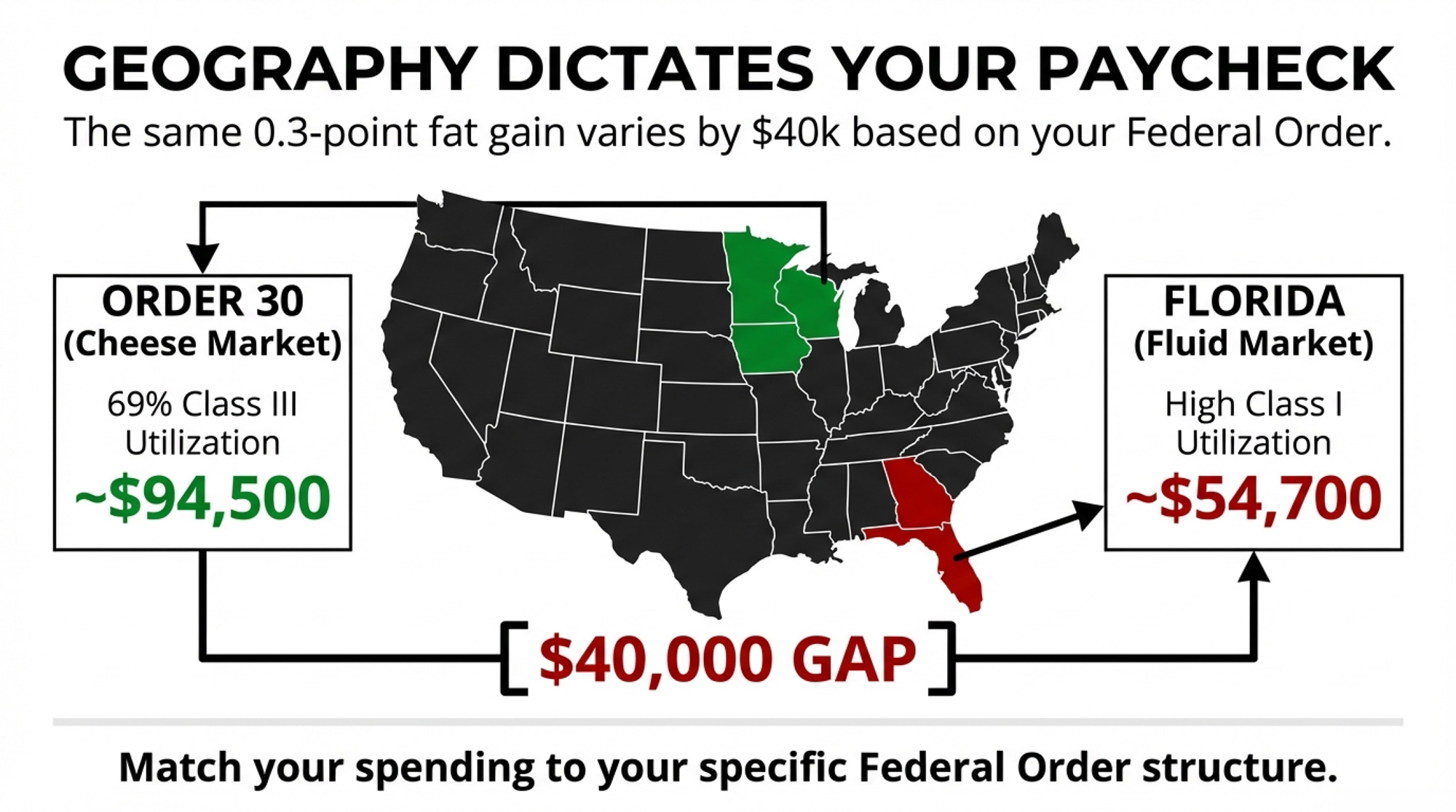

And regional structure amplifies everything. A 0.3-point butterfat improvement on a 500-cow herd captures an estimated $94,500 annually in Wisconsin’s MCP system versus approximately $54,700 in Florida’s skim-fat system. Same genetics. Same nutrition. A $40,000 gap from the order structure alone.

How $212,000 Disappears Into a Better Bulk Tank Test

Two 500-cow herds, both running 305-day lactations, were modeled using NM$ 2025 planning prices of $2.90/lb fat and $2.08/lb protein (VanRaden et al., January 2025). These are multi-year forecast prices; USDA built the index on non-spot prices. Actual FMMO butterfat ran about $2.95/lb in January 2025 and fell to approximately $1.45/lb by January 2026. The pounds principle holds at any price level; the dollar gap moves with the market.

Metric

Herd A (High Test)

Herd B (High Volume)

Difference

Milk/Cow/Day

72 lbs

82 lbs

+10 lbs

Fat Test

4.25%

4.05%

−0.20 points

Protein Test

3.05%

3.05%

Same

Annual Fat Shipped

466,650 lbs

506,453 lbs

+39,803 lbs

Annual Protein Shipped

334,890 lbs

381,403 lbs

+46,513 lbs

Fat Revenue @ $2.90/lb

$1,353,285

$1,468,712

+$115,427

Protein Revenue @ $2.08/lb

$696,571

$793,317

+$96,746

Combined F+P Revenue

$2,049,856

$2,262,029

+$212,173

Herd B — the lower-test herd — ships nearly 40,000 more pounds of fat and over 46,500 more pounds of protein. At actual January 2025 FMMO prices ($2.95 fat, $2.33 protein), the gap widens to roughly $226,000 because protein is priced higher than the NM$ assumption.

Three Places the Trap Compounds Silently

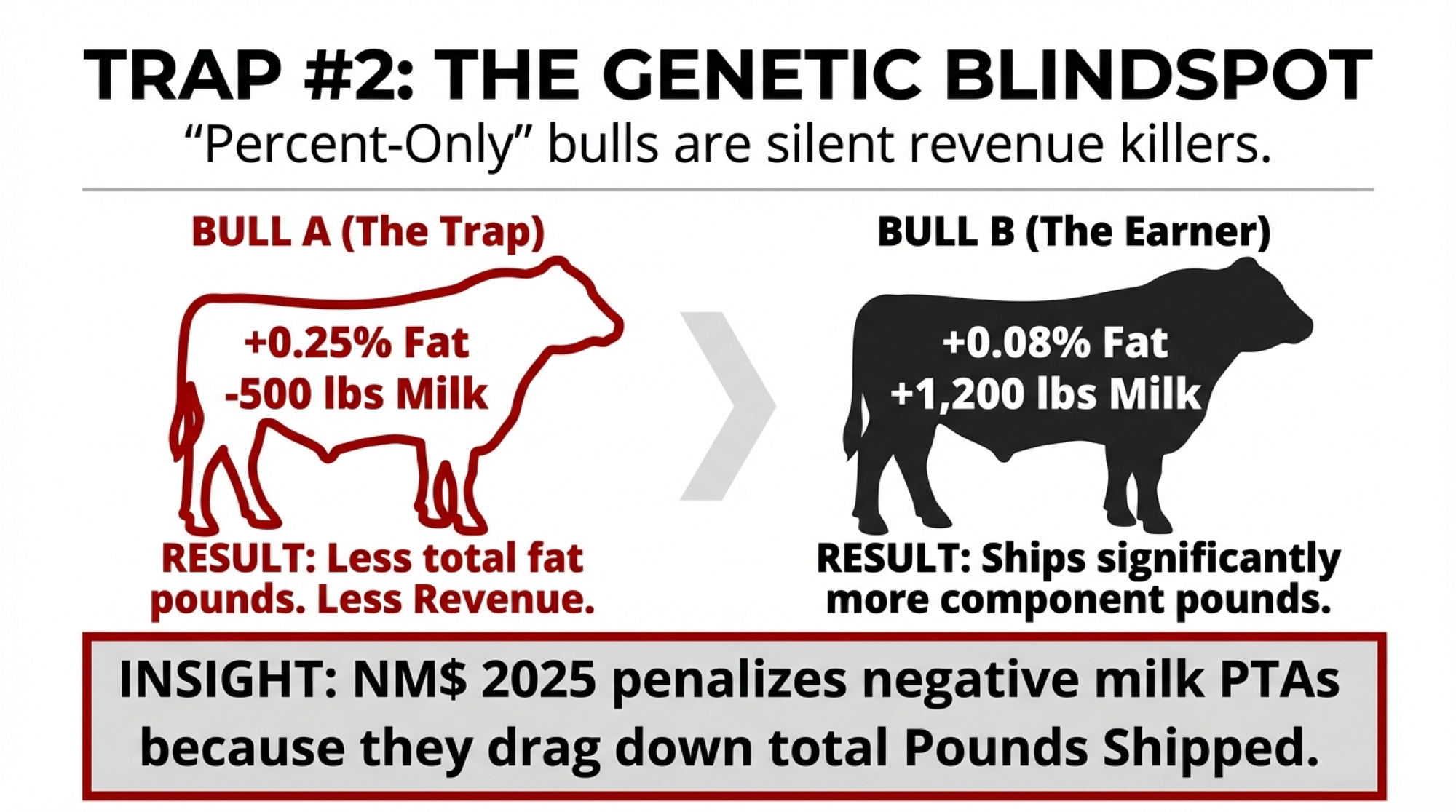

Genetics. The 2025 NM$ penalizes “percent-only” bulls with deeply negative Milk PTAs. A bull posting +0.25% fat but −500 lbs Milk loses on all three lines — less volume means fewer total fat pounds, fewer protein pounds, and less volume revenue. A bull at +0.08% fat with +1,200 lbs Milk often ships more total component pounds per lactation. That’s exactly what the $5.01/lb and $3.33/lb economic values reward.

Nutrition. Research from Prof. Kevin Harvatine’s lab at Penn State found C16:0 palmitic acid boosts fat test by +0.30 to +0.50 percentage points at ~2% of diet DM (Dairy Global, November 2023). Michigan State’s de Souza lab (J. Dairy Sci., 2024) showed mid-lactation cows at 40–50 kg/day responded best. But supplements run $0.65–$1.00/cow/day, and the protein test can slip 0.02–0.03 points. If milk yield doesn’t climb with the fat test, the P&L can go negative while the bulk tank report looks great.

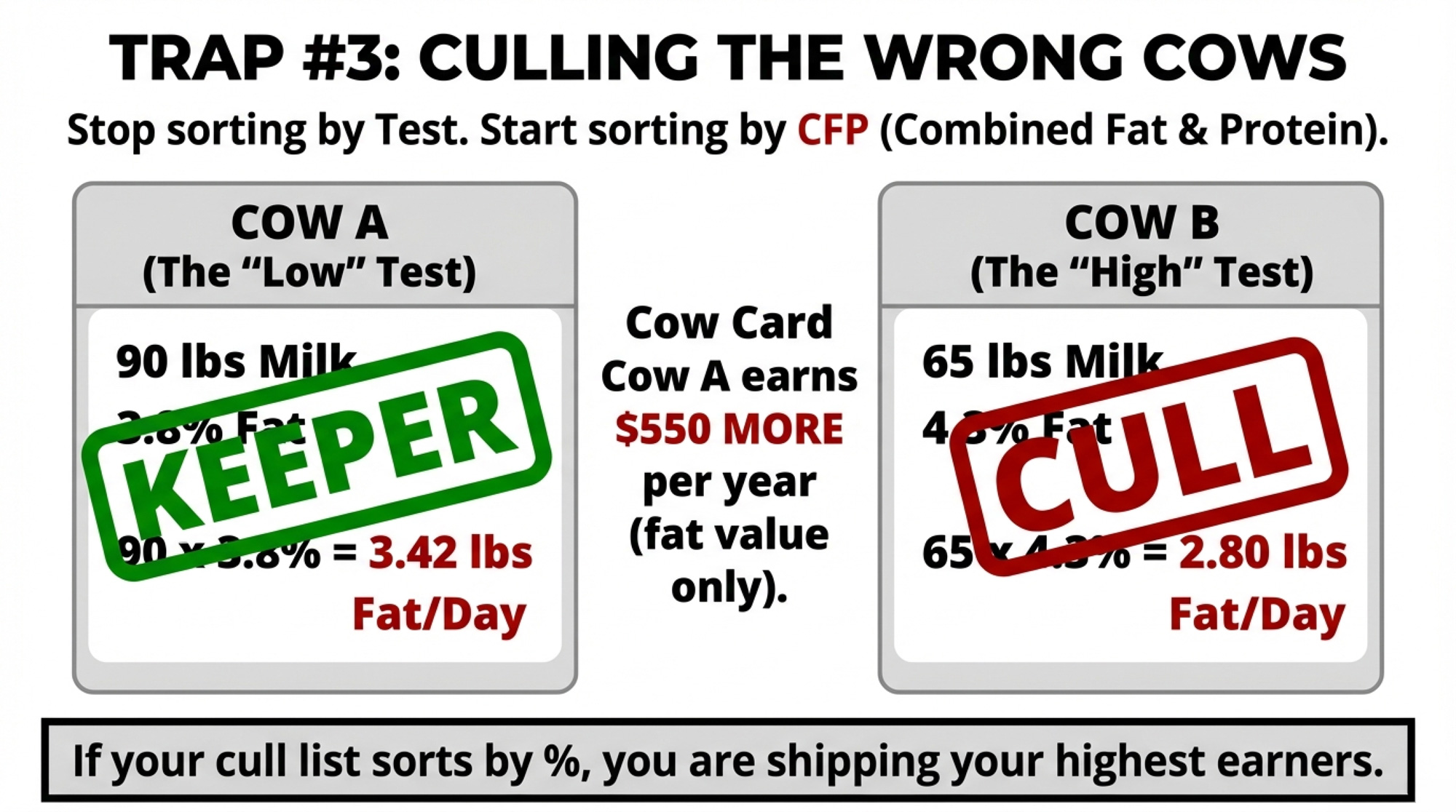

Culling. Cow 1 at 90 lbs/day and 3.8% fat ships 3.42 lbs fat/day. Cow 2 at 65 lbs/day and 4.3% ships 2.80 lbs. The “low test” cow delivers 0.62 more lbs of fat daily — about $550/year at $2.90/lb. If your cull list sorts by test instead of CFP (combined fat and protein pounds shipped), you may be shipping the wrong animals.

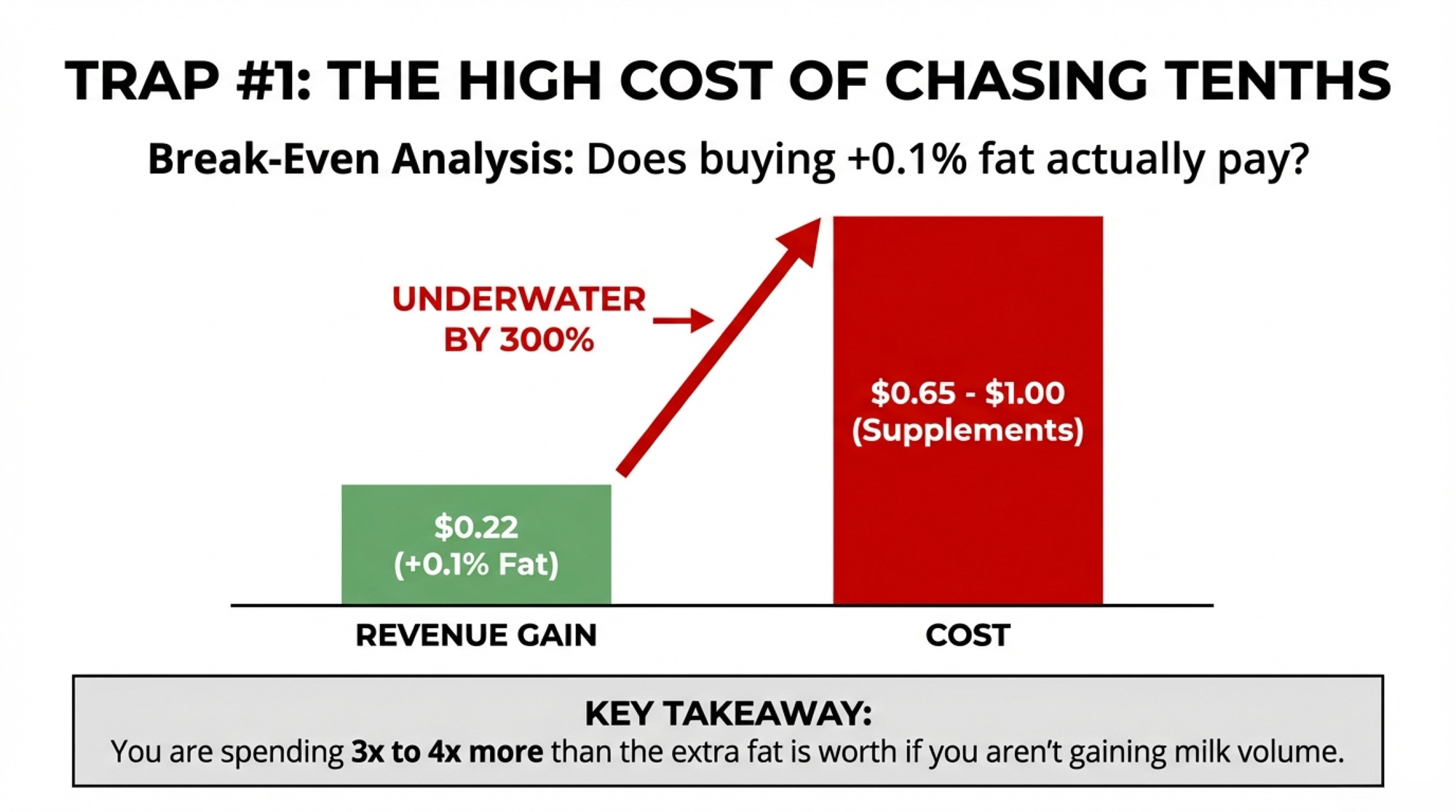

Does Chasing +0.1% Fat Actually Pay Under Component Pricing?

Full walkthrough: a program promising +0.10 points fat test on 500 cows averaging 75 lbs/day.

Break-even: about $0.22/cow/day. That’s three to four times below what any published C16:0 program costs. If a tenth of a point on fat test is the only gain — and you’re losing milk or protein in the process — the math is underwater.

The Shift: From Test Reports to Pounds Shipped

For herds getting ahead of this, the pivot starts with one change: they stop celebrating test and start tracking CFP per cow per day. Instead of “Our herd’s at 4.1% fat,” they’re asking: “How many pounds of fat and protein did we ship per cow today?”

That reframes every proposal — a new sire lineup, a nutrition tweak, or a cull list — around one question: does it raise CFP?

The Playbook: Four Ways to Manage for Pounds

1. Make CFP your primary metric. Calculate combined fat + protein pounds per cow per day, minimum monthly. 30-day action: pull last month’s data and establish your baseline. Trade-off: watching fat test flatten while CFP climbs feels wrong. It’s not.

2. Rebuild the cull list around CFP. Rank by shipped CFP first, then overlay fertility, health, and age. 90-day action: audit last quarter’s culls against CFP. Trade-off: you still need to watch for milk fat depression — tests aren’t irrelevant, just not the sorting metric.

3. Match spending to what your order actually pays. Order 30’s 69% Class III utilization means component value flows through relatively directly. In skim-fat orders with heavy Class I, the math is different. 30-day action: call your field rep and ask how much component value hits your check. Trade-off: even within the same order, different handlers deliver different capture.

4. Run genetics and nutrition on parallel tracks. Long-term: component-pound genetics (NM$, CFP). Short-term: nutrition for quick wins. 365-day action: rebalance your sire lineup at the next proof run using pound PTAs, not percentage PTAs. Trade-off: if component prices sag — January 2026 butterfat at ~$1.45/lb is a reminder — nutrition plays may need to scale back. The genetics keep compounding regardless.

What This Means for Your Operation

Run your own Herd A vs. Herd B table. Plug in your daily lbs, fat test, protein test, cow count, and your most recent FMMO component prices. If a lower-test scenario ships more pounds, you’ll need to decide.

The break-even for a +0.1% fat program is $0.22/cow/day. Published C16:0 costs range from $0.65 to $1.00. If you’re spending three to four times the break-even, the fat gain alone doesn’t cover it.

Audit your culls. Pull three to five cows you shipped for “low components” and check their CFP against cows you kept. If CFP sorts the list differently than test did, rebuild it.

Know your order structure. Order 30’s 69% Class III means the component value flows through. If you’re in a fluid-heavy order, your capture math is different — and so is every component investment decision.

Key Takeaways

If your success metric is fat test rather than fat and protein pounds shipped, you’re managing to the wrong number. The post-June 2025 FMMO system and the 2025 NM$ ($5.01/lb fat, $3.33/lb protein) both reward pounds.

The $212,000 gap is $115,427 from fat and $96,746 from protein at NM$ planning prices. At actual January 2025 FMMO prices, it’s closer to $226,000.

The 2025 NM$ penalizes percent-only bulls. Fat emphasis jumped from 28.6% to 31.8%, but milk volume still carries a positive value. A sire whose Milk PTA drags may produce daughters that ship fewer total component pounds.

Regional structure reshapes every component decision. A 0.3-point fat gain isn’t worth the same $94,500 in Wisconsin as it is in a fluid-heavy Southeast order.

The Bottom Line

The herds that come out of this stronger won’t necessarily be the ones with the prettiest bulk tank reports. They’ll be the ones that ran the barn math and were honest about what actually pays. So — where does your herd sit: managing for the number that feels good, or the pounds that move the check?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

$19.14 Costs vs. $18.95 Milk: Is Your Barn Tech Paying the Difference? – Stop leaving margin on the barn floor. This analysis exposes why you’re 19¢/cwt underwater and arms you with the specific ROI calculations to ensure your current technology actually pays for itself through increased efficiency.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

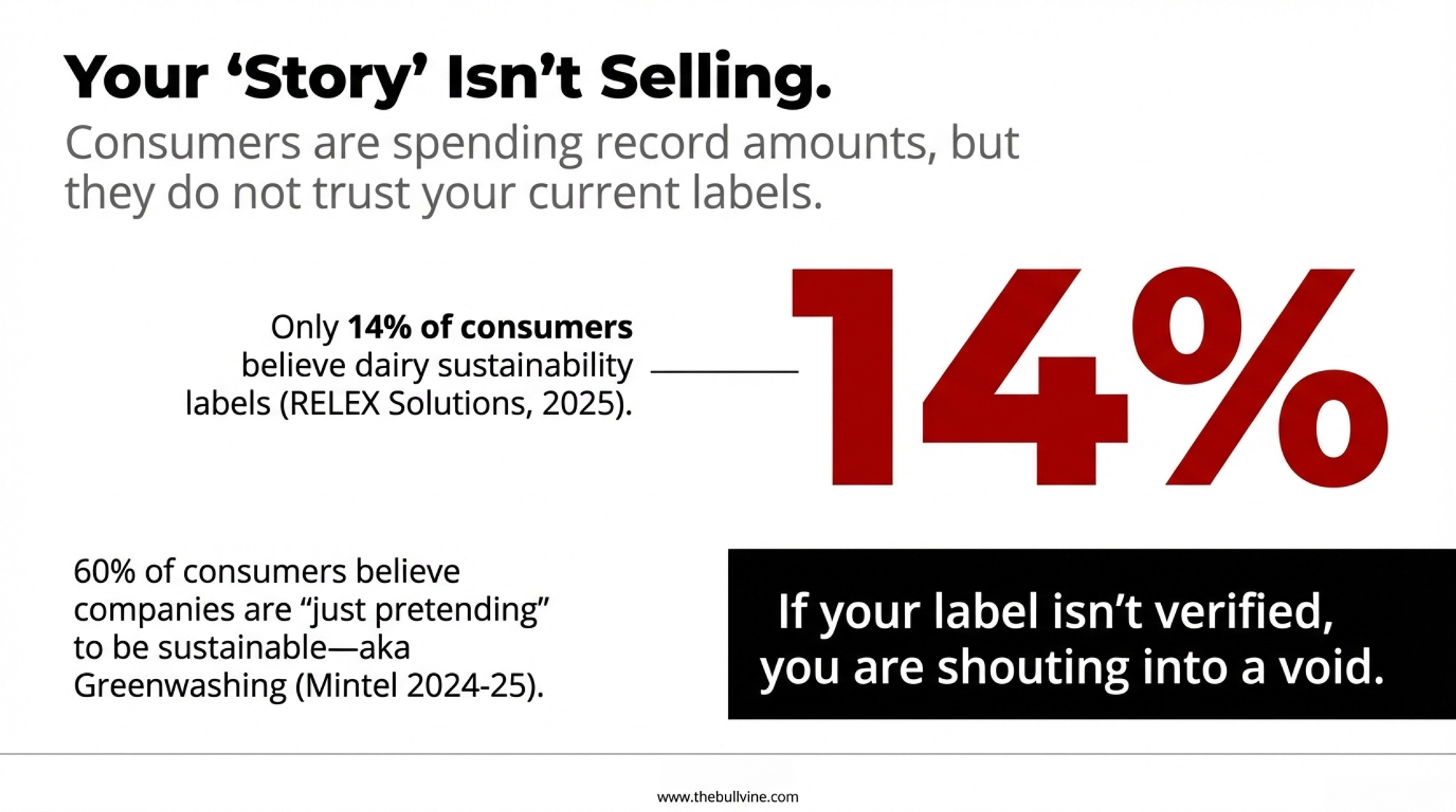

Only 14% of consumers believe dairy labels. Jasper Hill still gets $22 a wedge. If you aren’t turning welfare and certification into margin, you’re leaving money on the shelf.

Executive Summary: Valentine’s Day spending is hitting records, but only 14% of consumers believe sustainability claims on dairy labels, which means your “story” probably isn’t buying you much margin right now. Across U.S., Canadian, and European research, shoppers consistently rank animal welfare ahead of carbon when they choose dairy, and they’re willing to pay more when a credible certification backs that claim. That’s why organic, grass-fed, and welfare-certified brands like Jasper Hill, Maple Hill, Alexandre Family Farm, and AGW-certified herds are already seeing retail premiums of $2.63 per half gallon and farm-gate pay prices in the $40–$50/cwt range against a $14.70 conventional Class I base. At the same time, hot-button issues like cow–calf separation and child labor in cocoa are shaping how consumers judge the ethics of the cheese and chocolate they put on a Valentine’s board. You’ve already got programs like FARM and proAction running in the background, and pasture-based herds can add AGW, Validus, or Regenerative Organic Certification on top — but none of that pays unless you translate it into a plain-language welfare story consumers can find and trust. This piece gives you a concrete playbook for three types of operations — co-op shippers, regional/specialty suppliers, and direct-to-consumer farms — to turn welfare and certification into better contracts, stronger brands, and higher-value Valentine’s sales, rather than leaving money on the shelf.

Somewhere tonight, a shopper will pick up a $22 wedge of aged cheddar for their Valentine — and flip it over looking for a dairy animal welfare certification before they check the price. Valentine’s Day spending will hit a record $29.1 billion in 2026, up from $27.5 billion last year, with the average American budgeting $199.78 on gifts (National Retail Federation, January 2026, n=7,791 U.S. adults). Dairy is increasingly part of that haul: Wakefield Research data (December 2025, n=1,000 U.S. adults) commissioned by Wisconsin Cheese found 66% of Americans now call cheese their “love language,” and 64% would trade a dozen roses for a curated cheese board.

Jasper Hill Farm’s underground aging cellars turn high‑welfare milk into $22 wedges that can survive a Google search — the kind of welfare‑backed story most dairy labels never tell.

One farm has figured out how to make that moment work for them. In Greensboro, Vermont, brothers Andy and Mateo Kehler built Jasper Hill Farm into the gold standard of artisan dairy — pasture-based and regenerative, their cheeses aged in 22,000 square feet of underground cellars. Jasper Hill blue cheese was featured at the Obama White House state dinner for French President François Hollande in February 2014 — accompanying the dry-aged rib eye on a menu designed to showcase America’s best small-farm producers. Their Harbison won Best of Show at the 2018 American Cheese Society competition, topping 1,954 entries. Most dairy labels can’t survive that level of scrutiny. Jasper Hill’s can, and that difference is worth real money in 2026.

Feel-good spending numbers aside, only 14% of U.S. consumers fully trust grocery sustainability claims (RELEX Solutions, 2025 U.S. consumer survey), and Mintel’s Global Outlook on Sustainability: A Consumer Study 2024-25found 60% think companies are “just pretending” to be sustainable. Dairy animal welfare certification should be the credibility tool that closes this gap. For most operations, it isn’t — because most operations aren’t talking about it.

Dairy’s Valentine’s Moment — More Shelf Space, No Story Behind It

Candy still leads the Valentine’s gift list at 56%, followed by flowers and evenings out. But dairy keeps gaining ground in ways the commodity numbers don’t capture. In the UK, cheese volumes surged by an additional 1.2 million kg around Valentine’s compared to pre-COVID levels, with specialty and continental varieties accounting for 24% of that increase (AHDB, 2022 UK data).

Wisconsin Cheese’s “Wedges of Love” — a $100 curated box of nine artisan cheeses from producers like Roelli Cheese Haus and Uplands Cheese Company — was released in limited drops from January 20 through February 8, available while supplies lasted. As their Chief Marketing Officer, Suzanne Fanning put it, “cheese is always welcome to the party.” And when 62% of consumers say they’re bored of traditional Valentine’s gifts, the market opening for dairy is obvious.

Wisconsin Cheese’s $100 “Wedges of Love” box — nine artisan wedges from producers like Roelli and Uplands, launched January 20, sold in limited drops. When 62% of consumers say they’re bored of roses, this is what a dairy Valentine’s marketing play looks like.

The industry keeps putting cheese on the shelf without a credible story to back it up. As Jasper Hill Farm describes its approach on their website, great cheese starts with good milk, good milk starts with healthy animals, and healthy animals start with a healthy landscape. That’s not marketing copy—it’s a supply chain philosophy. It’s also exactly what consumers are hunting for when they flip over that label, and it’s what separates a $22 wedge from a $4 block in the same dairy case.

Under-35 Shoppers Read Your Label — Then Google It

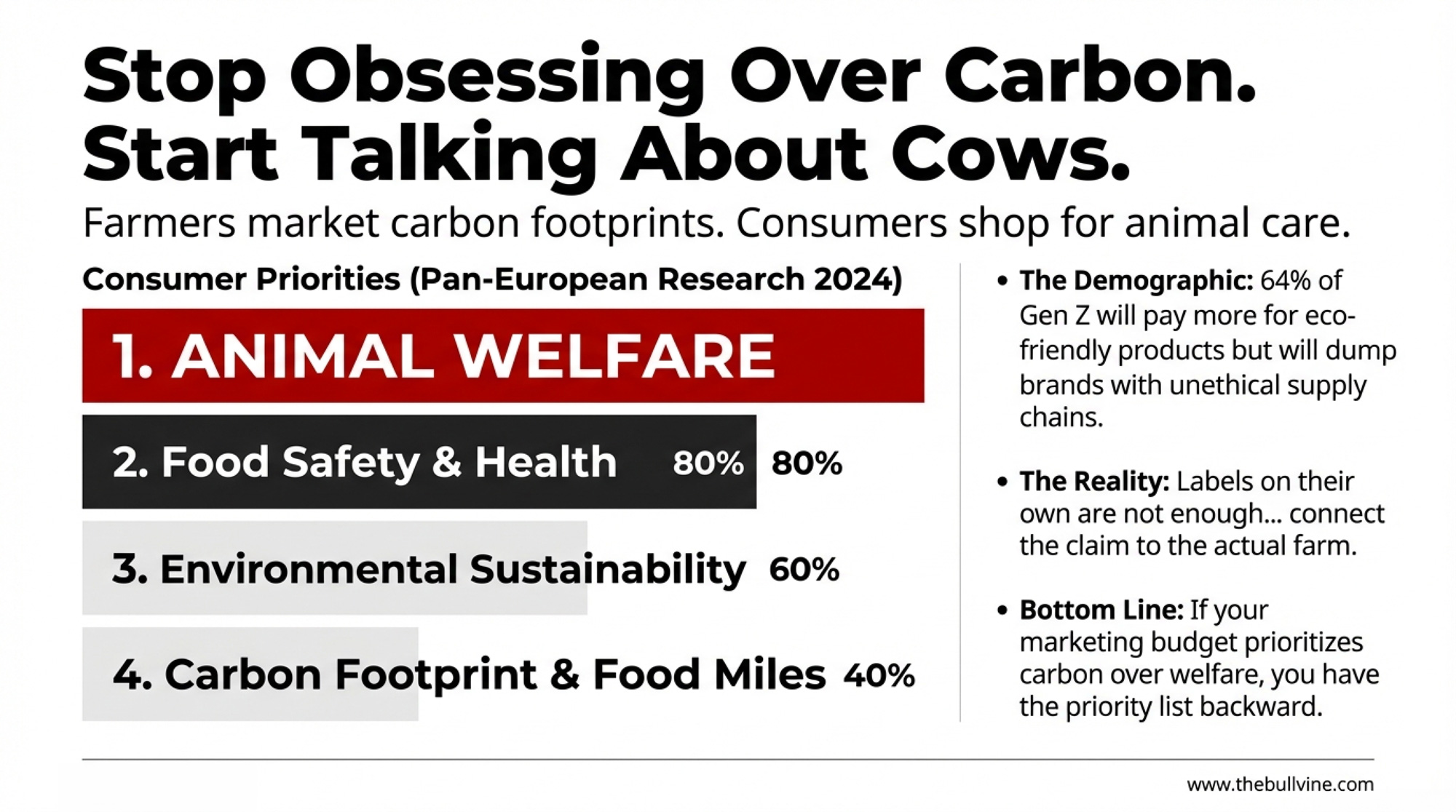

Over 70% of consumers under 35 say they’re more likely to buy from brands demonstrating genuine sustainability commitments (The Dairy Mail, January 2025 analysis). Among Gen Z specifically, 64% say they’d pay more for eco-friendly products — and the same 64% would dump a brand exposed for unethical supply chain practices (Britopian, 2025, U.S. data).

This isn’t just survey talk. In the UK, one in ten consumers boycotted a go-to brand in the past year over sustainability concerns, and 17% actively check labels for certifications before buying (Speciality Food Magazine, November 2024 UK survey). Among 24-to-35-year-olds, 10% said they’d pay up to 50% more for verifiably sustainable products.

A 2024 pan-European study published in Agrarforschung Schweiz (Swiss Agricultural Research), surveying consumers across five countries, laid out what this demographic actually prioritizes when buying dairy:

Animal welfare — ranked first, ahead of every other sustainability attribute

Food safety and health — second and third, reflecting practical self-interest

Environmental sustainability — important, but consistently ranked below welfare

Carbon footprint, food miles, and organic certification — at the bottom of the list

The researchers noted that “labels on their own are not enough to change behaviour” and recommended pairing labels with communication connecting the claim to the actual farm. If your marketing budget prioritizes carbon messaging over animal welfare communication, you’ve got the priority list exactly backwards.

Welfare Outranks Carbon — And the Premium Is Real

A November 2025 study in the Journal of Dairy Research found 70% of consumers expressed willingness to pay a premium for animal welfare-certified dairy, with women and younger consumers showing significantly higher interest; 91% agreed pasture access improves welfare. American Humane’s 2024 Farm Animal Welfare Survey (a nationally representative U.S. sample, November 2024) found 67% prefer humanely raised products, 67% emphasize the importance of third-party certification, and 58% are willing to pay more for humanely raised labeling.

Does willingness-to-pay always translate at the register? Anyone who’s watched a consumer reach for the cheaper jug knows the gap between survey answers and checkout behavior. But the premiums already flowing through the dairy case say this isn’t hypothetical anymore.

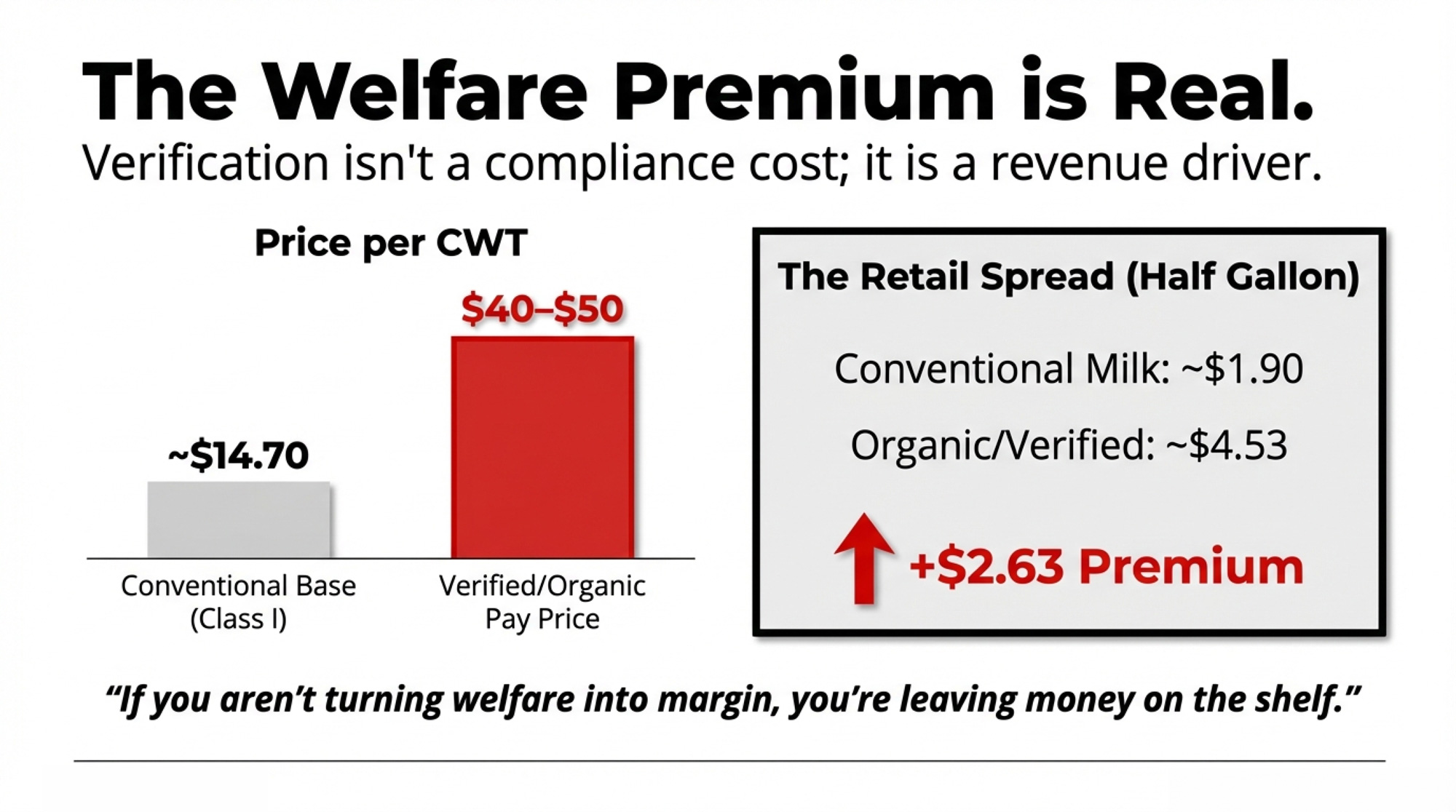

USDA AMS data from February 2026 shows organic half-gallon milk averaging $4.53 retail versus $1.90 for conventional — a $2.63 premium. Organic gallon milk: $8.66 versus $2.79, a $5.87 spread (USDA AMS, November 2025). Organic farm-gate pay prices in 2025 ranged from Horizon contracts at $40+/cwt to Maple Hill targeting $45/cwt and newcomer Origin Milk near $50/cwt (NODPA, May 2025) — against a conventional Class I base price of $14.70/cwt (USDA AMS, February 2026).

Product/Certification Type

Retail Price (per unit)

Conventional Baseline

Retail Premium ($)

Farm-Gate Pay ($/cwt)

Conventional Milk

$1.90 (half-gal)

$1.90

—

$14.70

Organic (Horizon)

$4.53 (half-gal)

$1.90

+$2.63

$40.00+

Maple Hill (Grass-Fed Organic)

$7.59 (half-gal)

$1.90

+$5.69

$45.00

Alexandre Family Farm (Regenerative Organic)

$7.49–$8.89 (48–59 oz)

~$1.52–$1.83 (equiv.)

+$5.97–$7.06

$45.00–$50.00

Origin Milk (Organic)

Not disclosed

$1.90

Not disclosed

~$50.00

AGW-Certified (Autumn’s Harvest)

Premium pricing

Conventional

+20% sales lift

Processor-dependent

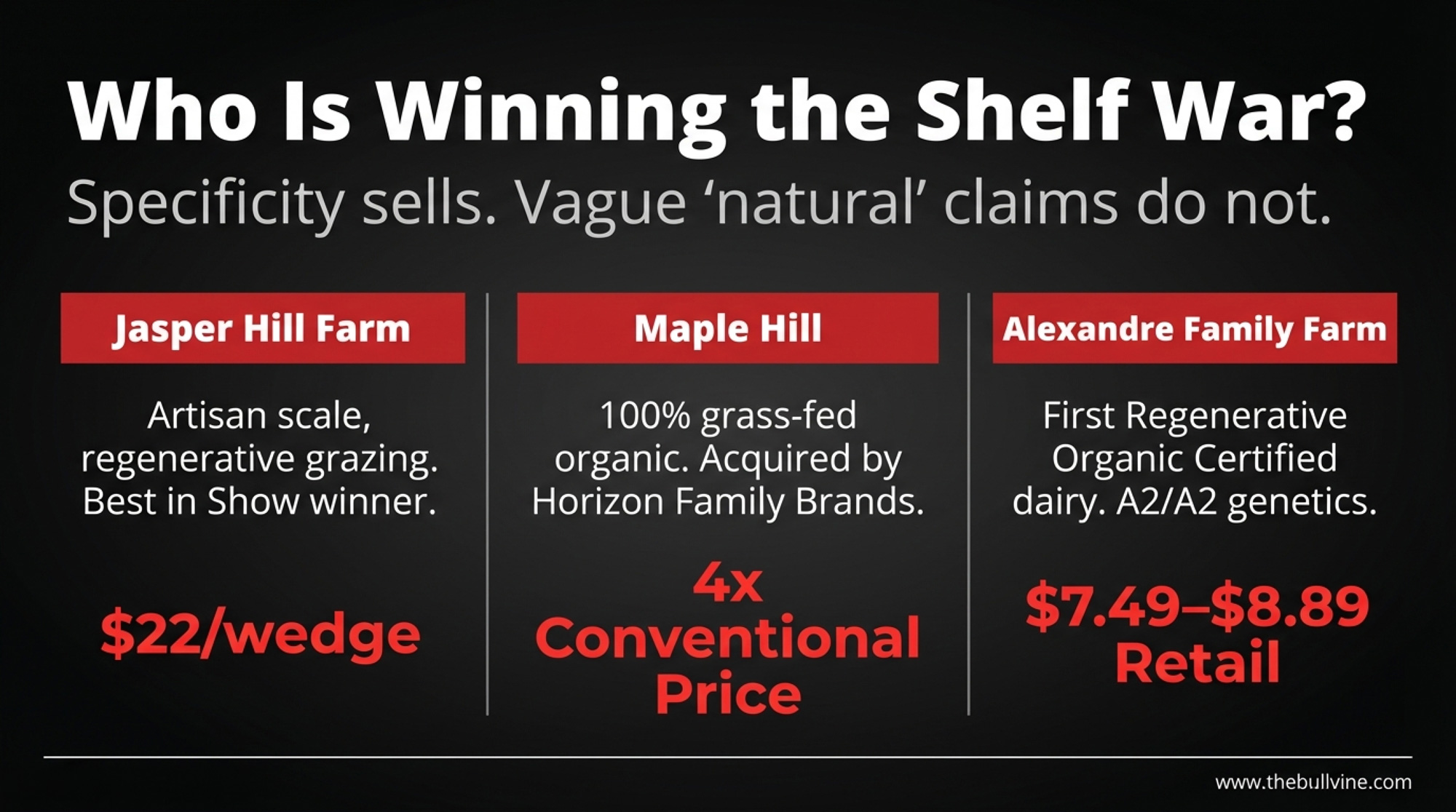

You can see it at the shelf. Maple Hill Creamery — now part of Horizon Family Brands after a December 2025 acquisition, but still marketed as 100% grass-fed organic and PCO certified — retails at $7.59 per half gallon at Target. Four times the conventional price. Alexandre Family Farm in Crescent City, California — the first Regenerative Organic Certified dairy in the U.S., pasture-based, A2/A2, a multi-generational family operation — retails at $7.49–$8.89 for 48–59 oz. Whether your operation captures any of that value or watches it flow to someone else’s label depends entirely on what story you’re telling.

The Alexandre family on pasture in Crescent City, California — a multi-generational operation, the first Regenerative Organic Certified dairy in the U.S., retailing A2/A2 milk at $7.49–$8.89. This is what a welfare story that survives a Google search looks like.

About that Maple Hill acquisition. Platinum Equity bought the Horizon Organic and Wallaby brands from Danone in April 2024 and rebranded as Horizon Family Brands in August. By December 2025, they’d acquired Maple Hill as their first bolt-on — CEO Tyler Holm called its grass-fed expertise a complement to Horizon’s “capabilities and vision for the future.” When private equity is paying acquisition prices for grass-fed organic brands, the market is telling you something about where the value is heading.

Here’s the baseline most consumers have never heard of: 99% of U.S. domestic milk production already participates in the FARM Animal Care program, covering more than 31,000 dairy farms across 49 states. In Canada, proAction is mandatory on every dairy farm. The programs exist.

The consumer communication doesn’t. Jamie Jonker, then NMPF’s vice president of sustainability and scientific affairs, put it well in a FARM Program report: “Farmers have a great story to tell when it comes to animal care on their farms. The goal of animal-care programs, like the FARM Program, is not to be an additional burden for farmers, but rather to collect the data that provides positive proof of what we already know to be true: farmers take excellent care of their animals.”

That story is just not reaching the people buying your milk. The premium opportunity is real — but so is the risk, because the welfare story consumers hear most often isn’t the one you’d choose to tell.

Calf Separation: The Story Activists Tell When You Won’t

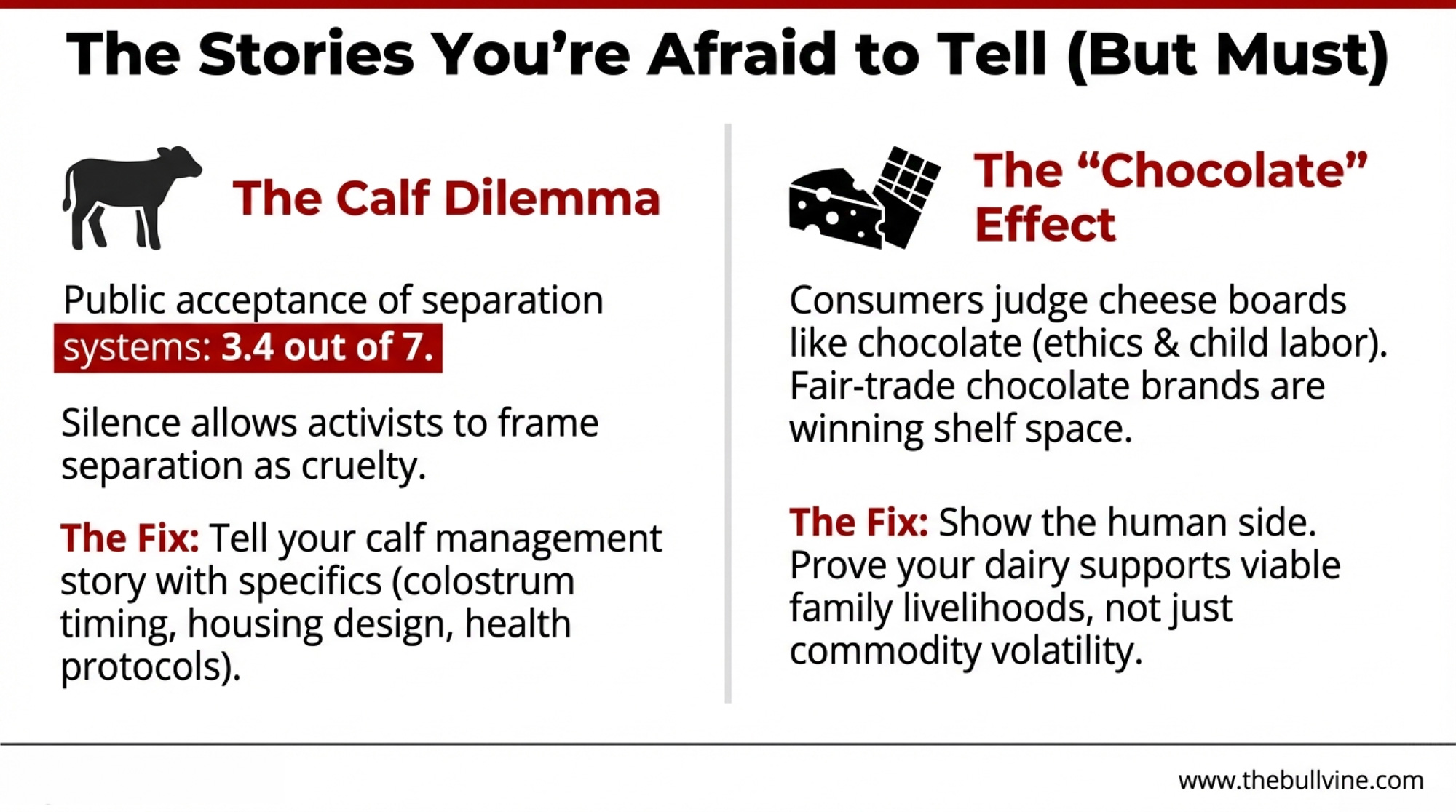

Anyone who’s walked through a maternity pen at 2 a.m. knows the bond is real — and that managing it responsibly is complicated. Early cow-calf separation followed by individual housing is still standard practice on most dairy operations. Public acceptance of it is remarkably low.

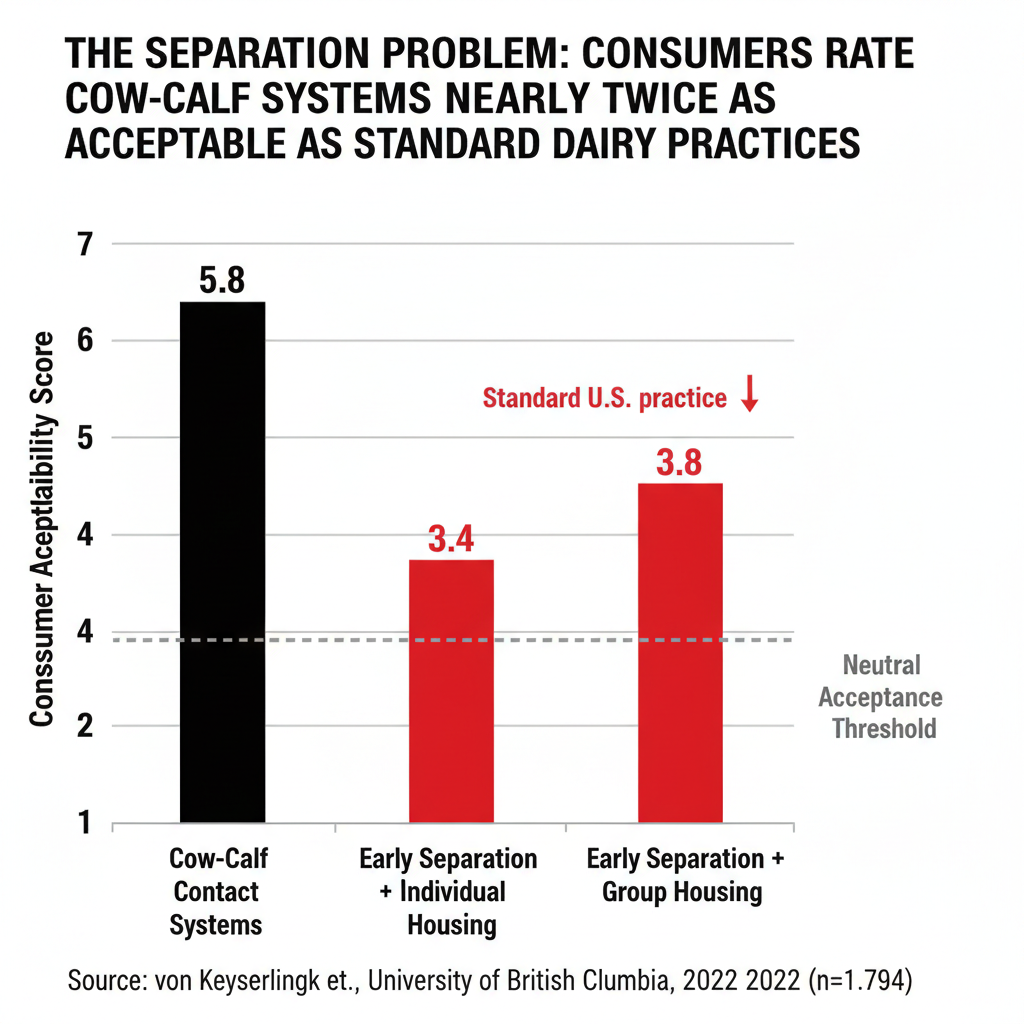

Dr. Marina (Nina) von Keyserlingk, NSERC Industrial Research Chair in Dairy Cattle Welfare at the University of British Columbia, published a 2022 study — a convenience sample of 307 Canadians plus a nationally representative sample of 1,487 Americans — and found that on a 7-point scale, cow-calf systems scored 5.7–5.8, while separation systems scored just 3.4–3.8 regardless of housing type. Faunalytics research confirmed the pattern: after visiting a working dairy farm, the most common new concern was calf separation, and exposure didn’t neutralize it. It amplified it.

The health argument for day-one separation? Muddier than either side wants to admit. A 2019 Journal of Dairy Sciencesystematic review by Beaver et al. found that extended cow-calf contact showed “beneficial or no effects” on calf health for scours and respiratory disease. A 2023 JDS perspective argued the practice “carries the risk of eroding public trust in the dairy industry if it is not addressed.”

Advocacy groups know Valentine’s Day — a holiday built on bonding — is the perfect moment to run campaigns about separating mothers from their calves. The default “you don’t understand farming” response stopped working years ago. Telling your calf management story with specifics, before someone else tells it about you, is the only play that actually works.

Your Cheese Board’s Other Credibility Problem

The chocolate next to your cheese carries its own baggage — and it’s baggage that makes your label look worse by association. The U.S. Department of Labor estimates 1.56 million children work on cocoa farms in the Ivory Coast and Ghana (Forbes, February 2025). Hershey, Mars, and Nestlé have repeatedly missed self-imposed deadlines to eliminate child labor from their supply chains. Brands emphasizing fair-trade sourcing — Taza Chocolate and Divine Chocolate — are capturing more Valentine’s spend as consumers connect the dots.

Here’s why this matters if you’re a dairy producer: consumers are building their Valentine’s cheese boards with the same ethical lens they use for chocolate. If the fair-trade bar on the board tells a better sourcing story than the wedge sitting next to it, that’s a comparison you lose at the point of sale. Jasper Hill closes that gap with specifics: regenerative grazing, whey recycling, and partnerships with small neighboring dairies that get premium pay for premium milk. Their approach keeps family-scale operations in Greensboro connected to a viable livelihood instead of the volatile commodity market.

Third-Party Proof: The Only Labels That Work

Verified certification is the antidote to consumer skepticism. Not all certifications carry the same weight, though — and the operational requirements differ more than most producers realize.

Certification

Cost to Farmer

Core Requirement

Audit Frequency

AGW Certified Animal Welfare Approved

Free — AGW covers all costs

Continuous outdoor pasture access, entire life

Annual on-farm audit

Validus CARE Certified

Processor-arranged

80%+ compliance across welfare, environment, and worker care

Annual third-party audit

Canada proAction + Blue Cow

Included in DFC membership

82 requirements across welfare, food safety, and biosecurity

Regular on-farm validation

Certified Grass-Fed Organic (OPT/EarthClaims)

Organic certification cost + verification

Zero grain, 60% DMI from pasture, 150-day grazing season

Annual third-party verification

AGW carries one of the highest welfare ratings from Consumer Reports, and the barrier to entry is lower than you’d think. Steffen Schneider at Hawthorne Valley Farm in Ghent, New York, put it simply: “It’s a wonderful service to provide free to farmers. People know it and look for it.” Timothy Haws at Autumn’s Harvest Farm in Romulus, New York, reported a 20% increase in sales after getting certified: “People love it!” Not sure if your operation qualifies? AGW offers free eligibility assessments — the cost of finding out is a phone call.

In Canada, Dairy Farmers of Canada ran its first-ever proAction consumer communication campaign in 2024, reaching 14.4 million Canadians and hitting an all-time high for Blue Cow Logo recognition — highlighting 57 environmental practices and 82 program requirements. What all these certifications share is straightforward: somebody who doesn’t work for you shows up, checks the books, and puts their name on it.

The Greenwashing Trap: 60% of Consumers Think You’re Faking It

The trust numbers are ugly everywhere anyone’s bothered to measure. In the U.S., 31% of consumers don’t trust companies to be honest about their environmental impact (Mintel, Global Outlook on Sustainability 2024-25). Sixty percent agree that many companies are “just pretending.”

“60% of U.S. consumers agree that many companies are ‘just pretending’ to be sustainable.” — Mintel, Global Outlook on Sustainability: A Consumer Study 2024-25

In the UK and Germany, the Changing Markets Foundation’s “Feeding Us Greenwash” report (March 2023, YouGov polling) found trust in sustainability claims on meat and dairy averages roughly 15%, with 59% expressing high concern about greenwashing. The Foundation flagged JBS for net-zero claims, Nestlé for carbon-neutral KitKat labeling, and Danish Crown for calling pork “climate controlled” — plus widespread use of idyllic pasture imagery on products from confined operations.

You might not be Nestlé. But if your local co-op’s marketing materials feature rolling green pastures and contented cows while the actual operation looks nothing like the brochure, you’re the one holding the reputational risk when a journalist or advocacy group comes knocking. A 2025 Corporate Climate Responsibility Monitor found that major food companies “exploiting loopholes in voluntary standards,” and Danone stands out as one of the few dairy-adjacent companies to have set a specific methane-reduction target (30% from fresh milk by 2030). Mintel’s Richard Cope noted that greenwashing education now feeds consumer skepticism more than engagement. Numbers, not slogans.

What This Means for Your Operation

If you ship a commodity to a co-op, you don’t control the retail label, but you shape what your processor can credibly claim. Your co-op is sitting on a consumer-facing story that 99% of the U.S. milk supply already qualifies forthrough FARM, covering 31,000+ farms across 49 states. In Canada, proAction is mandatory.

Can’t change your system? Change your communication. DFC reached 14.4 million Canadians with proAction messaging in 2024. If your processor isn’t generating equivalent consumer-facing value, put this on your Q2 2026 board agenda with a specific ask: What’s our consumer-facing welfare communication plan? Which retail accounts are deploying it? And why isn’t 99% FARM participation translating into any brand value at the shelf?

If you sell through regional brands or specialty processors, this is where certification ROI gets tangible. AGW certification costs you nothing — no audit fees, no annual charges, plus free marketing support. The operational hurdle is real — you need pasture access, and you need to meet their welfare standards, full stop. If your operation is confinement-based, AGW isn’t your path. Look at Validus CARE or push your processor to leverage FARM communication instead. Timothy Haws at Autumn’s Harvest Farm reported a 20% sales increase after becoming AGW-certified. And organic dairy commands $2.63 per half gallon over conventional at retail (USDA AMS, February 2026), with farm-gate organic pay reaching $40–$50/cwt in 2025 versus a Class I base of $14.70. One caveat worth being honest about: organic transition takes 36 months and carries real costs during the conversion period. The premium exists, but the runway to capture it isn’t short.

If you sell direct-to-consumer or artisan, you own the customer relationship. Valentine’s is your moment. Build a holiday offer around the specifics that differentiate you — not a generic “sustainable” badge. Jasper Hill does it with regenerative grazing, whey recycling, and partnerships that keep neighboring small dairies viable. Alexandre Family Farm does it with Regenerative Organic Certification, A2/A2 genetics, and a multi-generational family story — retailing at $7.49–$8.89 for less than a half gallon. Wisconsin’s Roelli Cheese Haus does it with craft and provenance.

The trade-off nobody talks about: Telling your welfare story proactively invites scrutiny. Someone will ask harder questions. But the alternative — staying silent while advocacy groups and competitors write the narrative about your practices — is worse. The von Keyserlingk research is unambiguous: consumers who learn about standard dairy practices don’t become more accepting of them. They become more concerned. Control the story, or it controls you.

What to Do Before Next Valentine’s Day

Build a holiday communication calendar now—and start six weeks out. Wisconsin Cheese launched “Wedges of Love” on January 20, a full 25 days before February 14. That’s the lead time that works. Valentine’s Day, Mother’s Day, and Christmas are your three highest-visibility moments. Plan your social media, farm tour invites, and retail signage around these dates—they’re when consumers are most emotionally primed to care about how their food is produced.

Lead with animal welfare, not carbon. Pan-European research (Agrarforschung Schweiz, 2024) confirms consumers rank welfare above environmental sustainability when choosing dairy. If your messaging leads with carbon footprint, flip the order.

Pursue the certification that fits your system. AGW costs nothing and delivers measurable results, but it requires pasture access. Confinement operations should push processors to activate FARM or Validus communication at retail. Canadian producers should demand that their co-op leverage proAction and the Blue Cow more aggressively.

Get specific about calf management. Publish your calf care protocol on your website or in your direct-to-consumer materials. Vague assurances don’t work. Specifics — colostrum timing, housing design, health protocols, how long calves stay with dams, if applicable — do.

Audit your own label for greenwashing risk. If you use words like “sustainable,” “humane,” or “natural” without third-party verification, you’re one investigative journalist away from a credibility crisis. Only 14% of consumers trust those claims as it stands. Either back them up or remove them.

Run the premium math for your operation. Organic half-gallon commands $2.63 over conventional at retail. AGW-certified Autumn’s Harvest reported a 20% sales lift. Maple Hill retails at 4x conventional — and was attractive enough for Horizon Family Brands to acquire outright in December 2025. What would even a fraction of that premium mean for your bottom line?

Every Valentine’s Day, millions of consumers make choices that signal what they value. Those signals are getting louder, more specific, and harder to ignore. When a consumer picks up your product on February 14th, does your label tell a story that holds up — or one that falls apart the moment they Google it?

Key Takeaways

Stop betting on vague claims. Only 14% of consumers believe dairy sustainability labels, but research shows they care most about animal welfare, not carbon slogans.

Follow the money, not the noise. Welfare-backed and organic brands like Jasper Hill, Maple Hill, Alexandre Family Farm, and AGW-certified herds are already seeing $2.63/half-gallon retail premiums and $40–$50/cwt farm-gate pay versus a $14.70 Class I base.

Use the programs you already have. FARM and proAction cover almost all U.S. and Canadian milk, and pasture-based herds can add AGW, Validus, or Regenerative Organic Certification on top — but they only pay if you turn them into a clear welfare story on your label, website, and social.

Plan around “treat holidays.” Build a simple communication plan for Valentine’s Day, Mother’s Day, and Christmas that shows how you handle calves, pasture, and herd health — instead of letting activists or competitors define your practices.

Pick one concrete next step. Call AGW for a free eligibility check, push your co-op to activate FARM or proAction in retail messaging, or publish your calf-care protocol so shoppers don’t have to guess.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

The $1750 Calf: Is Your 2026 Breeding Plan Leaving $800 a Head on the Table? – Secure your future herd while capturing massive beef-on-dairy premiums by weaponizing your genomic data. This guide breaks down the surgical breeding methods that turn surplus pregnancies into a high-margin revenue stream that significantly outpaces commodity milk income.

Tech Reality Check: The Farm Technologies That Delivered ROI in 2024 (And Those That Failed) – Master your next capital investment with verified payback periods for robotics, sensors, and AI. This reality check delivers the brutal gap between glossy brochures and barn-floor returns, ensuring your technology drives measurable margin instead of just adding complexity.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

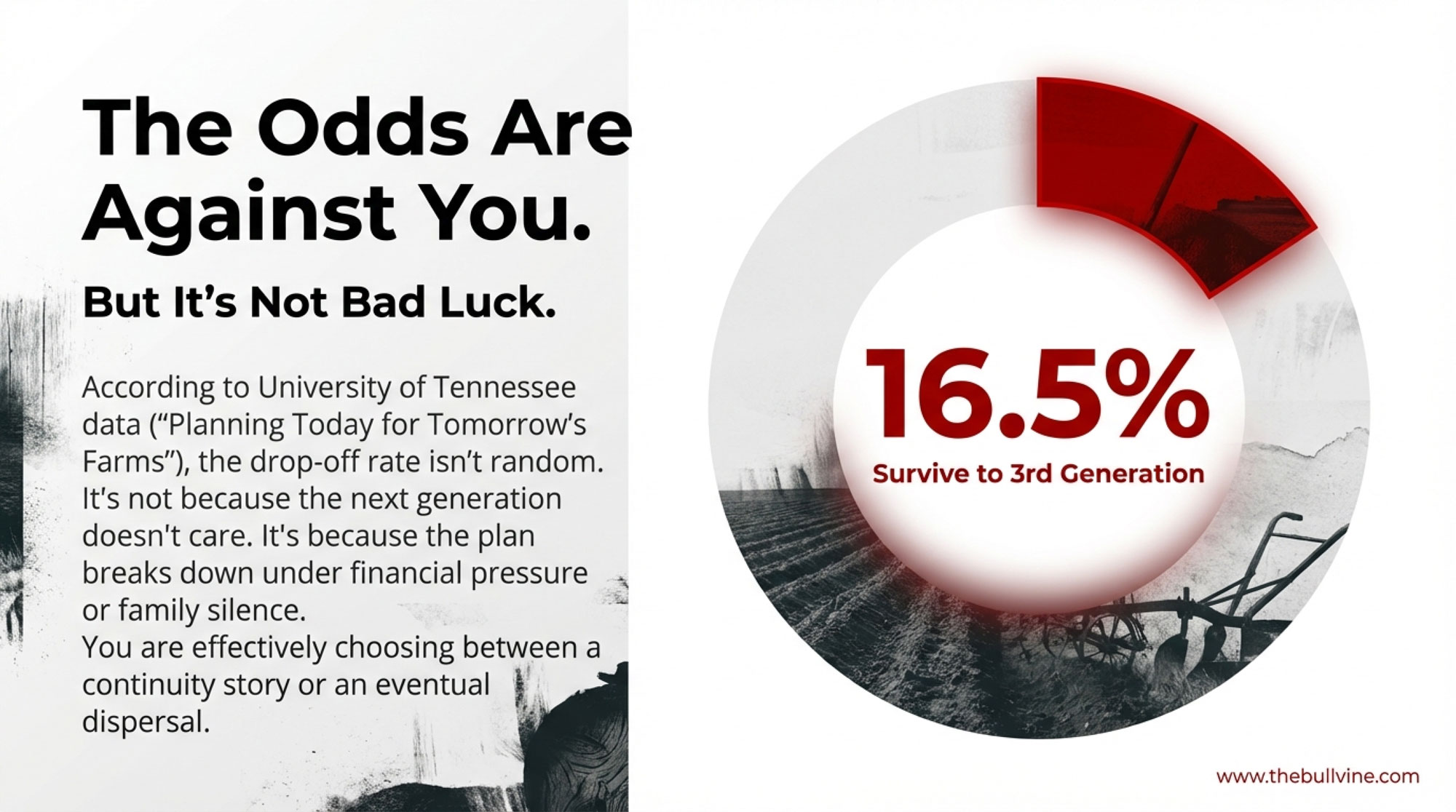

Your kid’s sweat equity is worth $0 without a signed agreement. A 2025 dairy farm court ruling just proved it the hard way.

Executive Summary: If your succession plan only lives in family conversations, this piece shows why that’s a bet you can’t afford to keep making. A 2025 Ontario court ruling in Metske v. Metske cut six years of a son’s sweat equity down to $31,700, because the family never put clear price, terms, or timelines on the transfer. At the same time, U.S. dairy farm numbers are down 39% in five years, farmland has more than doubled in value since 2010, and average net earnings sit around $592 per cow — a mismatch that makes “equal” inheritance almost impossible to cash‑flow. You see the flip side in Minnesota’s 150‑year Heusinkveld dairy, where education, scale, and structure give the next generation a real shot instead of just hopes and handshakes. The article walks you through why “equal” splits usually force a sale, while “equitable” transfers — separate entities for land and cows, earned buy‑ins, and written, bank‑vetted agreements — keep the doors open. You also get hard numbers to work with (4:1 max debt‑to‑EBITDA, 1.25+ term debt coverage, current FSA rates) and a 90‑day triage plan to start turning vague expectations into signed paper your lender and your kids can actually rely on.

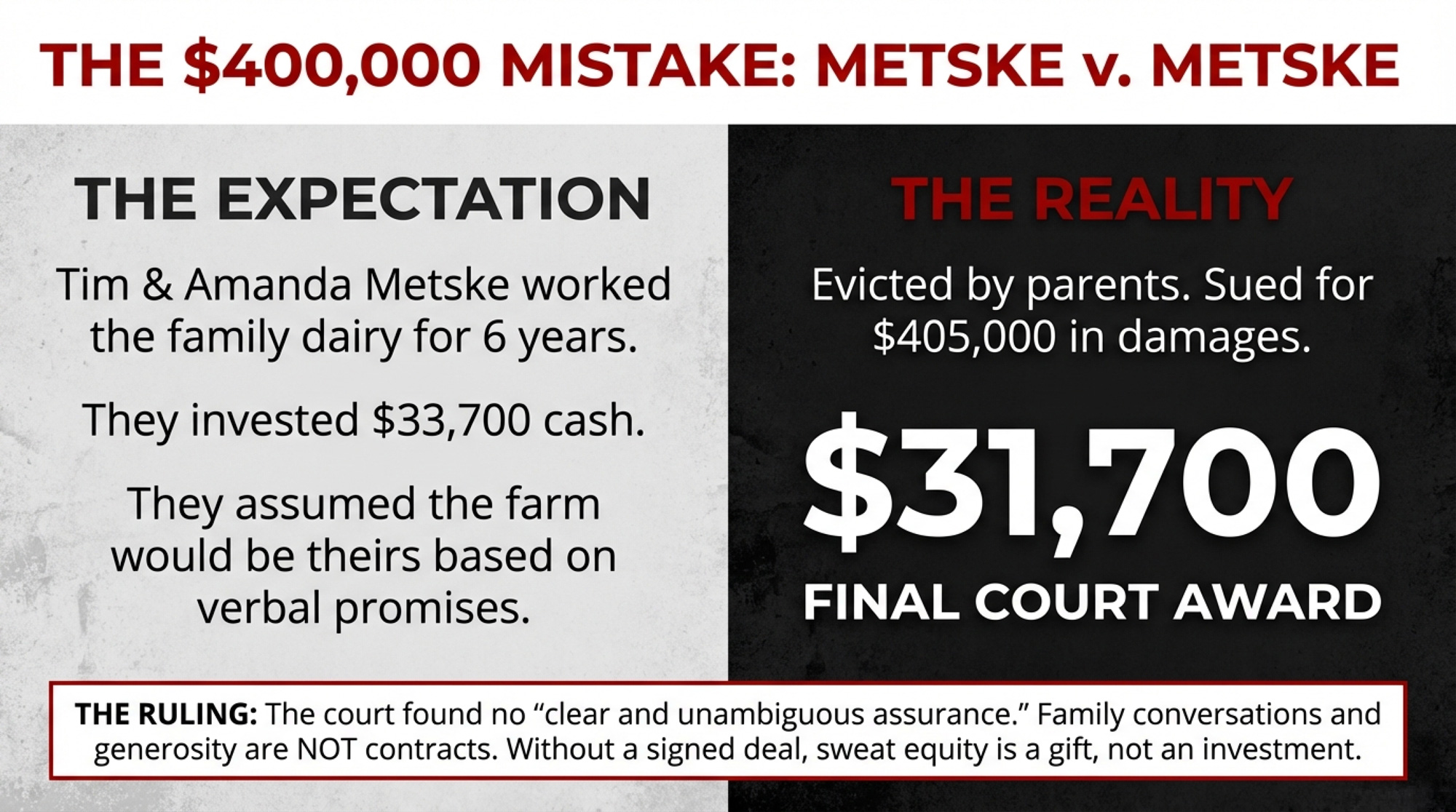

By every outward measure, Tim Metske was building his future. Starting around 2012, he and his wife, Amanda, ran his parents’ Ontario dairy — bought the herd from Martin and Roseanne Metske for approximately $90,000 (funded by a bank loan Martin co-signed), leased the quota, and drew up a business plan for the bank. They invested $33,700 of their own money in property improvements, including a furnace and repairs. The whole time, they operated under what the trial judge later described as “favourable but undefined” terms for eventually acquiring the land and buildings.

Nobody wrote anything down.

In April 2018, Roseanne told them to leave by the end of May. Forced off the land and without the dairy quota attached to it, they disposed of the herd at a loss and sued. The trial judge awarded $405,000 in damages. Martin and Roseanne appealed. In 2025, the Ontario Court of Appeal — in Metske v. Metske, 2025 ONCA 418 — overturned the bulk of that award and reduced Tim and Amanda’s recovery to $31,700: the net value of tangible improvements minus $2,000 in damages to the farmhouse.

Six years of sweat equity, reduced to a number smaller than the original investment. The court couldn’t build a structure that the family never built.

Why the Court Ruled the Way It Did

The Court of Appeal’s reasoning exposes exactly why informal dairy farm succession plans collapse.

The court found no “clear and unambiguous assurance.” The Metskes’ family conversations never crystallized beyond a willingness to negotiate. Price, financing, timing, and even which properties were included — all remained undefined. An “agreement to agree,” the court held, isn’t enough to ground a legal claim.

Here’s the part that should keep every dairy family up at night: Tim and Amanda’s own business plans worked against them. The documents they’d prepared for the bank showed acquisition at fair market value. The Court of Appeal said this contradicted any claim of a promised below-market deal. Martin’s past generosity, even Roseanne’s warm words at the wedding, weren’t enough to establish “donative intent”.

And the financial reality sealed it. When Tim tried to secure financing for the dairy quota in 2013, the bank insisted on a 10-year amortization, which the projected cash flow couldn’t support. From that moment forward, the contemplated succession was financially dead — but nobody acknowledged it for another five years.

As Lerners LLP noted in their analysis: proprietary estoppel “protects against the unfairness of a promisor resiling from a promise, not against the commercial risk of an aspirant purchaser who cannot perform”.

The law can’t save you from a plan that was never a plan.

What Is Proprietary Estoppel — And Why Should You Care?

You’ve probably never heard this term. But if your succession “plan” is built on verbal promises, it’s the legal concept that will decide your family’s future.

Proprietary estoppel is a legal claim that arises when one person relies on another’s promise regarding property — and suffers a loss when that promise is broken. In farm succession disputes, the incoming generation typically argues: “You told me I’d get the farm, I worked for years based on that promise, and now you’ve pulled the rug out.”

The Metske ruling shows how hard it is to win this claim. Ontario’s Court of Appeal required a “clear and unambiguous assurance” — not vague encouragement, not general family goodwill, not a willingness to negotiate someday. The court also demanded proof that the promise was specifically intended as a commitment, not just an optimistic conversation. Tim and Amanda’s own bank documents — showing they expected to buy at fair market value — contradicted any claim of a guaranteed below-market deal.

The bottom line: “My dad said I’d get the farm” is not a contract. It’s not even close. If the terms aren’t written, signed, and witnessed — with independent legal advice for both sides — they don’t exist in the eyes of the law.

The Numbers Behind the Crisis

The Metskes aren’t an outlier. They’re a pattern.

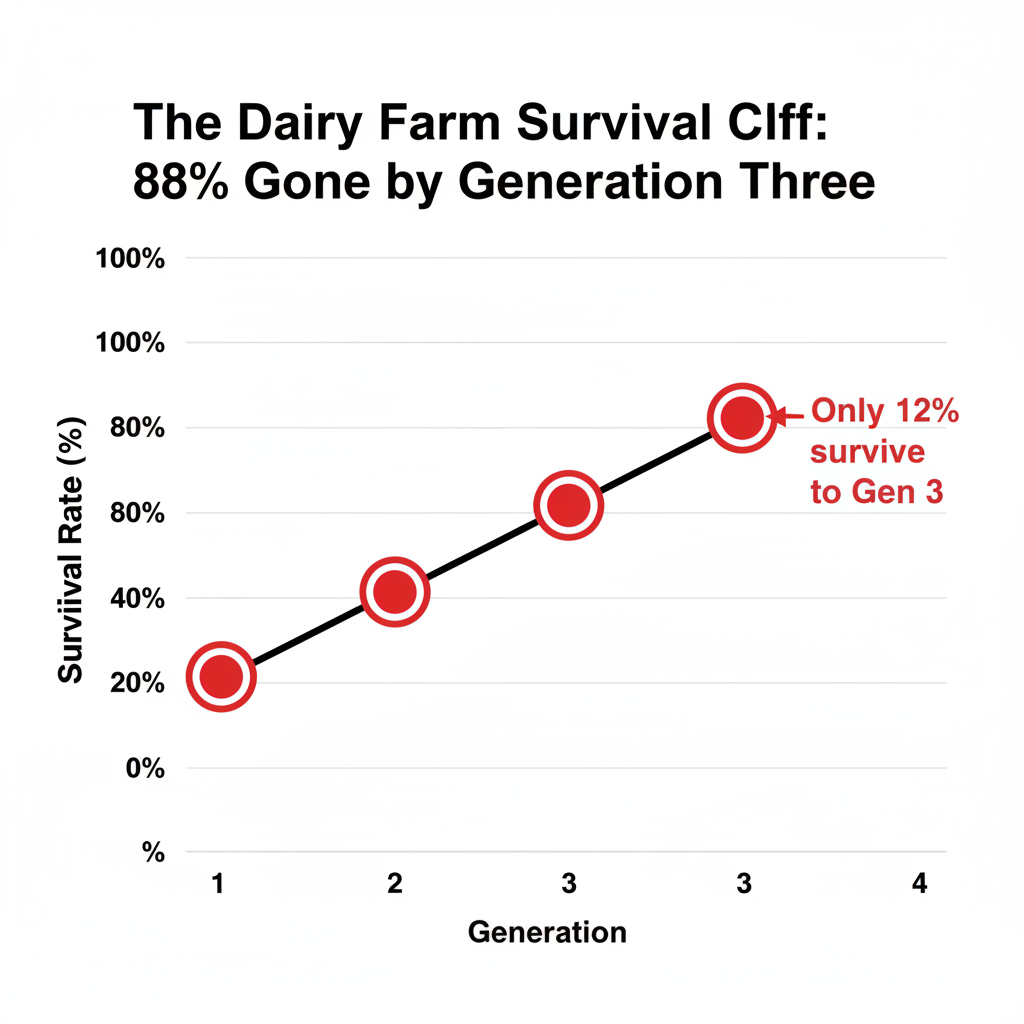

Ron Hanson, professor emeritus at the University of Nebraska, has spent his career studying farm succession. His numbers: 30% of family farms survive to the second generation. Just 12% make it to the third. Only 3% reach the fourth. John Ward’s foundational 1987 research at Northwestern’s Kellogg School of Management found similar results across all family businesses — roughly 30% to the second generation, 10–15% to the third.

Nearly 9 in 10 family farms don’t survive to see a third generation at the helm. Not because the kids don’t want the farm. Because nobody built the structures to make the transfer work.

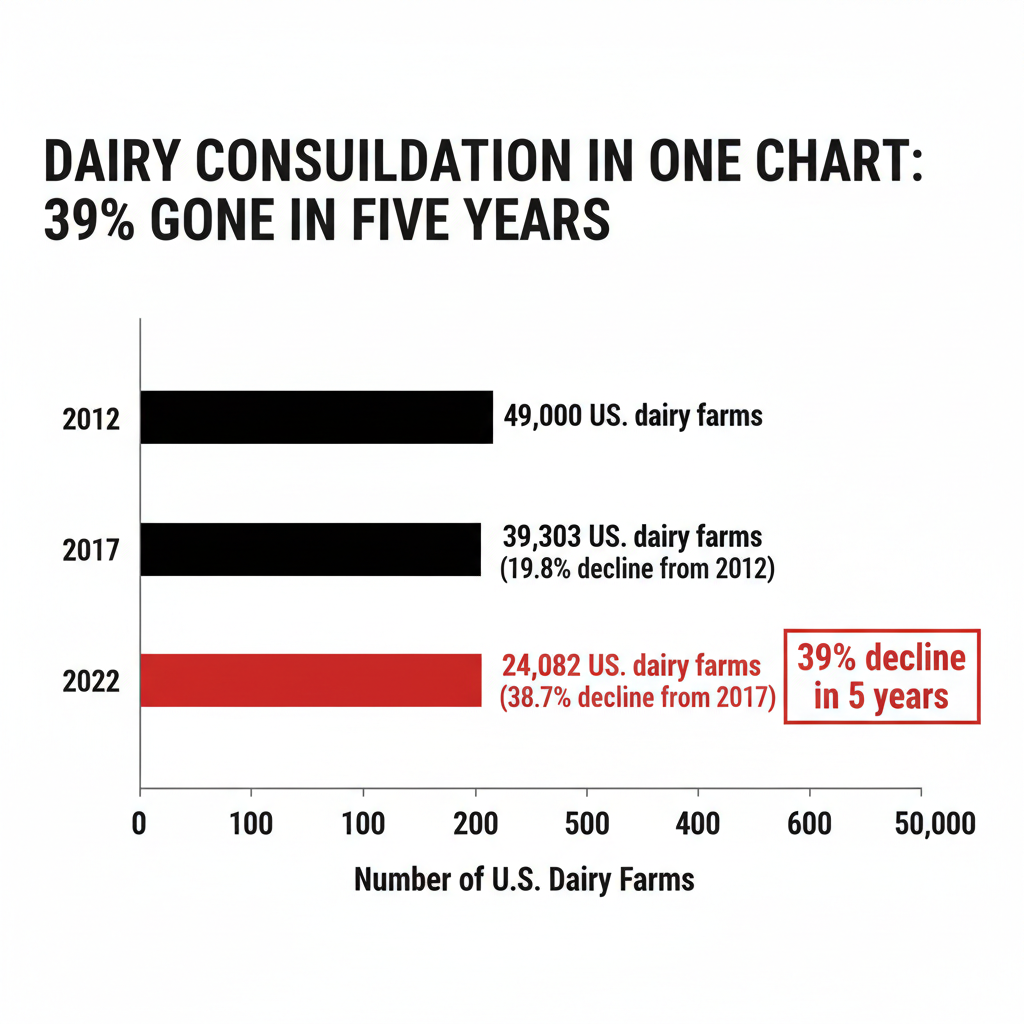

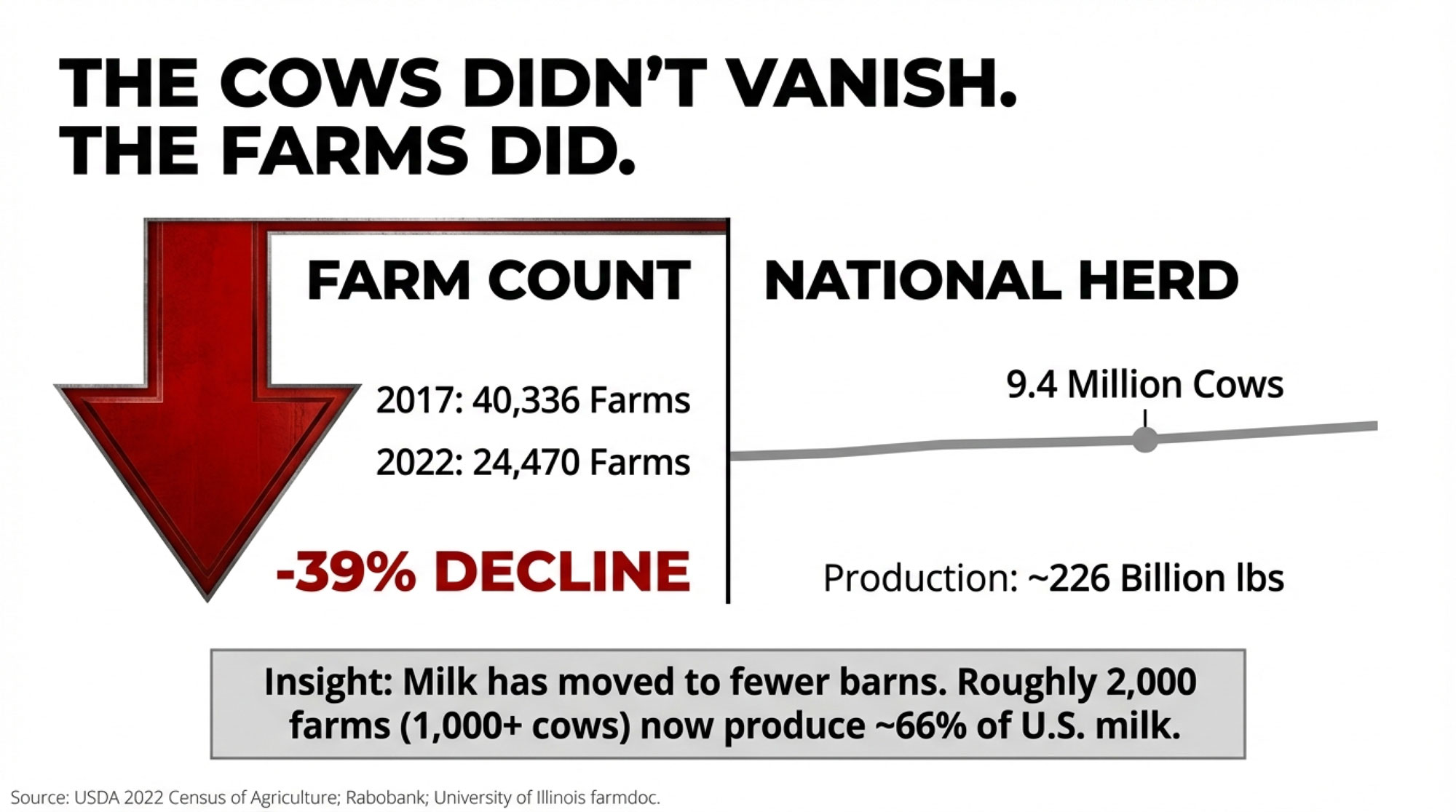

The consolidation data tells the same story from a different angle. The 2022 USDA Census of Agriculture shows U.S. dairy farms dropped from 39,303 operations in 2017 to 24,082 in 2022 — a 39% decline in five years, and 51% down from 2012. Canada tracks the same direction: the Canadian Dairy Information Centre reports 12,007 dairy farms in 2014, down to 9,256 by 2024 — a steady 2.6% annual decline. Wesley Tucker, MU Extension agriculture business specialist, puts the pipeline in even starker terms: 70% of farms are projected to trade hands in the next 20 years.

Farms with 1,000 or more cows — roughly 2,013 operations, about 8% of all U.S. dairies — now produce approximately two-thirds of the country’s milk, according to Rabobank analysis. The mid-size family dairy is getting squeezed from both ends: too big to walk away from, too asset-heavy to hand off without a structure in place.

This article draws on an Ontario court ruling, Canadian farmland data, U.S. census figures, and a Minnesota family operation. The legal frameworks differ at the border — Canadian supply management and quota add layers that the American system doesn’t have, and property law varies province to province and state to state. But the math and the human nature remain the same. Families that don’t formalize their plans lose the farm, whether it’s sitting on 500 acres outside Guelph or in Fillmore County, Minnesota.

Why the Math Keeps Getting Worse

The asset-value problem isn’t easing up. It’s accelerating.

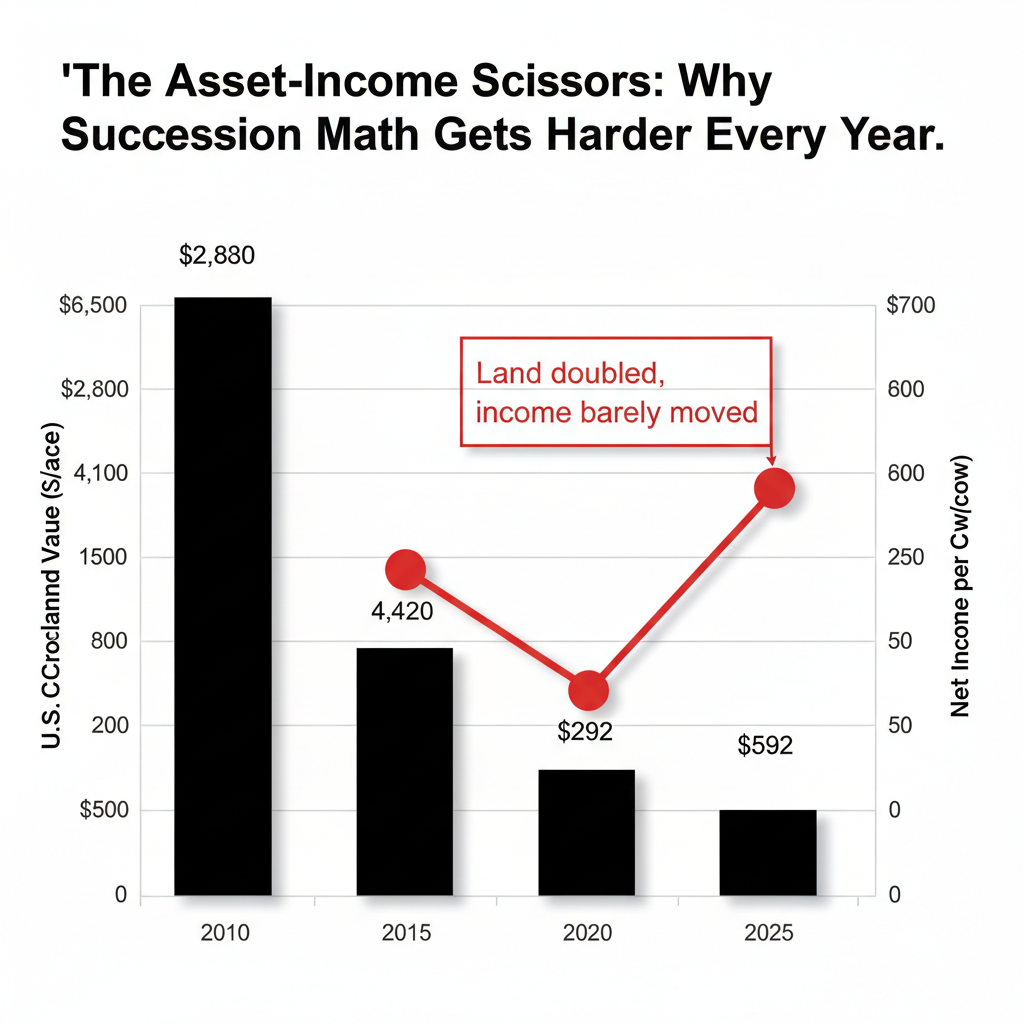

U.S. farm real estate averaged $4,350 per acre in 2025, up 4.3% year-over-year and more than double the $2,150 average in 2010, according to the USDA’s August 2025 Land Values Summary. Cropland specifically hit $5,830 per acre — up 4.7% from the prior year, compared to $2,980 in 2011. In major dairy states, the numbers climb higher: Michigan farmland jumped 7.8%, and Iowa cropland averaged $10,300 per acre.

North of the border, Farm Credit Canada’s mid-year 2025 review showed Canadian cultivated farmland values rose 6.0% in the first half of 2025 alone, a slight acceleration from the 5.5% growth in the same period of 2024. Over the 12 months from July 2024 to June 2025, Canadian farmland appreciated 10.4%. Manitoba led the nation at 11.2%, while Ontario farmland values held flat.

Now stack those asset values against what milk actually pays. Zisk projections for 2025 ranged from $531 to $1,640 per cow, depending on region and herd size. A 2024 Northeast Dairy Farm Summary pegged average net earnings at $592 per cow, up from $292 the year prior. Better than 2023, sure. But $592 per cow against land that doubled in 15 years — that’s the succession math in one sentence.

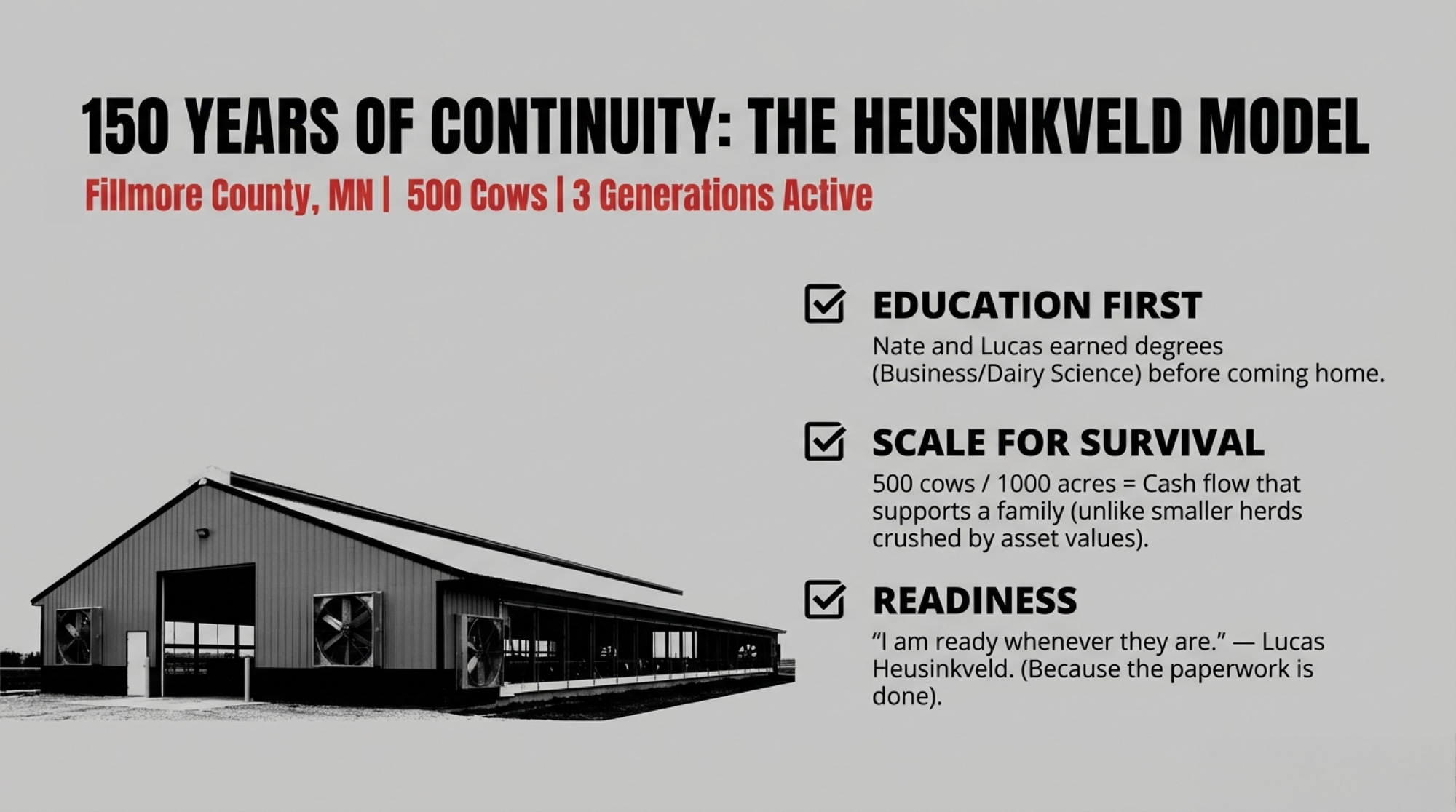

What 150 Years of Continuity Looks Like

In Fillmore County, Minnesota, the Heusinkveld dairy tells a different kind of story.

The operation has run continuously for about 150 years — a milestone the Fillmore County Journal covered in April 2024. Jeff and Steve Heusinkveld took their turn running the farm in 1970. Jeff’s son, Nate — an agri-business management degree from Mankato State — came back to take over. He married Misty in 2000 and moved onto the farm.

Today, Nate runs the operation. Jeff has since passed away, but Nate’s mother, Darla, still lives on the farm and handles the calf chores. The dairy has grown to 500 cows — 450 milked three times daily through a double-12 parallel parlor — plus 85 beef cows. They crop 350 acres of hay and 550 acres of corn, and seven full-time employees round out the crew.

The next generation is already in the barn. Nate’s son Lucas earned a dairy science degree from NICC Calmar, Iowa, and works alongside his dad every day. “I am ready whenever they are,” Lucas told the Fillmore County Journal — talking about the day Nate and Misty decide it’s his turn.

What jumps out about this family: education before entry. Nate got his business degree, and Lucas got his dairy science degree, both before coming home. And 500 cows on nearly a thousand crop acres generates the kind of cash flow that can actually support a transition — unlike operations where asset values dwarf annual income by a factor of 10 or more.

The Inheritance Math That Breaks Most Transitions

Farm Credit Canada’s transition resources put it bluntly: “unspoken expectations are the silent killers of transition plans.” Their guidance notes that agriculture has a deeply ingrained pattern of assumed succession — “Either the parent assumes a particular child will farm, or a child thinks they’ll get the farm — but they’ve never had a conversation about it”.

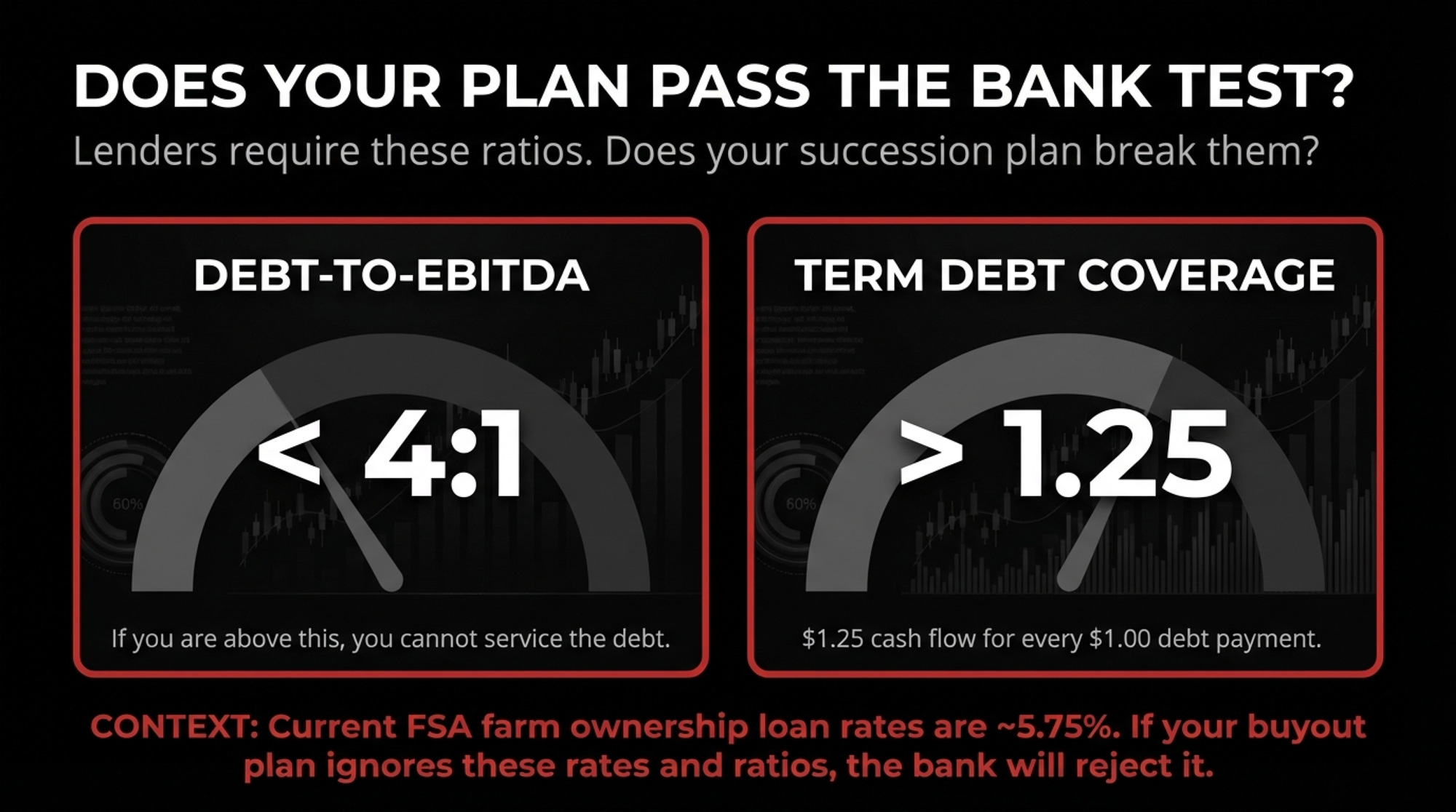

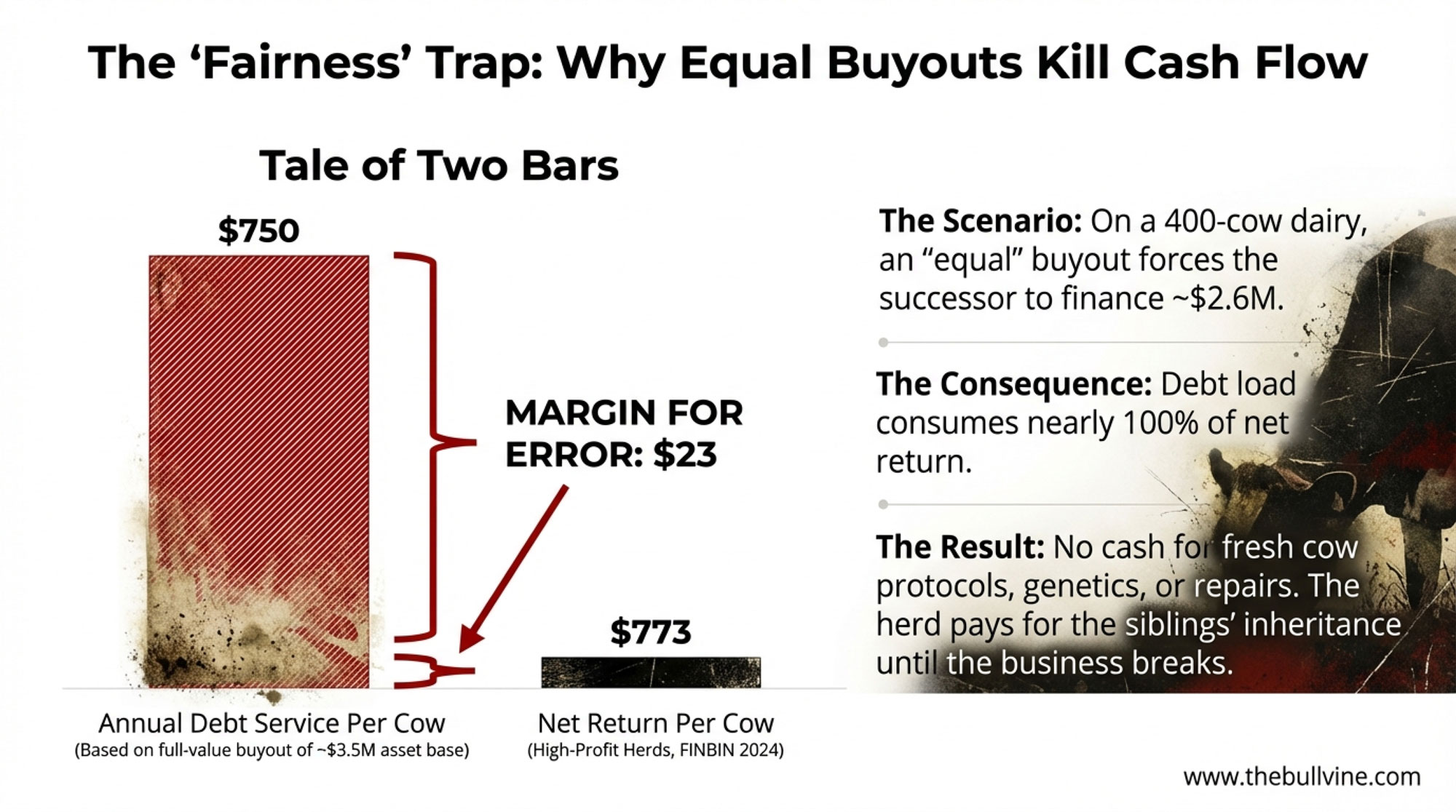

When parents want to treat all kids “equally,” the farming heir has to buy out siblings at asset-value prices, somehow using cash-flow-level income. At $5,830 per acre for U.S. cropland, a 500-acre operation’s land alone is worth $2.9 million before you count cattle, equipment, or buildings. Now run the debt math. Analysts recommend staying below a 4-to-1 debt-to-EBITDA ratio to cash flow expenses and meet scheduled debt payments. Penn State Extension notes that many lenders require a term debt coverage ratio of at least 1.25 — meaning the farm generates $1.25 in cash flow for every $1.00 in scheduled intermediate- and long-term debt payments — just to consider a plan viable. They flag 1.75 or better as the green zone.

So ask yourself: if your successor takes on $2.9 million in land debt alone at current FSA rates of 5.750% for farm ownership loans, can that 500-cow herd, generating $592 per cow in net earnings, cover the payments and still operate? One tough milk year tips the balance. Two tough years and you’re looking at a forced sale.

As agricultural attorney Trent Hilding told the Michigan State Dairy Extension podcast: “In a lot of cases, for the farms to be viable and successful, they do have to transfer in a fashion that’s not equal.” But he added, “it still could be considered equitable and fair.”

Equal vs. Equitable: Why the Distinction Decides Your Farm’s Future

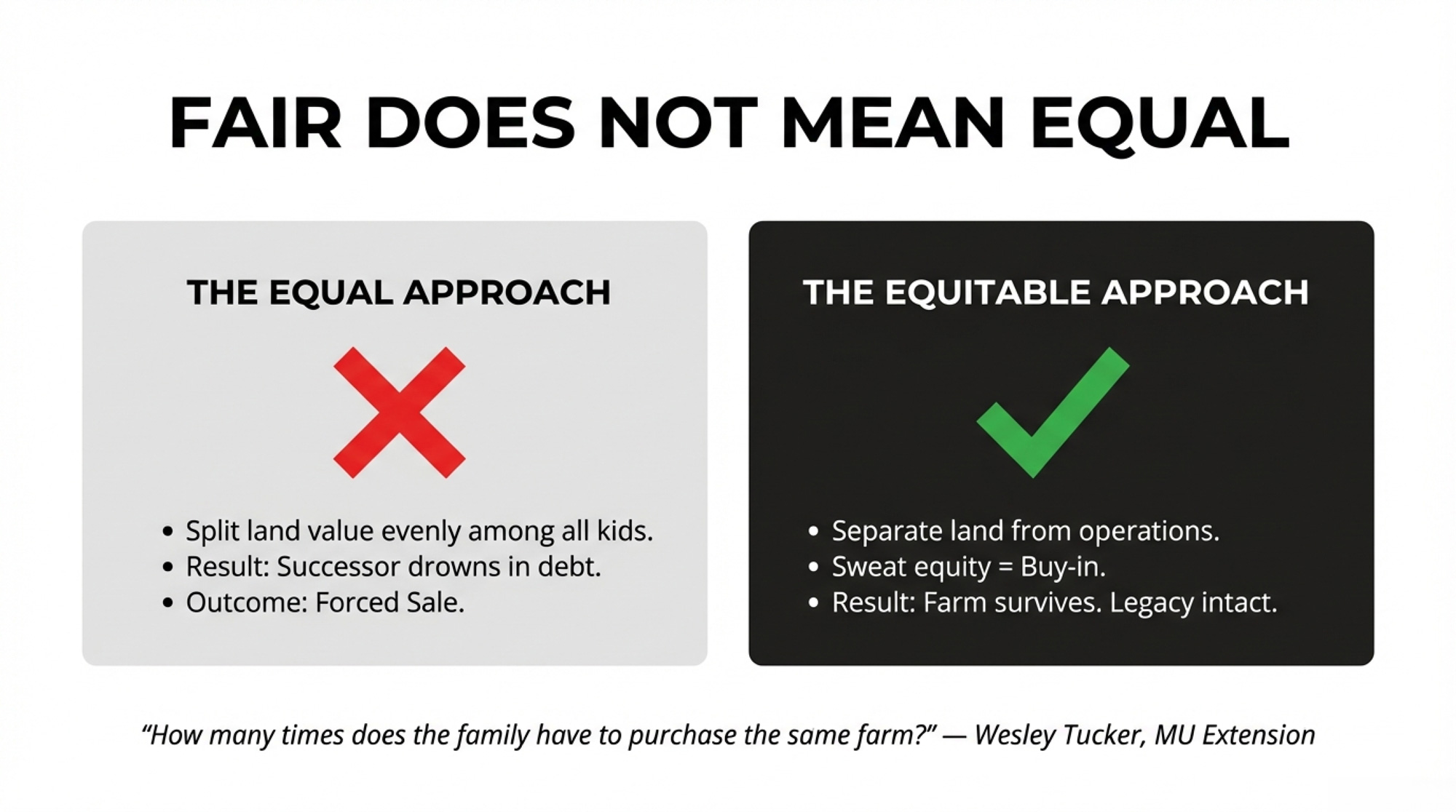

Most families default to “equal.” Split everything evenly among the kids. It feels right. It isn’t. Here’s how the two approaches play out:

The “Equal” Approach

The “Equitable” Approach

Land & Assets

Divide the total land value by the number of children. Each gets an equal dollar share

Separate operational assets from land ownership using distinct entities. Farming heir acquires the operation; land held separately

Sibling Buyout

Farming heir must buy out siblings at full fair market value — $2.9M+ on a 500-acre operation at $5,830/acre

Use long-term leases, gradual equity earn-in, or infrastructure investment counted as buy-in. As Wesley Tucker asks: “How many times does the family have to purchase the same farm?”

Documentation

Reliance on handshake agreements and family goodwill — exactly the approach the Metske court rejected

Written, witnessed, and bank-vetted contracts with independent legal advice for both parties

Debt Load

Successor likely exceeds the 4:1 debt-to-EBITDA threshold and fails the 1.25 term debt coverage minimum before day one

Debt sized to what milk actually generates — $592/cow — with payments structured to maintain viability

Typical Outcome

Forced sale or bankruptcy. The Metske family got $31,700 after six years.

Multi-generational continuity. The Heusinkveld family just passed 150 years.

The families that survive figure out something the rest don’t: the “inheritance fairness” problem and the “business continuity” problem are two separate challenges that need two separate solutions. Blending them together is what kills the farm.

How to Structure It So the Farm Survives

Hilding’s advice provides a practical starting framework:

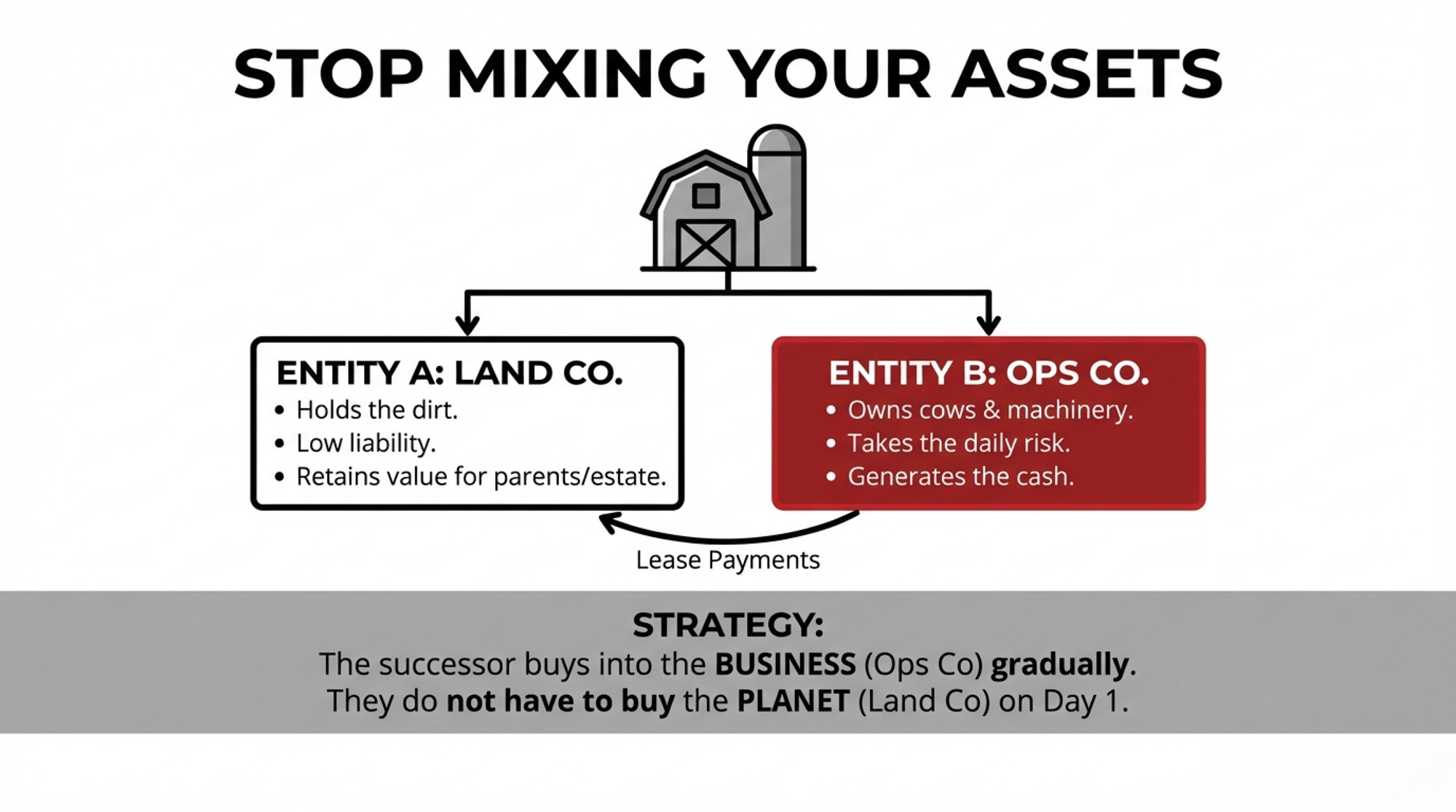

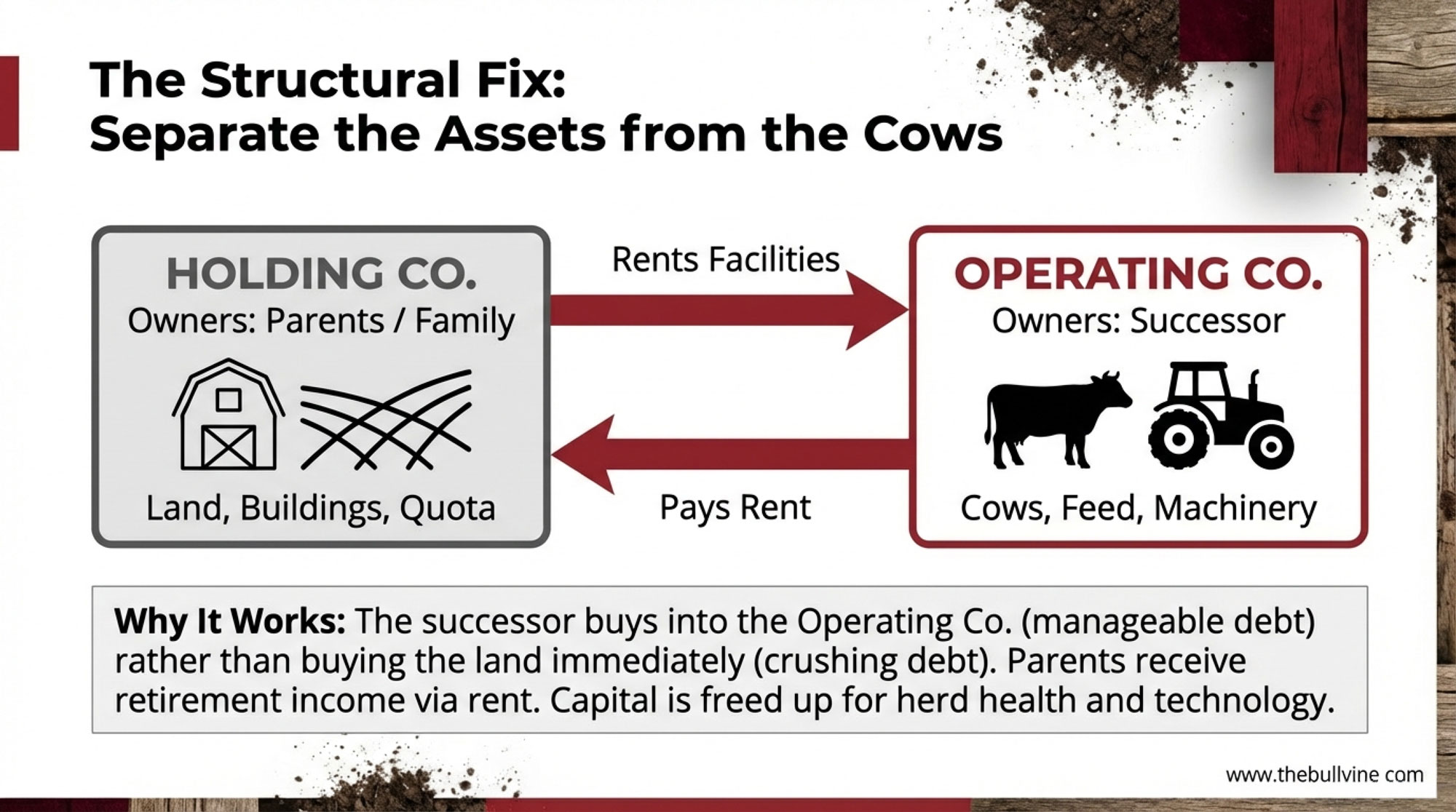

Separate operations from real estate. Establish one entity for the dairy operation and another to hold the real estate. “The real estate is a key investment you want to be separate from your liability, your employees, and the risk factors you have in your operation,” Hilding said. An incoming generation can’t afford to buy everything at once. Separating the assets gives everyone room to work. One trade-off to flag: entity separation adds legal and accounting overhead, and if structured carelessly, it can trigger tax consequences. Get advice specific to your province or state before you file anything.

Get the base documents done. A will or trust is the foundation. “No matter your age or amount of assets, having who you want in charge in writing makes a big difference,” Hilding advised.

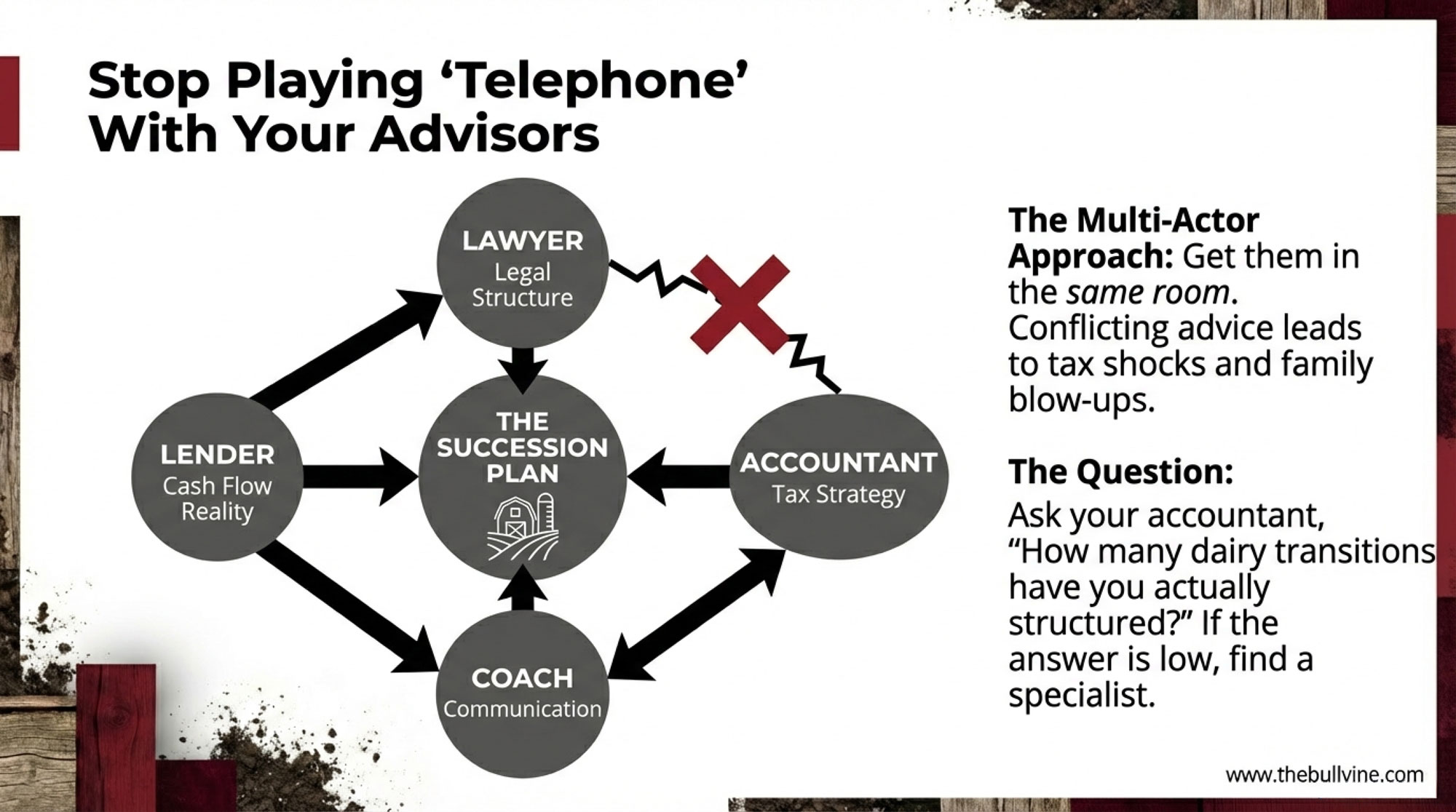

Start the financial transparency early. The biggest misstep Hilding sees: the older generation withholding too much information, usually because they’re afraid of losing control. His advice — involve farming heirs in regular financial meetings and discussions with the lender. “Just because we do something on paper doesn’t mean you’re not showing up and aren’t part of the farm”.

Reagan Bluel, MU Extension dairy specialist, wrote in August 2025 that there’s another angle worth considering: treat infrastructure reinvestment as “buy-in”. When the incoming generation invests in a new parlor or freestall expansion that improves net income for everyone, that investment should count toward their stake. “When you include the purchase of the land in addition to a major piece of infrastructure, such as a parlor, the cash flow rarely works,” Bluel wrote.

Bluel sees this play out in real time across Missouri operations. “I recall hearing a prevailing statement by the older generation over and over when talking to farm families, ‘I didn’t have this farm given to me,'” she wrote. That pride is real — but so is the math. The assets needed for a dairy to succeed today are vastly different from 40 years ago, and Missouri land prices alone have increased an average of 6% annually over time.

What the Metske Ruling Teaches About Documentation

The Lerners LLP analysis of the court decision reads like a checklist of what the Metske family should have done:

Kill the “agreement to agree.” An outline without price, payment schedule, or valuation mechanism leaves your successor exposed. The court specifically rejected the idea that ongoing negotiations equal binding commitments.

Document the journey, not just the destination. Incremental steps — such as sales, quota leases, and vendor-takeback loans — need to be recorded and cross-referenced to a future transfer agreement. A memorandum of understanding, supported by independent legal advice for both parties, bridges the gap between kitchen-table discussions and enforceable agreements.

Align financing with the plan from day one. Tim and Amanda’s inability to secure lending doomed the succession before it started. Bring the lender in early. Confirm serviceability. Match payments to what the operation actually generates.

Make any below-market terms explicit. If you genuinely intend to offer your kid favorable pricing, write it down. Promissory notes. Side agreements. Signed and witnessed. The court rejected the notion that general family generosity amounts to a binding commitment.

Ontario producers have a free resource most haven’t opened: Publication 70, the Ministry of Agriculture’s Farm Succession Planning Guide — 120 pages covering business organization options, operating agreements, ownership transfer methods, and taxation implications.

Factor

Documented Succession Plan

Undocumented (Metske Case)

Written Agreement

Signed purchase agreement with price, terms, timeline, and independent legal advice

None—”agreement to agree” rejected by court

Equity Recognition

Years of sweat equity and capital improvements credited toward purchase price or ownership stake

$33,700 in improvements reduced to $31,700 net after damages

Bank Involvement

Lender pre-approves financing structure; cash-flow viability confirmed before transfer

Bank refused 10-year quota financing in 2013—plan was already dead

Parental Intent

Donative intent (below-market terms) explicitly documented and tax-structured

Business plans showed FMV purchase—no proof of gifting intent

Dispute Resolution

Binding arbitration or mediation clauses; clear exit terms if plan changes

Six years of litigation; family relationships destroyed

Legal Outcome

Enforceable ownership transfer; successor builds generational wealth

Trial award of $405,000 overturned to $31,700 on appeal

Multi-Gen Continuity

Farm survives to generation three (12% club)

Farm lost; 88% attrition statistic

Why “Eventually” Is the Most Dangerous Word in Succession

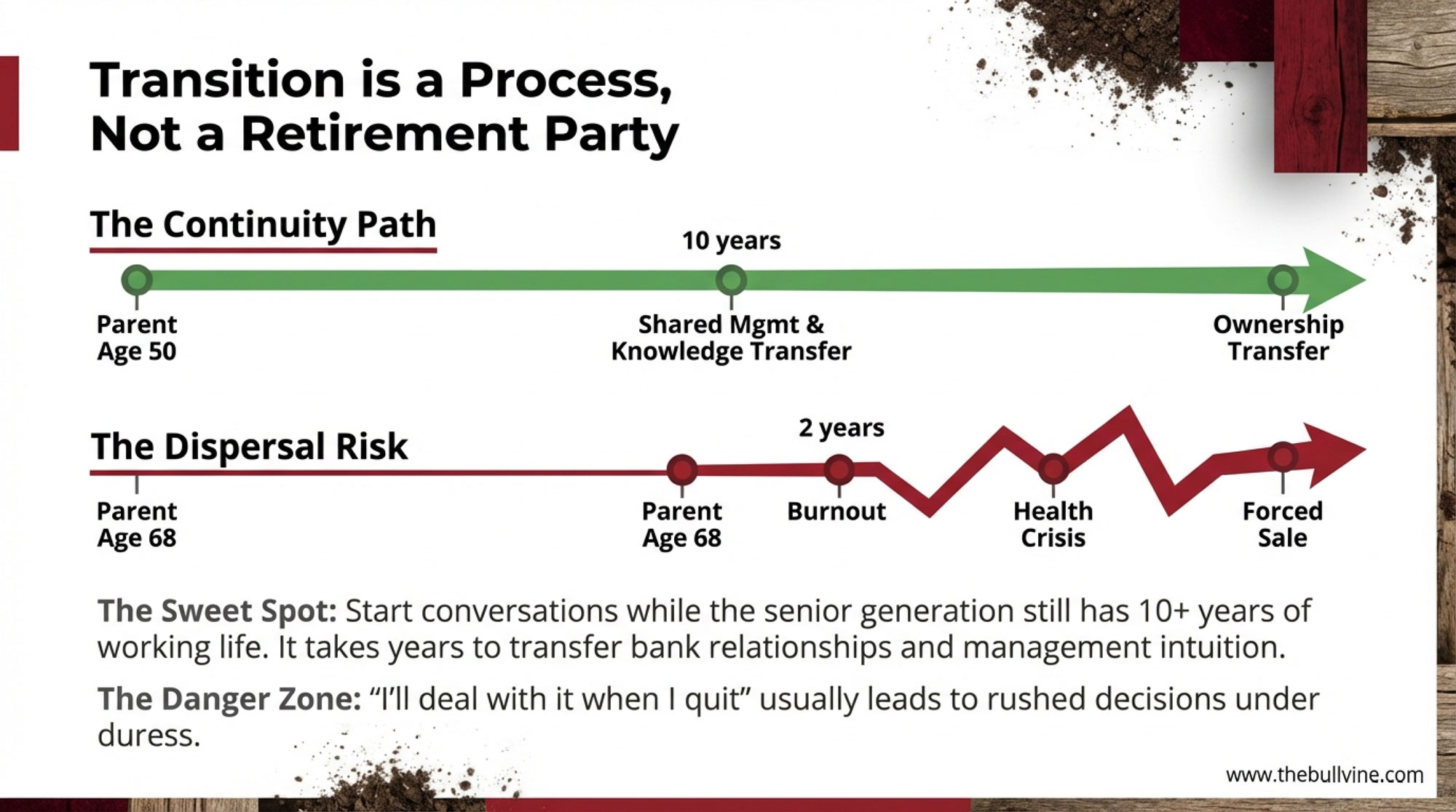

Hanson told Brownfield Ag News that this is exactly what families avoid. “To someday admit that I may not be on my farm, or I may not be operating or managing my farm, is very hard for a lot of farm producers,” he said. FCC’s transition resources don’t sugarcoat it: “Farm transition planning that starts at a funeral is a worst-case scenario”. That’s why advisors recommend starting 10–15 years out — not because the paperwork takes that long, but because restructuring entities, transferring equity, and getting everyone comfortable with a plan that’s fair but not equal all take time you can’t manufacture in a crisis.

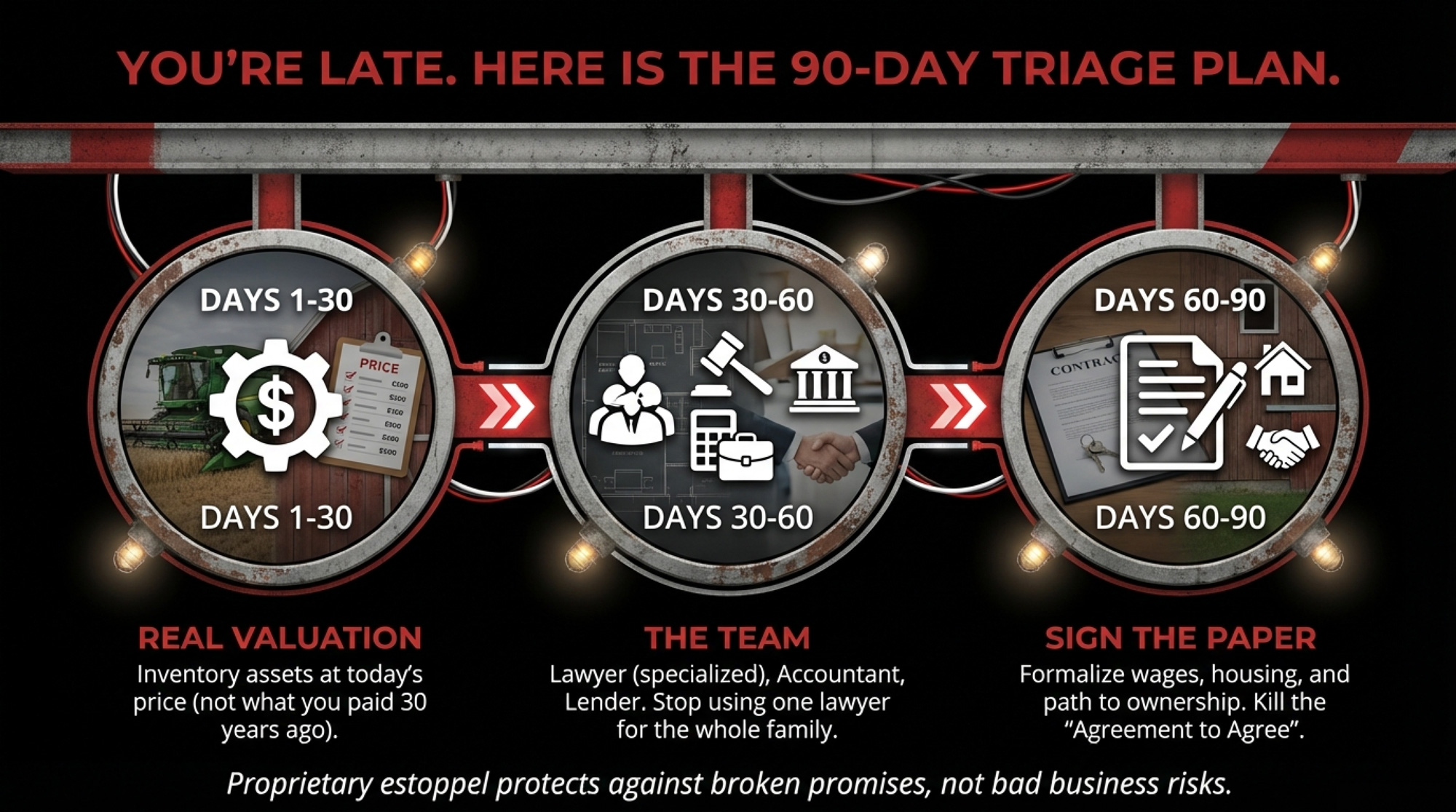

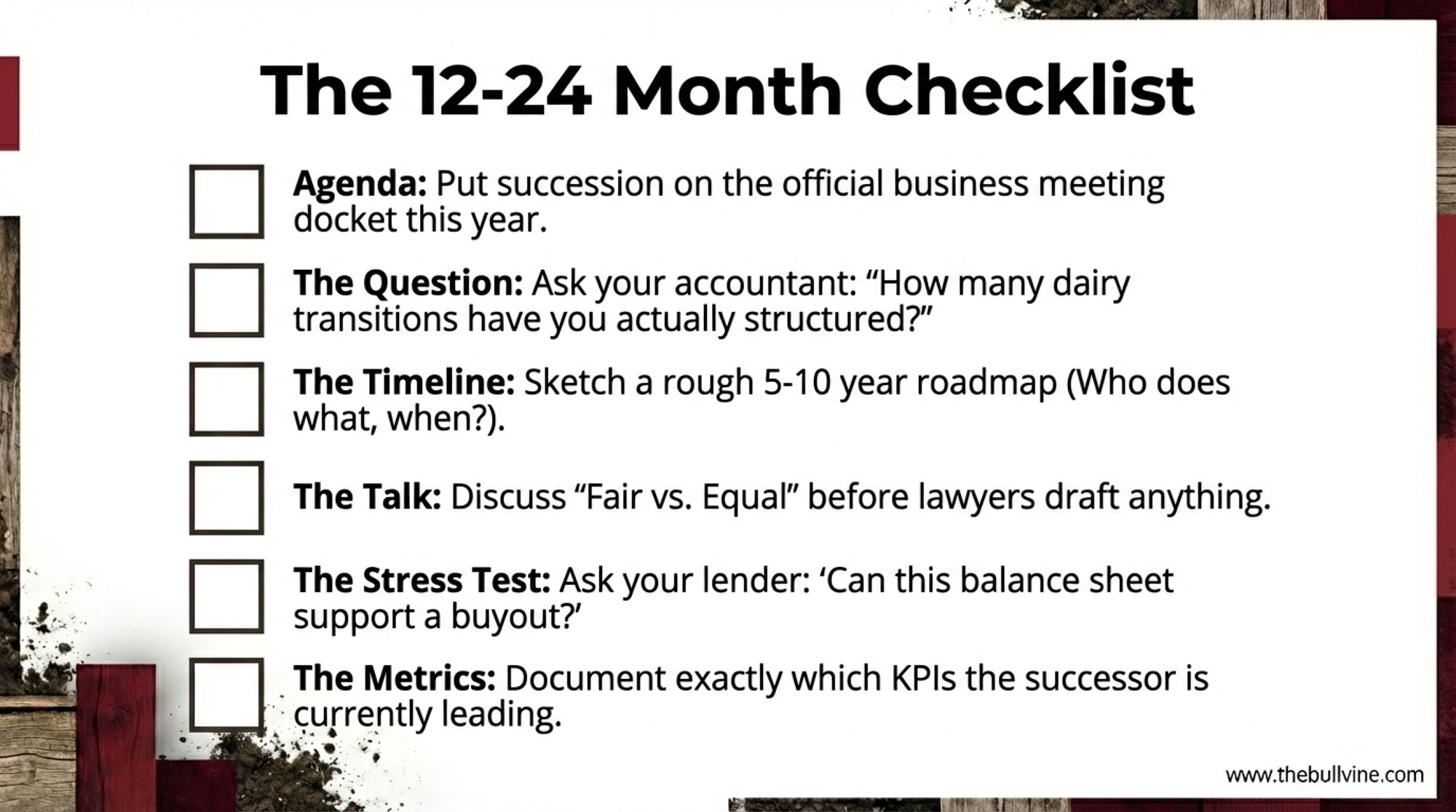

The 90-Day Triage: When You’re Already Behind

Timeline

Core Task

Key Deliverables

Red Flags to Address

Days 1–30

Asset inventory with real values

Land, cattle, equipment, quota, buildings valued at current market (not what you paid). Calculate debt-to-EBITDA ratio.

Debt-to-EBITDA above 4:1? Any succession plan that adds debt is dead.

Days 15–45