There is simply too much cheese. USDA’s Dairy Market News reports that cheese production schedules are “steady to stronger” and, for some cheesemakers, “limited warehouse space is becoming a concern.” Meanwhile, there is plenty of milk, especially now that bottlers are slowing down intakes for summer break.

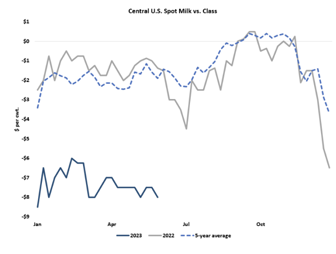

There is simply too much cheese. USDA’s Dairy Market News reports that cheese production schedules are “steady to stronger” and, for some cheesemakers, “limited warehouse space is becoming a concern.”  Meanwhile, there is plenty of milk, especially now that bottlers are slowing down intakes for summer break. Spot milk prices in the Upper Midwest ticked back down this week, with some sales as low as $12 under Class III. A few cheesemakers offered their workforce a long weekend, but others worked straight through the Memorial Day holiday. And, unlike earlier in the year, there are very few plants taking downtime for maintenance, so today’s steep discounts reflect a milk surplus that cannot be blamed on underutilized production capacity. By all accounts, the vats are full. USDA reports that some cheesemakers are turning away spot milk because they simply can’t hold anymore.

Meanwhile, there is plenty of milk, especially now that bottlers are slowing down intakes for summer break. Spot milk prices in the Upper Midwest ticked back down this week, with some sales as low as $12 under Class III. A few cheesemakers offered their workforce a long weekend, but others worked straight through the Memorial Day holiday. And, unlike earlier in the year, there are very few plants taking downtime for maintenance, so today’s steep discounts reflect a milk surplus that cannot be blamed on underutilized production capacity. By all accounts, the vats are full. USDA reports that some cheesemakers are turning away spot milk because they simply can’t hold anymore.

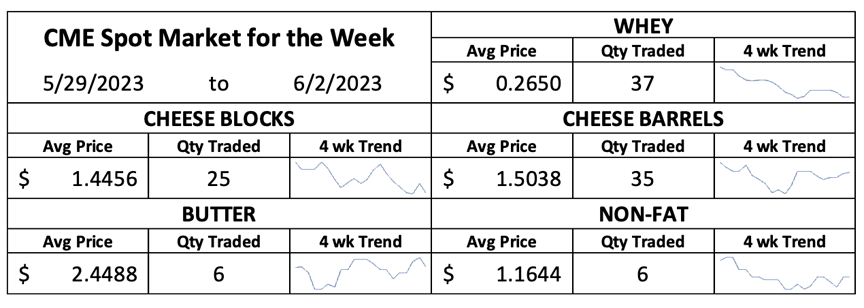

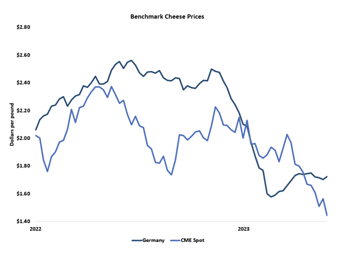

The excess weighed heavily on the cheese markets. CME spot Cheddar blocks plummeted to $1.42 per  pound on Wednesday, their lowest value since May 2020, at the height of the pandemic panic. Blocks made a partial recovery and closed today at $1.43, still down 4.75ȼ for the week. Barrels fared a little better. They closed today at $1.5125, up 2.25ȼ since last Friday. Those prices are probably low enough to attract a bit more export business, but demand is clearly not keeping pace with production.

pound on Wednesday, their lowest value since May 2020, at the height of the pandemic panic. Blocks made a partial recovery and closed today at $1.43, still down 4.75ȼ for the week. Barrels fared a little better. They closed today at $1.5125, up 2.25ȼ since last Friday. Those prices are probably low enough to attract a bit more export business, but demand is clearly not keeping pace with production.

More cheese means more whey, and most of it is being dried. Demand for higher protein whey concentrates is finally starting to perk up, which could shift more of the whey stream into concentrates down the road. But for now, dry whey output is heavy and so are stocks. CME spot whey prices slipped further this week, closing at 25.75ȼ, just a fraction of a cent above last week’s all-time low and down 1.75ȼ from last Friday.

Once again, the Class IV products held within their well-established trading ranges. CME spot nonfat dry milk (NDM) finished right where it started at $1.17. Spot butter regained half of the ground it lost last week, climbing 1.5ȼ to $2.445.

Once again, the Class IV products held within their well-established trading ranges. CME spot nonfat dry milk (NDM) finished right where it started at $1.17. Spot butter regained half of the ground it lost last week, climbing 1.5ȼ to $2.445.

Dairy Market News describes the NDM market as “balanced,” thanks to decent demand from Mexico. Still, driers are running hard to balance milk supplies in the back half of the spring flush. High temperatures have taken a toll on components, but nights are cool and milk yields are still only a little below the recent peak.

Churns are running, but butter output is expected to slow soon as the heat saps cream production and boosts ice cream sales. For now, though, butter production is going strong and manufacturers are putting away product for later this year.

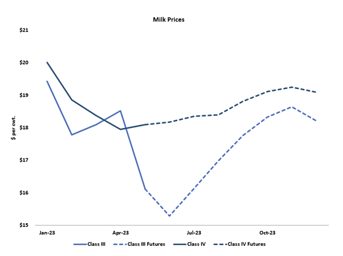

USDA announced the May milk price at a paltry $16.11 per cwt., down $2.41 from April and $9.10 lower than May 2022. At $18.10, May Class IV milk was 15ȼ higher than April but $6.89 lower than the astoundingly high price set last year. The futures promise steady or better prices ahead for Class IV. Unfortunately, Class III milk is projected to be even cheaper in the near term. Most Class III contracts lost about 50ȼ this week, and June Class III slumped to an untenable $15.29. July is a little better at $16.14, but that is still well below the cost of milk production. Deferred prices look a bit better, in the $17s and $18s, but that is still not enough to pay the bills on most operations. Class IV prices were characteristically stable this week, with modest gains in June and July and slight losses down the board. The futures project prices in the low $18s nearby, climbing above $19 in the fourth quarter.

USDA announced the May milk price at a paltry $16.11 per cwt., down $2.41 from April and $9.10 lower than May 2022. At $18.10, May Class IV milk was 15ȼ higher than April but $6.89 lower than the astoundingly high price set last year. The futures promise steady or better prices ahead for Class IV. Unfortunately, Class III milk is projected to be even cheaper in the near term. Most Class III contracts lost about 50ȼ this week, and June Class III slumped to an untenable $15.29. July is a little better at $16.14, but that is still well below the cost of milk production. Deferred prices look a bit better, in the $17s and $18s, but that is still not enough to pay the bills on most operations. Class IV prices were characteristically stable this week, with modest gains in June and July and slight losses down the board. The futures project prices in the low $18s nearby, climbing above $19 in the fourth quarter.

At these values, dairy producers are suffering painful financial losses, and the number of sellouts is on the rise. However, dairy slaughter volumes are not all that high, which suggests that, for now, most cattle are simply moving to a new home. With lofty beef prices and low milk prices, that’s likely to change very soon. But until it does, the dairy markets will remain under pressure.

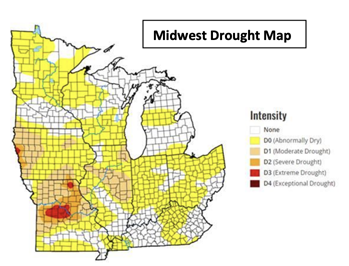

Heavy rains are helping to relieve the multi-year drought in the Southern Plains, but it’s hot and dry in the Corn Belt and the forecast calls for more of the same, with the hope of showers more than a week away. The U.S. Drought Monitor rates two-thirds of the Corn Belt as abnormally dry or worse, with 15% officially in drought. Young crops are starting to show signs of stress. Prolonged dryness will chip away at yield potential, although the impact is much less severe today than it would be in mid-summer when the crop pollinates. On the other hand, exports remain tepid. The opposing fundamentals pushed prices back and forth, but ultimately, concerns about the weather won out, and a strong Friday rally signaled that the bulls had the upper hand heading into the weekend. July corn closed at $6.09, up a nickel for the week. December corn climbed 6.75ȼ to $5.4125. July soybeans climbed another 15.25ȼ to $13.525. However, soybean meal prices dropped again. The July contract lost $5.40 and settled at $397.80 per ton.

Heavy rains are helping to relieve the multi-year drought in the Southern Plains, but it’s hot and dry in the Corn Belt and the forecast calls for more of the same, with the hope of showers more than a week away. The U.S. Drought Monitor rates two-thirds of the Corn Belt as abnormally dry or worse, with 15% officially in drought. Young crops are starting to show signs of stress. Prolonged dryness will chip away at yield potential, although the impact is much less severe today than it would be in mid-summer when the crop pollinates. On the other hand, exports remain tepid. The opposing fundamentals pushed prices back and forth, but ultimately, concerns about the weather won out, and a strong Friday rally signaled that the bulls had the upper hand heading into the weekend. July corn closed at $6.09, up a nickel for the week. December corn climbed 6.75ȼ to $5.4125. July soybeans climbed another 15.25ȼ to $13.525. However, soybean meal prices dropped again. The July contract lost $5.40 and settled at $397.80 per ton.

Original Report At: https://www.jacoby.com/market-report/too-much-cheese/