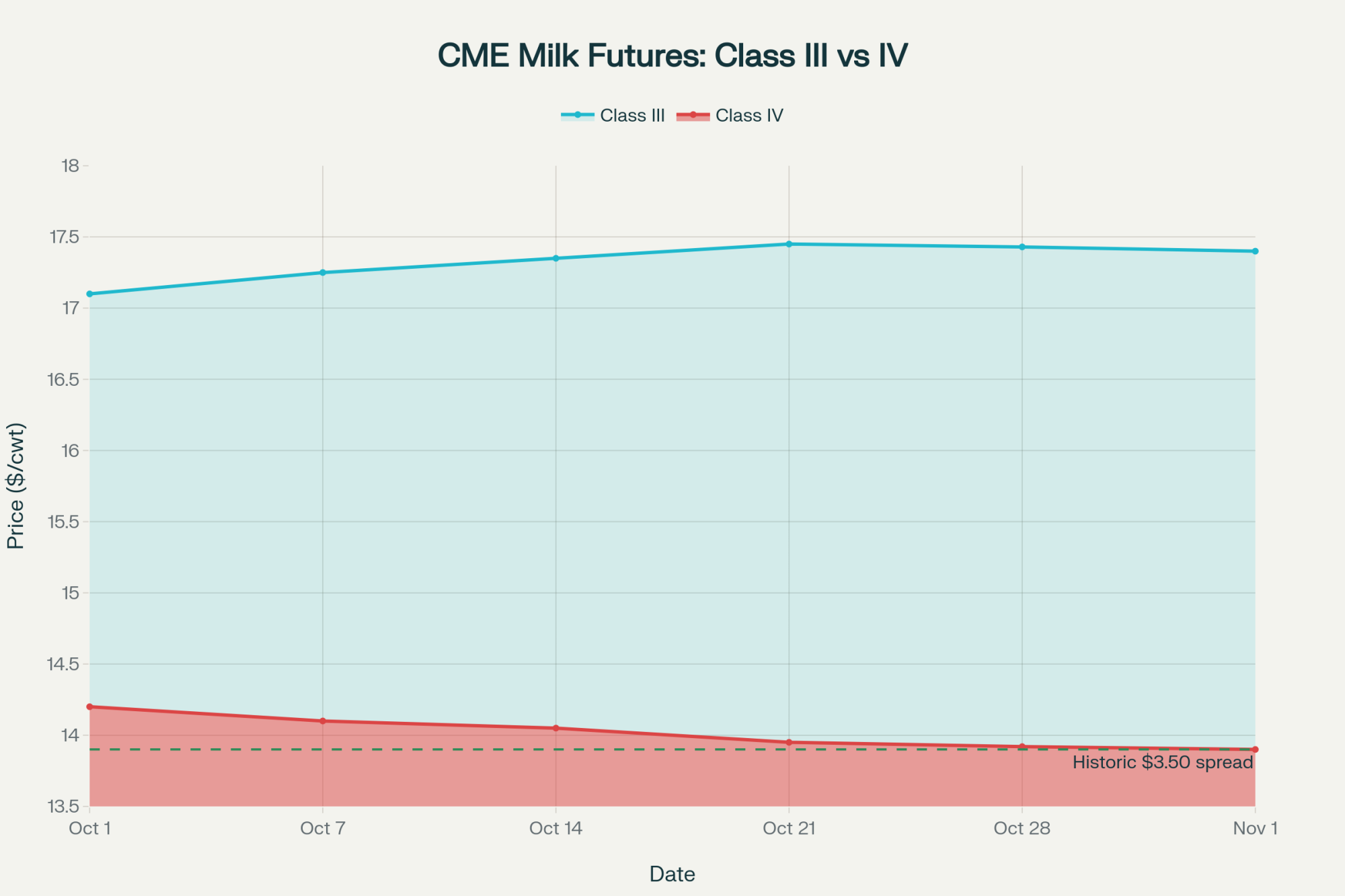

European cheese crashed 37% year-over-year, and the Class III-IV spread reached a farm-killing $3.50/cwt.

Executive Summary: Global dairy markets are in freefall. European cheese crashed 37% year-over-year, GDT auctions fell for the fifth straight week, and the Class III-IV spread exploded to a farm-killing $3.50/cwt—your Class III neighbor is now making $3,800 more per month than you. Milk production is surging everywhere (New Zealand +2.8%, UK +7.5%, U.S. herd at 32-year high) while demand craters, with only whey (+2.2%) and China’s premium dairy pivot offering hope. The Trump-Xi deal promises 25 million tonnes of annual soybean purchases to ease feed costs, but it won’t save commodity producers. Bottom line: If you’re shipping Class IV at $13.90 while others get $17.40 for Class III, you’re losing $45,000 annually. The farms that survive will be those that act now to lock in Class III, optimize components, and abandon the volume-at-any-cost mentality that’s driving this market into the ground.

Global dairy markets delivered another week of painful reality checks. European cheese posted annual declines of more than 30%. The fifth straight GDT auction decline confirmed what you already know—there’s too much milk chasing too few buyers. Meanwhile, the Class III-IV spread hit $3.50/cwt, meaning your neighbor shipping Class III milk is making $3,800 more per month than you are if you’re stuck in Class IV.

European Futures: Butter Holds, Everything Else Slides

Key Takeaway: European traders moved 2,620 tonnes last week, but the real story is powder weakness (-1.3%) while whey bucked the trend (+2.2%)—a clear signal that protein derivatives are the only bright spot.

EEX recorded 524 lots of trading activity, with Tuesday’s 925-tonne session marking the week’s peak. The breakdown tells you everything about market sentiment:

- Butter futures only dropped 2.0% to €5,093/tonne

- SMP futures weakened 1.3% to €2,161/tonne

- Whey futures climbed 2.2% to €1,007/tonne

That whey strength? It’s your lifeline. Strong protein derivative demand for feed and nutrition applications is keeping values supported while everything else crumbles.

Singapore Exchange: New Zealand’s Spring Flush Hits Hard

Key Takeaway: SGX traders moved 17,020 tonnes, but WMP prices fell for the fifth straight week to $3,523/tonne—Fonterra’s 2.8% production increase is flooding the market.

The numbers paint a clear oversupply picture:

- WMP: Down 0.7% to $3,523/tonne

- SMP: Flat at $2,591/tonne

- AMF: Up 0.2% to $6,677/tonne

- Butter: Down 1.3% to $6,339/tonne

Here’s what matters for your operation: Fonterra’s September collections hit 179 million kgMS (+2.8% YoY), with season-to-date volumes running 3.0% ahead. When New Zealand pumps out milk like this, global prices have nowhere to go but down.

European Cheese Collapse: The 30% Massacre

Key Takeaway: European cheese prices aren’t just weak—they’re in historic freefall. Every major variety is down 30%+ year-over-year, and buyers know more pain is coming.* The weekly damage was brutal:

- Cheddar Curd: Crashed €113 to €3,388 (-33.6% YoY)

- Mild Cheddar: Plunged €206 to €3,430 (-33.3% YoY)

- Young Gouda: Trading at €2,909 (-37.2% YoY)

- Mozzarella: Down €105 to €2,823 (-36.2% YoY)

Why should you care? Because European processors are bleeding cash—paying €520/tonne for milk while selling Gouda at €400/tonne. That math doesn’t work. Something’s got to give.

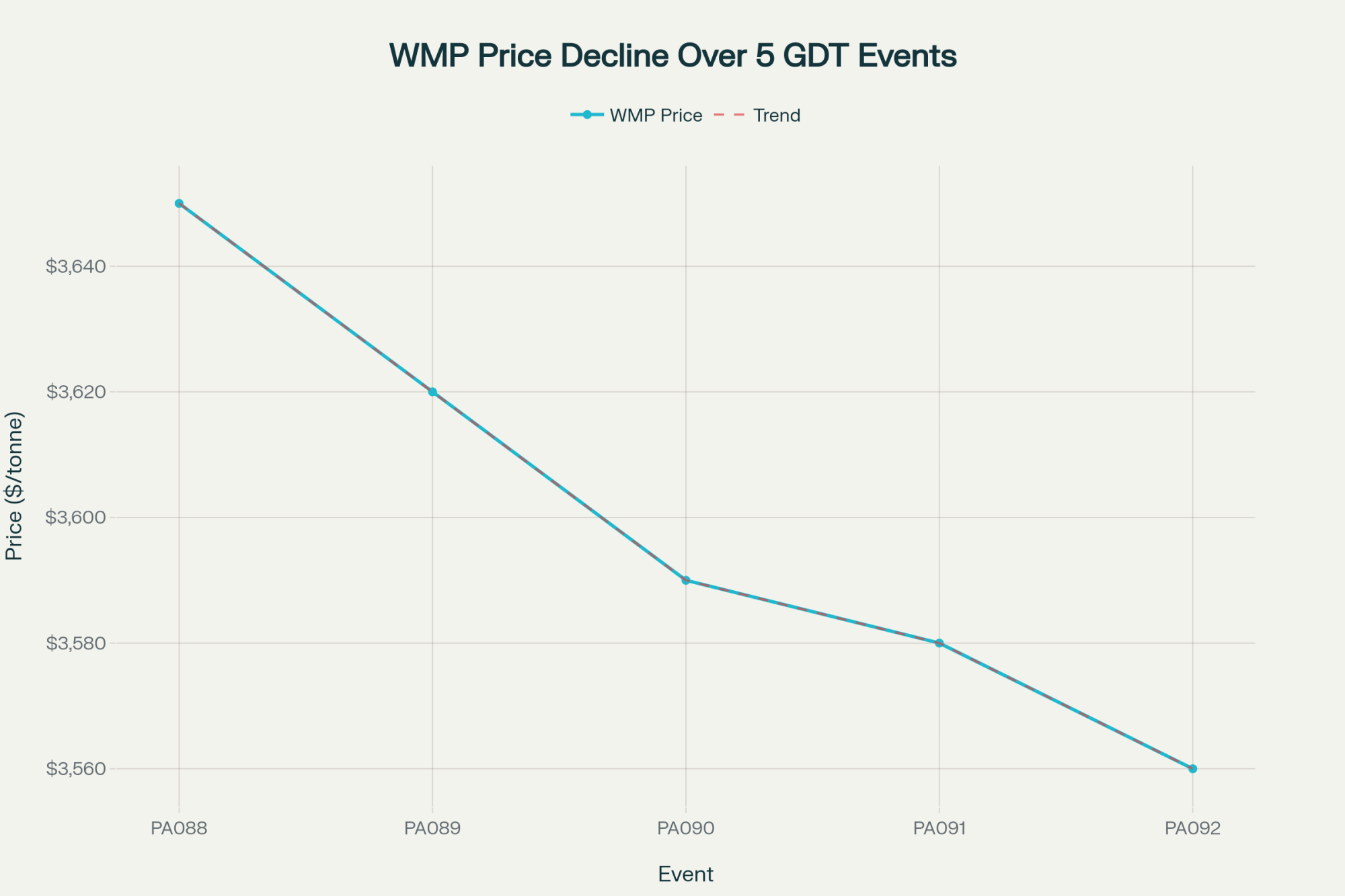

GDT Auction: Fifth Straight Decline Says It All

Key Takeaway: *The GDT Pulse auction delivered another gut punch—WMP at $3,560 and SMP at $2,530 represent 13-month lows. Buyers have zero urgency. The PA092 results confirmed what everyone fears:

- WMP: $3,560/tonne (down $90 from two weeks ago)

- SMP: $2,530/tonne (down $55 from prior pulse)

- Total volume: Only 2,612 tonnes with 41 bidders

That’s five consecutive declines. The message? Global buyers are sitting on their hands, waiting for even lower prices.

Global Production: Everyone’s Making More Milk

Key Takeaway: From New Zealand (+2.8%) to Poland (+5.7%) to the UK (+7.5%), milk is flowing everywhere except where you need it—into buyer demand.

Southern Hemisphere Springs Forward

- New Zealand: 316.3 million kgMS season-to-date (+3.0%)

- Australia (Fonterra): 23.4 million kgMS YTD (+3.0%)

- Argentina: September production surged 9.9% YoY

Northern Hemisphere Piles On

- UK: September hit 1.28 million tonnes (+7.5% YoY)

- Poland: 1.11 million tonnes in September (+5.7% YoY)

- Ireland: November 2024 exploded 34% higher

- USA: Herd at 9.52 million cows—highest since 1993

CME Markets: The Class Spread That’s Killing Farms

Key Takeaway: The $3.50/cwt Class III-IV spread isn’t just a number—it’s the difference between profit and loss for thousands of dairy farms.*Here’s your Friday closing reality check:

Winners:

- Cheddar Barrels: $1.8050 (+3.5¢)

- Dry Whey: $0.7100 (+2¢)—nine-month high

- Class III November: $17.40/cwt

Losers:

- NDM: $1.1325 (-2.75¢)

- Butter: $1.6100 (barely holding)

- Class IV November: $13.90/cwt

Do the math: If you’re shipping 3 million pounds monthly, that $3.50 spread means $3,800 less in your milk check compared to your Class III neighbor. That’s a new pickup truck disappearing every year.

Feed Markets: China Deal Sparks Soybean Rally

Key Takeaway: Soybeans hit $11/bushel on China’s promise to buy 12 million tonnes immediately plus 25 million tonnes annually—but will they follow through?

The Trump-Xi meeting delivered feed market fireworks:

- Soybeans: Surged 60¢ to $11.00/bushel (15-month high)

- Soybean Meal: Jumped $27 to $321.40/ton

- Corn: Up 8¢ to $4.31/bushel

Treasury Secretary Bessent’s announcement sounds impressive, but here’s the reality: Those Chinese purchase commitments are still below pre-trade war levels. Don’t count your feed savings yet.

Trade Breakthroughs: Southeast Asia Opens Doors

Key Takeaway: New agreements with Malaysia, Cambodia, Thailand, and Vietnam eliminate dairy tariffs—finally giving U.S. exports a fighting chance against New Zealand and Australia.

President Trump’s Asian tour delivered real results:

- Malaysia: Eliminates all dairy tariffs, recognizes U.S. standards

- Cambodia: Zero tariffs on all U.S. dairy products

- Thailand: Framework covers 99% of goods (dairy included)

- Vietnam: Preferential access for substantially all dairy

Why this matters: Vietnam imported $668 million in dairy through August 2025, but U.S. suppliers captured only $22 million due to tariff disadvantages. These deals level the playing field.

China’s Premium Pivot: The $150,000 Opportunity

Key Takeaway: China’s 18% surge in premium dairy imports versus 12% declines in commodity products isn’t a blip—it’s a structural shift that rewards quality over quantity.

The numbers tell the story:

- Cheese imports: +13.5% YoY

- Butter imports: +72.6% YoY

- Skim milk powder: Significant retreat

For a 500-cow operation optimized for components and premium channels, this shift could mean $150,000+ in additional annual revenue. The question is: Are you positioned to capture it?

The Bottom Line: Survival Mode Until Spring

Here’s your reality: Global milk production is overwhelming demand, and it’s not stopping. The Class III-IV spread is creating massive inequities between farms. European cheese markets are in freefall with no floor in sight. Your only bright spots? Whey strength and potential Chinese premium demand.

Three moves to make this week:

- Lock in Class III if you can—that $3.50 spread won’t last forever

- Review your component optimization—premium markets are your escape route

- Don’t forward contract cheese—European prices prove there’s more pain coming

The market’s sending clear signals: Commodity dairy is dead money. Premium products and value-added channels are your survival strategy. The farms that adapt to this reality will still be here in 2027. The ones that don’t? They’ll be someone else’s expansion.

What’s your move? The clock’s ticking, and every month at $13.90, Class IV is another month closer to the edge.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

- Maximizing Milk Components: A Producer’s Guide to Boosting Fat and Protein – This guide provides actionable strategies for nutrition, herd management, and breeding that directly increase component percentages, helping you capture the higher Class III values and escape the commodity trap highlighted in this week’s market collapse.

- Navigating the New Dairy Economy: Why Volume is No Longer King – This strategic analysis unpacks the economic forces driving the shift from volume to value. It provides a framework for rethinking your business model to align with premium market demand and ensure long-term profitability in a volatile global market.

- The Genetic Key: Unlocking Higher Components Through Genomic Selection – Explore how to leverage modern genomics as a long-term solution to the market’s demands. This article demonstrates how to build a more resilient and profitable herd by selecting for genetics that naturally deliver higher-value milk components.

Join the Revolution!

Join the Revolution!

Join the Revolution!

Join the Revolution!Join over 30,000 successful dairy professionals who rely on Bullvine Weekly for their competitive edge. Delivered directly to your inbox each week, our exclusive industry insights help you make smarter decisions while saving precious hours every week. Never miss critical updates on milk production trends, breakthrough technologies, and profit-boosting strategies that top producers are already implementing. Subscribe now to transform your dairy operation’s efficiency and profitability—your future success is just one click away.