When butterfat improvements create processing problems, it’s time to rethink what “better” means

EXECUTIVE SUMMARY: What farmers are discovering across the country is that we’re not facing a typical market downturn—we’re navigating the collision of three fundamental industry shifts that require different thinking altogether. Processing plants built decades ago now struggle with today’s high-component milk, forcing producers to haul further while watching deductions climb. Meanwhile, the genetic improvements we’ve celebrated—butterfat up 12% over fifteen years according to genetic evaluation data—have created processing inefficiencies that ripple through the entire supply chain. Add China’s shift to selective importing and suddenly export markets that once promised growth look increasingly unpredictable. Yet here’s what gives me optimism: producers who recognize these aren’t temporary problems but new realities are finding profitable paths forward. Whether it’s negotiating directly with specialty processors, balancing component ratios for better premiums, or exploring beef-on-dairy programs that generate $875-1,100 extra per calf, the operations adapting thoughtfully to these changes are positioning themselves for long-term success in ways that benefit their bottom lines and their communities.

You know, looking at current milk prices and listening to producers at recent meetings, we’re clearly facing something different from typical market cycles. Whether you’re milking 100 cows in Vermont or managing 5,000 head in Arizona, we’re dealing with three major forces hitting simultaneously—processing capacity constraints, genetic evolution complications, and global trade shifts. And it’s their interaction that’s creating today’s uniquely challenging situation.

Processing Capacity: When Infrastructure Meets Its Limits

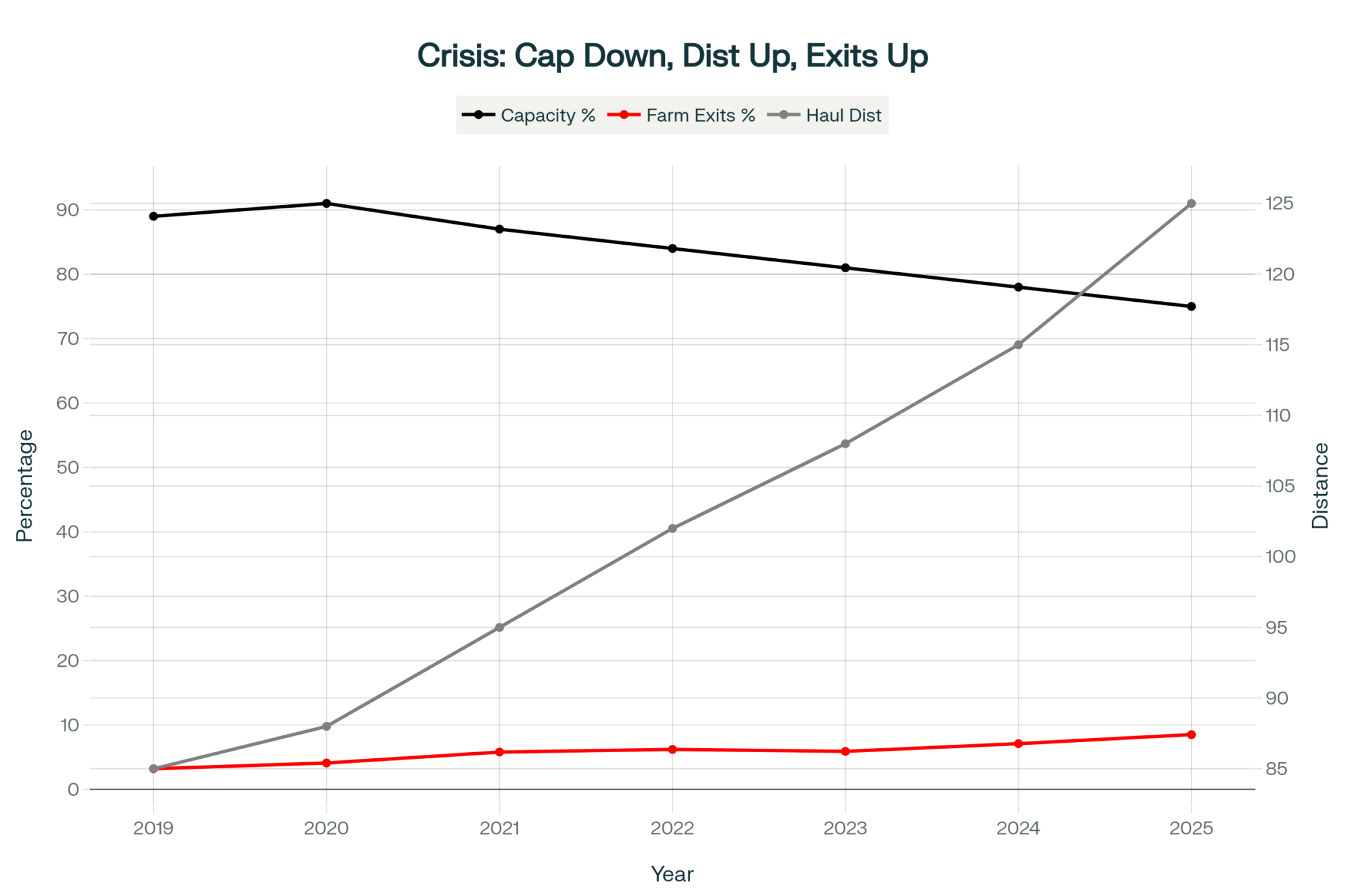

So let’s start with what many of us are experiencing firsthand. The USDA’s Dairy Market News has been documenting increasing transportation distances and rising hauling costs across most dairy regions, and we’re all seeing this directly in our milk checks—those hauling deductions just keep climbing, don’t they?

Progressive Dairy and Hoard’s Dairyman have both been covering these processing capacity constraints, particularly in traditional dairy regions. What’s interesting is that these plants were built decades ago for completely different times—different production levels and, honestly, milk with different characteristics altogether.

Here’s what really concerns me: every additional mile your milk travels is pure cost with zero added value. But there’s an even deeper issue…

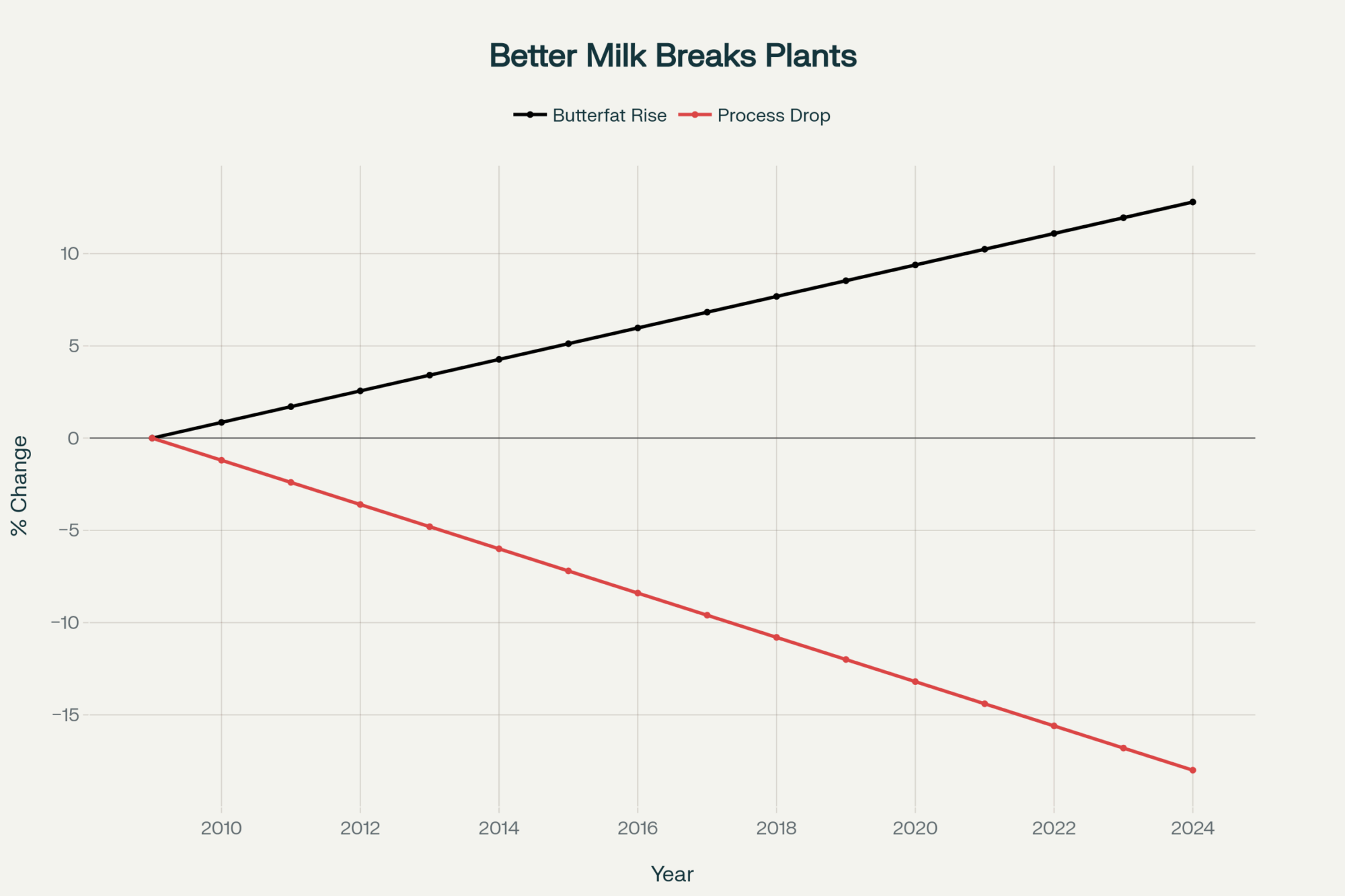

The milk we’re producing today has fundamentally different characteristics than what these plants were designed to handle. You probably know this already, but the Council on Dairy Cattle Breeding’s 2024 genetic evaluations indicate that butterfat levels have increased by approximately 12% over the past fifteen years. We’ve achieved exactly what we aimed for when premiums rewarded higher components.

But think about what this means practically. When butterfat levels increase significantly across millions of pounds of milk, that requires more cream volume to be separated. Different standardization requirements. Entirely different processing protocols. It’s like… well, it’s like we souped up the engine but forgot the transmission needs upgrading too.

Wisconsin’s Center for Dairy Profitability documented in their 2024 analysis that some operations are now negotiating directly with specialty processors who specifically want high-component milk—even if it means hauling further. These producers are often getting better prices despite the extra transportation costs, which tells you something about where the market’s heading.

I talked with a producer near Fond du Lac who made this shift last year. He’s hauling an extra 45 miles now, but getting 6% better pricing because his milk fits perfectly with what that specific cheese plant needs. Makes you think, doesn’t it?

What’s genuinely encouraging, though, is seeing adaptation in unexpected places. Southeast operations—particularly in North Carolina and Georgia, where they lack extensive legacy infrastructure—are building new processor relationships from scratch. And these facilities, designed for today’s milk characteristics, often capture opportunities that established regions miss because they’re locked into existing systems.

Even in the Pacific Northwest and Idaho, smaller processors are finding niches by specifically targeting high-component milk for specialty products. Innovation happens when necessity demands it, right?

The Genetics Evolution: When Success Becomes a Challenge

This really builds on the genetic progress we’ve made over recent decades. The data from genetic evaluation services shows we’ve achieved remarkable improvements in both butterfat and protein levels. And we should be proud of that achievement—it represents decades of careful breeding work.

Think about the logic here: producers did exactly what market signals told them to do. Federal Milk Marketing Order pricing has consistently rewarded butterfat at premium levels—often significantly higher than the premiums for protein. So naturally, breeding decisions followed the money. That’s not just smart business; it’s a rational response to clear economic incentives.

But now processors are telling a different story. Cornell’s PRO-DAIRY program published research in 2024 showing optimal component ratios for different dairy products, and many herds have shifted outside those ideal ranges. This creates processing inefficiencies that ripple through the entire system.

What I’ve found interesting is that several major cooperatives have been working with their members to address component balance—not abandoning improvement goals, but thinking strategically about what ratios work best for their specific processing capabilities. Some have even introduced premium schedules that reward balanced components rather than just high butterfat.

One Minnesota cooperative reported at their annual meeting that members who balanced components saw 7% better returns than those chasing maximum butterfat alone. Another cooperative in Ohio found similar results—their balanced-component producers averaged $0.85 more per hundredweight over the year.

The response varies dramatically by region, as you’d expect. Many Upper Midwest operations are adjusting their breeding strategies, while California and Southwest producers with different processor relationships may maintain their current approaches. And yes, beef-on-dairy has definitely become part of the equation. USDA Agricultural Marketing Service data from August 2025 showed beef-dairy crossbred calves averaging $875-1,100 premiums over straight Holstein bull calves at major auction markets.

Though opinions really do vary on this strategy—and understandably so. Some producers, especially those with robust genetic programs, are concerned about the long-term quality of replacements. Others see it as essential income diversification. I think both perspectives have merit depending on your specific situation. These patterns could shift with policy changes, but currently, it presents a real opportunity for many operations.

Global Trade: The Rules Keep Changing

Now, the international dimension adds complexity that affects all of us, whether we think about exports daily or not. The USDA Foreign Agricultural Service tracks global dairy trade patterns, and recent trends suggest we’re seeing fundamental shifts rather than temporary disruptions.

China’s dairy sector has undergone significant evolution. Their domestic production has grown significantly in recent years, and they’ve achieved substantial self-sufficiency in basic dairy products. What’s worth noting is that they’ve become selective importers, focusing on products they can’t efficiently produce domestically—such as whey proteins and specialized ingredients—rather than broad purchasing across all categories.

This represents strategic thinking about food security that makes sense from their perspective, even if it complicates our export planning. They’re essentially doing what we’d probably do in their position, aren’t they?

Mexico remains relatively stable thanks to USMCA provisions, maintaining its position as a major export market for U.S. dairy products. However, even there, European competitors are increasing pressure, and recent trade agreements could further shift the dynamics.

These patterns suggest—and this is concerning—that export markets, which once promised growth, are becoming increasingly unpredictable. So how do we build resilient operations in this environment?

The Human Dimension: Decisions That Go Beyond Spreadsheets

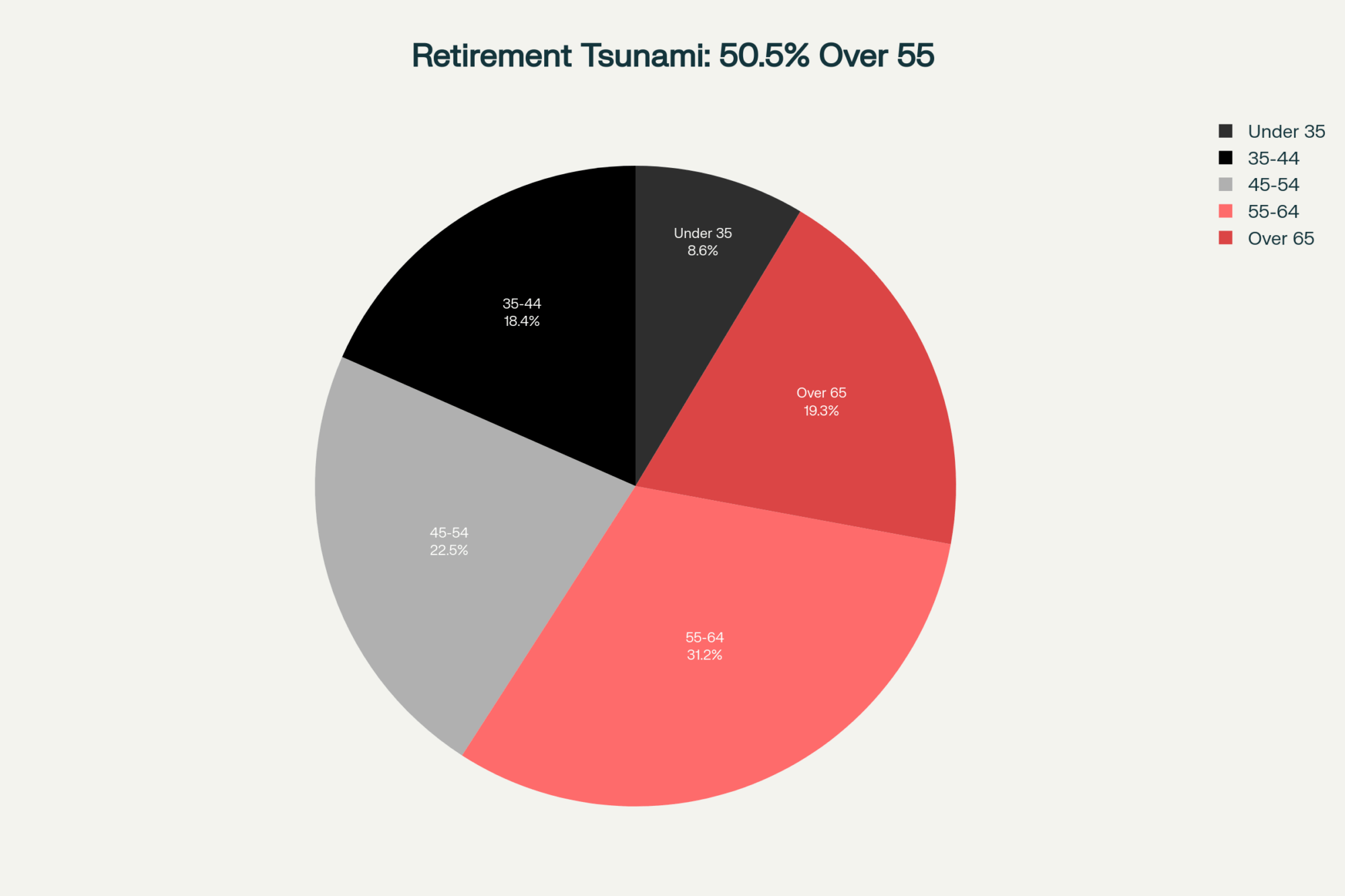

Here’s something that profoundly affects our industry yet rarely makes headlines. The USDA’s 2022 Census of Agriculture—our most recent comprehensive data—shows the average dairy farmer is now 57.5 years old. This creates decision-making challenges that transcend simple economic considerations.

Consider what many operations face right now: robotic milking systems typically cost $250,000-$ 400,000 per unit, according to equipment dealers. Parlor upgrades can go even higher, and facility improvements often pencil out over decade-plus horizons. These often make economic sense on paper. But when you’re 60 years old with kids established in careers off-farm… well, those calculations become deeply personal, right?

Extension programs across dairy states have been highlighting this challenge—it’s not just about return on investment anymore. It’s about aligning investments with life goals, family situations, and quality of life considerations. Neither aggressive investment nor maintaining the status quo is inherently right or wrong. Both reflect rational choices given individual circumstances.

What’s genuinely encouraging is seeing creative transition models emerging. Share milking arrangements are gaining traction in states like Wisconsin and New York. Long-term leases to younger farmers, gradual transitions to key employees—these aren’t traditional succession paths, but they’re creating real opportunities for the next generation.

A study from the University of Vermont Extension found that operations using these alternative transition models typically take 18-24 months to see full benefits from strategic adjustments, but report higher satisfaction rates for both exiting and entering parties.

Practical Pathways: What’s Actually Working

Given these challenges, what approaches show real promise? Well, it varies enormously, but patterns are definitely emerging from extension research and field observations.

Larger operations often benefit from comprehensive systems integration. University dairy programs consistently show that operations using integrated data management see meaningful improvements in feed efficiency—typically 15-25% gains with good implementation, according to a 2024 multi-state extension survey. It’s really about seeing breeding, feeding, health, and marketing as interconnected rather than separate enterprises.

Mid-size operations—let’s say 300 to 1,000 cows—frequently find success through selective modernization. Upgrading specific bottleneck areas while maintaining the functionality of existing systems. Cornell’s PRO-DAIRY program, as documented in their 2024 case studies, found that these targeted investments often deliver better returns than wholesale modernization attempts.

The Michigan State Extension reports that many operations are investing modestly in feed management improvements while starting to market a portion of their calves as beef crosses. A 600-cow farm near Lansing made these changes and saw 14% better margins without taking on overwhelming debt—and that’s smart adaptation if you ask me.

Smaller operations need different strategies entirely. Many thriving small farms are creating value through differentiation. The Vermont Agency of Agriculture’s 2024 report showed that 23% of dairy farms with fewer than 200 cows now engage in some form of direct marketing or value-added production. Whether it’s farmstead cheese, on-farm bottling, agritourism, or organic certification—these require different skills but can deliver margins 35-50% above those of commodity markets, according to their data.

Technology: Tool or Solution?

About technology adoption—and this is crucial—equipment alone doesn’t determine success. Integration into management systems does. Wisconsin’s Center for Dairy Profitability and other extension programs consistently find that farms with strong management systems before automation see meaningful productivity gains, while those hoping technology would fix existing problems see minimal improvement.

The key question isn’t “Should we adopt technology?” It’s “What specific problem needs solving, and what’s the most cost-effective solution?” Sometimes that’s expensive automation. Sometimes it’s modest investments in cow comfort or feed management that deliver similar gains. It all depends on your specific constraints and opportunities.

Looking Forward: Your Action Plan

So where does this leave us? The USDA Economic Research Service acknowledges significant uncertainty in their outlooks, but current projections suggest we’re in a fundamental transition, not a temporary disruption.

These three forces—processing constraints, genetic evolution, and shifts in global trade—will shape our industry for years to come. They’re realities to navigate, not problems that’ll magically resolve themselves.

However, what genuinely gives me optimism is that dairy farmers consistently demonstrate remarkable adaptability. Think about what we’ve navigated—the shift to Grade A standards, massive consolidations, environmental regulations, and technology revolutions. Each time, those who adapted thoughtfully found ways to thrive.

Success going forward will look different for different operations. A large dairy in Texas follows a completely different path than a grass-based farm in Missouri. And that diversity—that’s what strengthens our entire industry.

Begin by analyzing your operation in relation to these three forces. Where are you most vulnerable? What single change could provide the most impact? Whether it’s negotiating with a different processor, adjusting your breeding program, or exploring value-added opportunities—identify your highest-priority action and take that first step this week.

What matters most is an honest assessment of your situation, decisions aligned with your operation’s capabilities and goals, and willingness to adapt as conditions evolve. Whether that means expansion or right-sizing, new technology or perfecting current systems, global markets or local customers—multiple paths can succeed with the right strategy.

We’re part of something essential here—feeding people, maintaining rural communities, stewarding agricultural lands. The methods might evolve, the scale might shift, markets will definitely change, but that fundamental purpose… that endures.

As we navigate these challenges, remember that we’re stronger when we share experiences and learn from one another. Whether through cooperatives, extension programs, discussion groups, or just coffee with neighbors, staying connected helps us all make better decisions.

These are challenging times, no question. However, there are also times when thoughtful adaptation—not panic, nor stubbornness, but thoughtful adaptation—can position operations for long-term sustainability. The key is clear-eyed assessment, strategic planning, and supporting each other through this transition.

Because at the end of the day, that’s what dairy farmers do. We figure out how to keep moving forward, keep producing, keep feeding our communities. The specifics change, but that core mission… that’s what endures.

KEY TAKEAWAYS

- Processing partnerships pay off: Wisconsin producers negotiating directly with specialty cheese plants report 6-8% better pricing despite hauling 30-45 extra miles—the key is matching your milk’s component profile with specific processor needs rather than accepting commodity pricing

- Component balance beats maximum butterfat: Minnesota and Ohio cooperatives document that producers maintaining 0.80-0.85 protein-to-fat ratios earn $0.85-1.00 more per hundredweight than those chasing maximum butterfat alone, while processors actively seek this balanced milk

- Strategic beef-on-dairy delivers immediate returns: With crossbred calves commanding $875-1,100 premiums over Holstein bulls (USDA data, August 2025), using beef semen on 25-35% of your herd’s lower genetic merit cows generates $90,000-100,000 extra annually for a 1,000-cow operation

- Targeted modernization outperforms wholesale tech adoption: Extension research shows mid-size dairies (300-1,000 cows) achieve 15-25% feed efficiency gains by upgrading specific bottlenecks rather than complete system overhauls, with 18-24 month payback periods

- Alternative transitions create opportunities: Share milking, long-term leases, and gradual employee transitions offer viable paths forward for the 57% of dairy farmers approaching retirement without traditional succession plans, maintaining farm continuity while respecting personal goals

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

- From Breeding Chaos to Strategic Cash: How 2025’s Smartest Dairies Connect Every Decision – This article provides a tactical, how-to guide for integrating genomics with risk management. It reveals how producers are using three-tier breeding strategies to segment herds, generating extra cash from beef-on-dairy calves while maintaining long-term genetic progress.

- Trade War Reality Check: How North America’s $1.18 Billion Dairy Dependency Just Got Brutally Exposed – This strategic analysis shifts the focus from broad global markets to the specific, immediate threats of North American trade policy. It demonstrates how smart producers are building “anti-fragile” operations that gain strength from market disruption rather than relying on unstable export promises.

- Robotic Milking Revolution: Why Modern Dairy Farms Are Choosing Automation in 2025 – This piece offers a deep dive into technology adoption, busting common myths about robotic milking systems. It presents real-world data and case studies demonstrating how automation delivers a clear return on investment by reducing labor and improving herd health and productivity.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.