How this week’s supply tsunami exposed the industry’s biggest blind spot—and what you need to do about it

EXECUTIVE SUMMARY: Look, I just spent the weekend digging into July’s brutal market crash, and what I found will change how you think about your operation. The old “more milk, more money” playbook is officially dead – we’re now in an era where component optimization beats volume every single time. The numbers don’t lie: operations running 4.2% butterfat versus 3.8% are seeing $275-460 additional daily revenue on a 2,000-cow setup, and that gap’s only getting wider. Global markets just proved they’ll punish volume producers while rewarding those smart enough to focus on what their milk’s actually made of. With Class IV futures sitting at $19.05/cwt and Class III stuck at $18.50/cwt, the market’s screaming at you to optimize for fat and hedge against protein weakness. The producers who get this shift right now – not next year, not next month, but right now – will be the ones still standing when the dust settles.

KEY TAKEAWAYS

- Genetic selection pivot pays immediately: Daughters of fat-plus sires are generating $150-200 more annually per cow under current pricing structures. Start evaluating your breeding program for butterfat percentage over volume metrics – your 2026 calf crop depends on decisions you make this month.

- Component monitoring = instant profit capture: Real-time parlor monitoring lets you adjust feeding strategies daily, capturing an additional $0.20-0.30 per hundredweight just from ration timing. Pennsylvania farms already doing this are seeing results within 30-60 days, not years.

- Risk management isn’t optional anymore: Lock in 25-30% of your fat-heavy production through Class IV futures while buying Class III downside protection through DRP programs. With that $0.55 spread, not hedging is basically gambling with your operation’s future.

- Feed cost optimization creates double wins: Strategic fat supplementation and improved forage quality boost component returns by $0.15-0.25 per hundredweight with minimal input cost increases. Vermont producers using palmitic acid inclusion are seeing 0.15 percentage point butterfat gains in 4-6 weeks.

Look, I’ve been watching dairy markets for more than three decades, and what happened at the Global Dairy Trade auction this week… well, it’s one of those moments that fundamentally changes how we think about milk pricing. We just witnessed a brutal -4.1% crash in the GDT Price Index—the worst single-day performance in twelve months—and if you think this is just another cyclical blip, you’re missing the fundamental shift that’s happening right under our noses.

The thing about supply-driven corrections is they don’t send you a courtesy call first. When Fonterra reported their highest milk collections in five years, with May intake surging 7.5% year-over-year, and Irish collections jumped 6.5% for the month, the writing was on the wall. You simply can’t flood global markets with that much milk and expect prices to hold. Basic economics, right? But somehow our industry keeps forgetting this fundamental lesson.

This wasn’t just a bad day at the auction house either. The event ran for nearly three hours across 22 bidding rounds, with 161 participants and only 110 walking away as winners. When you see numbers like that, you know sellers were desperate to move product, and desperate sellers make for ugly prices.

But here’s what really gets me fired up about this whole situation… we’re not just dealing with lower prices. We’re looking at a fundamental restructuring of how milk components get valued, and it’s happening whether we like it or not.

The Component Split That’s Reshaping Everything

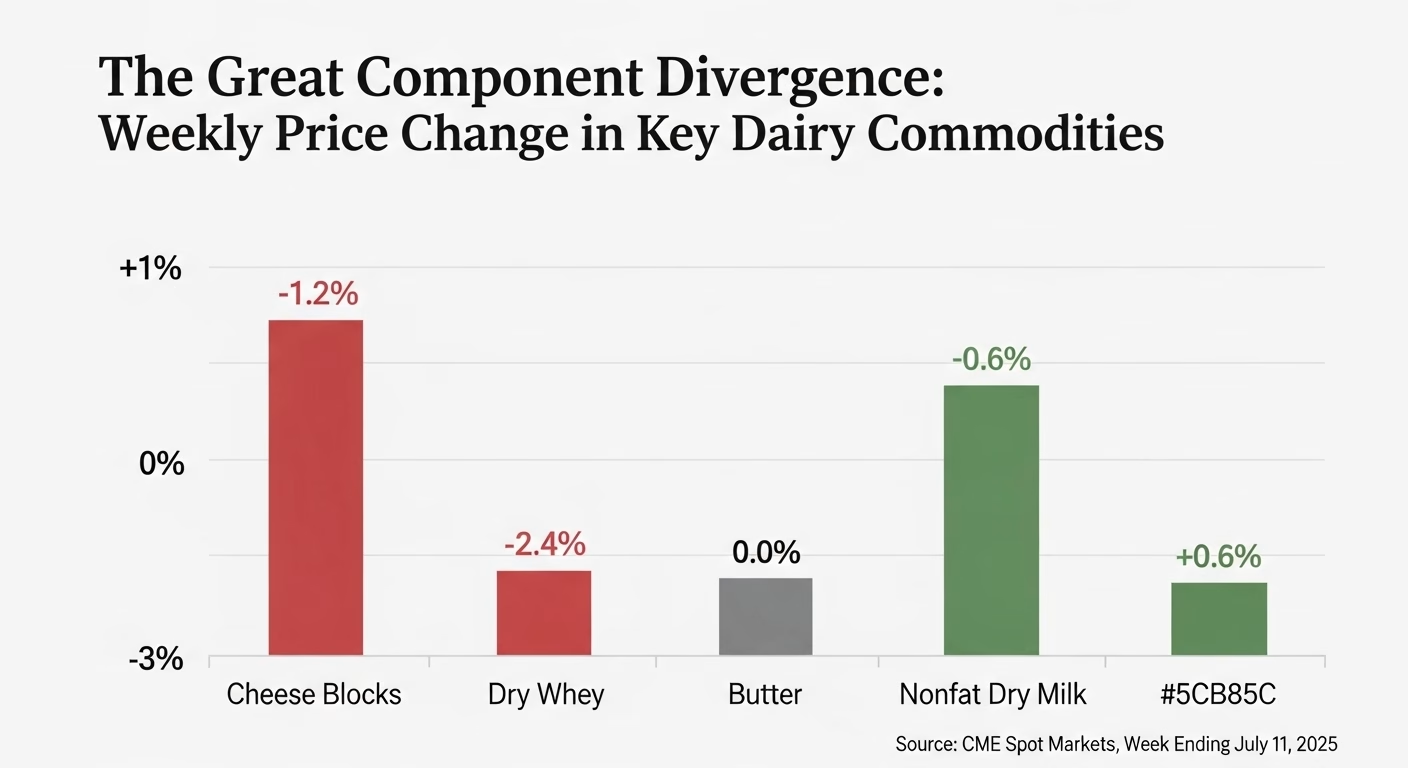

Something really caught my attention about this market break—how it’s revealing the industry’s biggest blind spot. The CME spot markets told the whole story this week. Cheese blocks dropped to $1.66/lb, dry whey collapsed to $0.5675/lb—that’s a 1.41 cent weekly decline that had whey traders wincing. But here’s the kicker: butter held steady at $2.59/lb and nonfat dry milk actually gained ground to $1.2675/lb.

That’s not random market noise, folks. That’s the market screaming at you about what it values right now.

What strikes me about this divergence is how it’s playing out differently depending on where you’re milking cows. According to recent work from the USDA’s July WASDE report, the 2025 all-milk price forecast got bumped up to $22.00 per hundredweight. That’s not pocket change; that’s the kind of revision that changes your whole year’s profitability outlook.

But here’s where it gets really interesting: Class IV futures are now trading at $19.05/cwt while Class III settled at $18.50/cwt. That’s a $0.55 spread that translates directly to your bottom line depending on your butterfat numbers.

Recent research from dairy economists at Cornell University suggests that operations with milk testing 4.2% butterfat versus 3.8% could see $0.30-0.50 per hundredweight advantages under current pricing structures. If you’re running Holstein genetics selected for high butterfat… well, you’re sitting pretty right now. But if your operation skews toward protein production? You’re feeling the squeeze, and honestly, it’s only going to get worse.

Why aren’t more producers talking about this shift? It’s like watching a slow-motion train wreck, and half the industry is still focused on the wrong track.

Regional Realities: When Geography Becomes Destiny

The fascinating thing—and a bit scary—is how global dairy markets aren’t really global anymore. They’re becoming increasingly regionalized, and that’s creating some wild opportunities for those who understand the game.

North America: The Unexpected Winner

U.S. producers are experiencing something I haven’t seen in years: genuine decoupling from global weakness. While New Zealand’s NZX futures show butter dropping from $7,660/MT in July to $6,740/MT by September—that’s a $920 drop in just two months—American producers are looking at improved margins.

The feed cost dynamics are actually working in our favor, too. According to extension specialists at the University of Wisconsin-Madison, the improved soybean meal price forecasts could translate to $25-35 less in monthly feed costs per cow for typical 500-head operations. When you’re feeding 4-6 pounds of protein supplement daily, those savings add up fast.

I was just talking to a producer in Wisconsin last week who’s already adjusting his ration strategy based on these projections. He’s calculating that with improved milk prices and cheaper protein supplements, he’s looking at roughly $40-50 per cow improvement in monthly margins. That’s the kind of swing that changes your whole year’s outlook.

But here’s what’s got me curious… how many operations are actually positioned to capture this opportunity versus getting caught flat-footed by the component shift?

Europe: Caught Between Two Worlds

European markets are fascinating right now because they’re being pulled in opposite directions. EU butter prices edged up 0.2% to €740/100kg while skim milk powder fell 1.8% to €239/100kg. That’s not market manipulation—that’s processors making strategic decisions about where to allocate their limited milk supplies.

The EU is dealing with supply constraints that are actually protective. Environmental regulations, bluetongue outbreaks (this is becoming more common across Germany and France), and demographic challenges are creating a natural supply ceiling. Sometimes regulations work in your favor… who knew?

Recent research from dairy production specialists at Wageningen University shows that EU milk output forecasts suggest minimal production growth of just 0.2% to 0.4% for all of 2025. When you’ve got that kind of constraint, every liter of milk becomes precious.

But here’s what’s interesting—the UK stands out as a major outlier. UK milk production jumped 5.7% year-over-year in May, hitting record daily volumes. While that sounds great for UK producers, it actually puts them in a tough spot. They’re producing into a weak global market without the EU’s internal supply constraints to protect them.

Oceania: Ground Zero for Pain

If you’re milking cows in New Zealand right now, you’re at the epicenter of this supply storm. The GDT results show just how brutal this correction has been: whole milk powder dropped 5.1% to $3,859/MT, butter fell 4.3% to $7,522/MT, and the forward curve suggests this pain isn’t over.

What’s really concerning is the future structure. When you see butter futures in steep backwardation—dropping over $900/MT in just two months—that’s the market pricing in sustained weakness. This isn’t a temporary blip; this is a fundamental reset that could last through the Southern Hemisphere’s peak production season.

The Genetics and Nutrition Reality Check

This component value divergence we’re seeing isn’t just a market quirk—it’s becoming a structural feature of how milk gets valued. What’s particularly noteworthy is how this is playing out for different genetic programs.

I know a producer in Vermont who’s been working with dairy geneticists at the University of Vermont Extension to optimize his breeding program for butterfat. They’ve moved away from pure volume genetics toward proven fat-plus sires, and he’s seeing results. Under current pricing, daughters of these bulls are generating about $150-200 more annually per cow than his volume-focused animals.

But genetics is only part of the equation. Feed efficiency experts from Penn State’s dairy science program are calculating that strategic fat supplementation and forage quality improvements can boost component returns by $0.15-0.25 per hundredweight with minimal additional input costs. That’s the kind of ROI that makes sense even in tight margin environments.

For a 2,000-cow operation producing 75 pounds per cow daily, optimizing from 3.8% to 4.2% butterfat translates to $275-460 additional daily revenue. Scale that across a year, and you’re talking about $100,000-168,000 in additional income just from component optimization. That’s not theoretical—that’s real money hitting your milk check every month.

| Herd Size | Daily Production | Butterfat Increase | Approx. cwt Advantage* | Potential Additional Annual Revenue |

| 500 Cows | 75 lbs/cow | 3.8% to 4.2% | $0.40/cwt | $54,750 |

| 1000 Cows | 75 lbs/cow | 3.8% to 4.2% | $0.40/cwt | $109,500 |

| 2000 Cows | 75 lbs/cow | 3.8% to 4.2% | $0.40/cwt | $219,000 |

*Based on a $0.40/cwt premium for a 0.4 percentage point increase in butterfat.

The question is… how quickly can you implement these changes, and what’s the realistic timeline for seeing results? From what I’m seeing on progressive farms, genetic improvements take 2-3 years to materialize fully, but nutritional adjustments can show results within 30-60 days.

Risk Management: Why Passive Strategies Are Dead

The current market environment is offering some of the clearest hedging signals I’ve seen in years. With Class IV futures trading at a significant premium to Class III, the market is practically screaming at you to hedge fat-based production while protecting against protein-based downside.

Here’s what I’m telling progressive operations: lock in 25-30% of your expected fat-heavy production through forward contracts while buying Class III downside protection through puts or the Dairy Revenue Protection program. The math is compelling—you’re capturing the current spread while limiting your exposure to further protein market weakness.

What’s fascinating is how this plays out differently across regions. European futures markets on the EEX are pricing similar opportunities, with July SMP contracts at €2,396/MT and butter at €7,371/MT—a spread that’s too wide to ignore for producers who understand component risk management.

The implementation timeline here is critical. Most DRP enrollment deadlines are 30-45 days before the coverage period starts, so if you’re thinking about protecting your fall production, you need to move now. Futures markets offer more flexibility, but you need the financial infrastructure in place—margin accounts, credit lines, the works.

The Technology Factor Nobody’s Talking About

Something else is happening that’s becoming increasingly clear: the producers who thrive in this environment aren’t just those with the best genetics or the cheapest feed—they’re the ones with the best data.

Component management has moved from optimization to necessity. Real-time monitoring technology isn’t a luxury anymore; it’s essential for capturing the value spreads we’re seeing. The operations that can adjust their nutritional programs based on daily component pricing are the ones that’ll come out ahead.

I was just at a farm in Pennsylvania where they’ve installed real-time component monitoring through their parlor system. The producer told me he’s adjusting his feeding strategy almost daily based on component premiums. It’s allowed him to capture an additional $0.20-0.30 per hundredweight just by optimizing his ration timing.

But here’s the thing—this technology isn’t cheap, and it requires a learning curve. The farms I’m seeing succeed with this approach are investing 12-18 months in training and system optimization before they see consistent results. Are you prepared for that commitment?

What the Next Few Weeks Will Tell Us

The upcoming July 15th GDT auction will serve as a crucial test of whether this correction has found a floor. Honestly? I’m not optimistic. Fonterra’s already announced significant volumes for the event, and if those hit the market and prices fall further, it’ll confirm that this bearish trend has legs.

But here’s the thing—the auction results are almost beside the point now. We’re operating in a fundamentally different market structure. Volume-focused strategies aren’t just outdated; they’re counterproductive in this environment.

Current trends suggest that Chinese import demand—which could provide the lifeline Oceanic markets desperately need—remains sluggish. According to agricultural trade economists at Iowa State University, without that demand recovery, New Zealand producers are looking at an extended period of painful price discovery.

The summer heat across the Northern Hemisphere is also playing a role. I’ve been getting reports from producers in Wisconsin and New York about heat stress impacting fresh cow performance. When you combine that with the seasonal decline in milk production, it could provide some support to powder markets… but probably not enough to offset the Oceanic supply tsunami.

The Bottom Line: Three Critical Takeaways

After watching this market chaos unfold, three things are crystal clear to me:

First, component management isn’t optional anymore. The fat-protein spread has become the defining feature of 2025 markets. Operations that can’t optimize for butterfat production will get left behind. Period. If you’re not tracking your component tests daily and adjusting your nutrition program accordingly, you’re missing the biggest profit lever in your operation.

This isn’t just about genetics anymore—it’s about real-time management. The producers who understand this are already implementing feeding strategies that can shift butterfat test by 0.1-0.2 percentage points within 4-6 weeks. Under current pricing, that’s $200-400 additional monthly revenue per cow.

Second, regional market dynamics are creating unprecedented opportunities. U.S. producers benefit from strong domestic fundamentals and that bullish USDA outlook. European producers have supply constraints working in their favor, creating natural price support. Oceanic producers… well, they’re learning about oversupply the hard way.

But here’s what’s particularly striking—even within regions, the opportunities vary dramatically. A producer in Vermont with high-fat genetics is in a completely different position than one in Texas focused on volume. Geography matters, but genetics and component management matter more.

Third, sophisticated risk management has moved from advanced strategy to basic survival. The market is offering clear signals about component value divergence, and passive strategies carry exceptional risk. With Class IV futures trading at such a premium to Class III, not hedging is essentially gambling with your operation’s future.

The tools are there—DRP programs, futures markets, forward contracts. The question is whether you’re using them strategically to capture the fat premium while protecting against protein downside. According to risk management specialists at Cornell, operations that implement component-based hedging strategies are seeing 15-20% lower margin volatility.

Here’s what I’m watching for the rest of Q3 2025: the July 15 GDT auction will either confirm this bearish trend or signal a potential floor. Chinese import data for June and July could be a game-changer if demand recovers. And honestly? Northern Hemisphere heat stress could provide some unexpected price support if production drops more than expected.

The question isn’t whether dairy markets will recover—they always do. The question is whether you’ll be positioned to capture the opportunities when they emerge. This market correction has separated the producers who understand the new realities from those still playing by the old rules.

And honestly? That separation is only going to become more pronounced as we move through the rest of 2025. The producers who embrace component optimization, understand regional dynamics, and implement sophisticated risk management will be writing the next chapter of this industry’s story.

The rest will just be reading about it in the market reports.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

- Spring Pasture Powerplay: Balancing Grazing Efficiency with Milk Component Goals – Reveals practical strategies for optimizing butterfat and protein production through strategic grazing management, including specific rotation schedules and supplementation protocols that can boost components by 0.2% within weeks of implementation.

- Maximizing Milk Solids Output Through Strategic Nutrition and Genetics – Demonstrates how to capture the fat-protein premium through targeted feeding strategies and genetic selection, providing specific DMI targets and supplementation protocols that deliver measurable component improvements and higher milk checks.

- 5 Technologies That Will Make or Break Your Dairy Farm in 2025 – Explores cutting-edge monitoring and automation technologies that enable real-time component optimization, featuring case studies of farms achieving 20% yield increases and 40% mortality reductions through smart implementation of precision dairy tools.

Join the Revolution!

Join the Revolution!

Join the Revolution!

Join the Revolution!Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.