The T.C. Jacoby Weekly Market Report Week Ending October 27, 2023

SMP fell hard at the GDT Pulse event on Tuesday. It’s too soon to know whether the Pulse auction represents a good indication of global SMP values or if it can be dismissed due to limited participation in such a nascent event. But it certainly sparked fears about the health of global demand for milk powder.

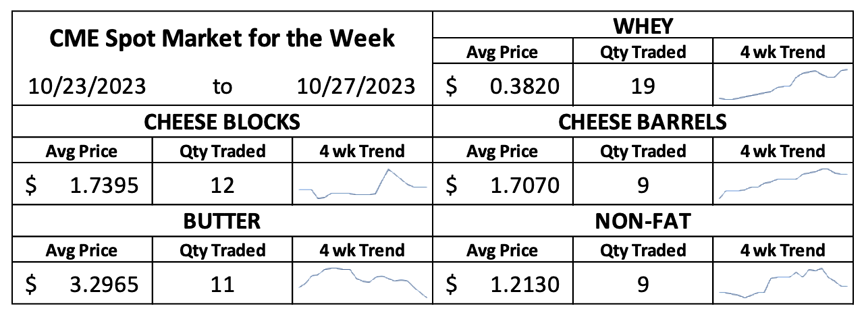

A poor showing at the Global Dairy Trade (GDT) Pulse auction spooked the milk powder markets this week and another month of disappointing trade data from China added further fright. The GDT debuted its Pulse auction in August, offering an indication of trends in whole milk powder (WMP) prices in the weeks between the full bimonthly events. This month, GDT added skim milk powder (SMP) to the Pulse docket. SMP values stabilized at the GDT in September and staged a convincing recovery in the first half of October. But SMP fell hard at the GDT Pulse event on Tuesday, retreating 4.7% from the comparable contract at last week’s full auction. WMP prices also took a step back, slipping 1.1% from last week’s mark. It’s too soon to know whether the Pulse auction represents a good indication of global SMP values or if it can be dismissed due to limited participation in such a nascent event. But it certainly sparked fears about the health of global demand for milk powder. CME spot nonfat dry milk slipped 3.5ȼ this week to $1.1975 per pound.

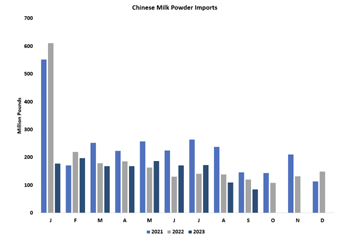

Chinese dairy import data was similarly unsettling. China brought in less than 42 million pounds of WMP in September, the lowest volume in five years. Chinese SMP imports also notched five-year lows at 43 million pounds. All told, Chinese milk powder imports fell 29.5% from year-ago volumes. These numbers are disheartening but not surprising. The product that arrived on China’s shores in September was purchased months before, at a time when China was notably absent from the global marketplace. But Chinese milk production has fallen below year-ago volumes for several months now, and Chinese buyers have been a little more active at the GDT and elsewhere. China still has large milk powder stocks, but it’s possible that China’s appetite for foreign product will improve going forward.

Chinese dairy import data was similarly unsettling. China brought in less than 42 million pounds of WMP in September, the lowest volume in five years. Chinese SMP imports also notched five-year lows at 43 million pounds. All told, Chinese milk powder imports fell 29.5% from year-ago volumes. These numbers are disheartening but not surprising. The product that arrived on China’s shores in September was purchased months before, at a time when China was notably absent from the global marketplace. But Chinese milk production has fallen below year-ago volumes for several months now, and Chinese buyers have been a little more active at the GDT and elsewhere. China still has large milk powder stocks, but it’s possible that China’s appetite for foreign product will improve going forward.

China’s imports of other dairy products were more reassuring. Butter and cheese imports both topped year-ago volumes once again. Chinese whey imports fell 11.6% short of the September 2022 tally, but Chinese imports of U.S. whey jumped from the very low volumes seen in February through August.

China’s imports of other dairy products were more reassuring. Butter and cheese imports both topped year-ago volumes once again. Chinese whey imports fell 11.6% short of the September 2022 tally, but Chinese imports of U.S. whey jumped from the very low volumes seen in February through August.

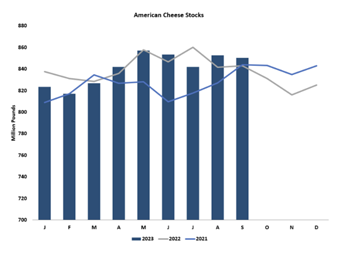

Closer to home, indications of demand were similarly mixed. USDA’s Cold Storage report showed that cheese stocks declined 23 million pounds from August to September. There were 1.47 billion pounds of cheese in  refrigerated warehouses at the end of last month, up just 0.2% from September 2022. The month-to-month decline was stronger than usual, which might hint that cheese demand was better than previously thought. But it’s more likely that buyers had some catching up to do after very slow sales in August. Inventories of American-style cheeses, including the Cheddar that determines CME spot market values, hardly budged, slipping just 2 million pounds for the month. American-style cheese stocks were up 0.9% from a year ago. There simply wasn’t enough good news in the Cold Storage report to prop up prices in Chicago. CME spot Cheddar blocks fell 5.75ȼ to $1.73. Barrels slipped 2.75ȼ to $1.6825.

refrigerated warehouses at the end of last month, up just 0.2% from September 2022. The month-to-month decline was stronger than usual, which might hint that cheese demand was better than previously thought. But it’s more likely that buyers had some catching up to do after very slow sales in August. Inventories of American-style cheeses, including the Cheddar that determines CME spot market values, hardly budged, slipping just 2 million pounds for the month. American-style cheese stocks were up 0.9% from a year ago. There simply wasn’t enough good news in the Cold Storage report to prop up prices in Chicago. CME spot Cheddar blocks fell 5.75ȼ to $1.73. Barrels slipped 2.75ȼ to $1.6825.

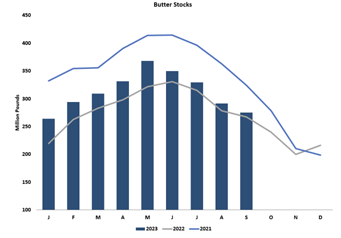

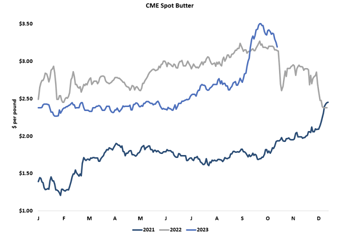

Butter stocks dropped 16.3 million pounds from August to September, clocking in at 275.4 million pounds. Butter stocks declined at a rapid clip in June through August, but the drawdown last some  momentum in September as soaring prices det would-be buyers. September 30 stocks were much lower than those seen in 2019 through 2021, which explains why prices climbed this fall. But inventories were 3% greater than in September 2022, undermining the argument that prices should top year-ago levels. CME spot butter prices dropped hard this week, plummeting 16.75ȼ to $3.1925 per pound. As grocers and buyers finish stocking up for the holiday baking season, prices are likely to fall further, echoing last year’s sudden selloff.

momentum in September as soaring prices det would-be buyers. September 30 stocks were much lower than those seen in 2019 through 2021, which explains why prices climbed this fall. But inventories were 3% greater than in September 2022, undermining the argument that prices should top year-ago levels. CME spot butter prices dropped hard this week, plummeting 16.75ȼ to $3.1925 per pound. As grocers and buyers finish stocking up for the holiday baking season, prices are likely to fall further, echoing last year’s sudden selloff.

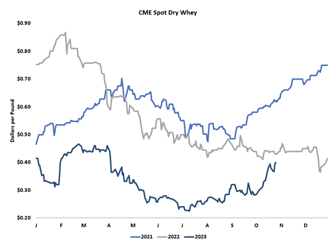

As it often does, the whey market bucked the trend. CME spot whey powder climbed a half-cent this week to 40ȼ, hitting that mark for the first time since April. Dairy producers can expect 60ȼ per cwt.  more from their Class III checks with whey at 40ȼ per pound than they could when it was languishing at 30ȼ. Stronger Chinese imports of U.S. whey likely helped at the margins, but the real reason for the whey rally is a dramatic increase in domestic demand for high-protein whey concentrates.

more from their Class III checks with whey at 40ȼ per pound than they could when it was languishing at 30ȼ. Stronger Chinese imports of U.S. whey likely helped at the margins, but the real reason for the whey rally is a dramatic increase in domestic demand for high-protein whey concentrates.

With most dairy products in the red, both Class III and Class IV futures took a sizeable step back this week. November and December Class III futures lost 72ȼ and 80ȼ, respectively. The futures forecast milk in the mid-$17s into early next year. Class IV contracts lost nearly as much ground, but prices are much, much higher. The October contract settled at $21.60, with November a dollar lower than that and December at $19.49.

Combines are rolling and grain prices are falling. December corn settled today at $4.8075 per bushel,

down more than 15ȼ for the week. There is plenty of corn on the U.S. balance sheet to satisfy domestic demand and keep prices relatively low. Grain values will spike if the trade becomes worried about a steep decline in South American crop prospects, which would quickly boost U.S. corn and soybean exports. But the forecast calls for showers in the driest parts of northern Brazil and Argentina, so those fears are taking a backseat for now. Indeed, U.S. corn and soy export prospects have diminished in the past few weeks as the dollar strengthened and U.S. export logistics faced additional complications. Low water levels on the Mississippi River have reduced barge traffic, and – just as grain started to flow in the northern United States and southern Canada – a labor strike has shut down all shipping on the St. Lawrence Seaway, a vital artery connecting the Atlantic Ocean to ports on the Great Lakes.

Nonetheless, USDA reported a spate of new corn and soybean export sales this week, and soybean meal is leaving our shores at a record-setting pace. Argentina is the world’s largest soybean meal supplier, and the U.S. is filling in the vacuum left by last year’s very small Argentine soy crop. December soybean meal jumped to $442.40 per ton today, up $18.50 from last Friday.

Original Report At: https://www.jacoby.com/market-report/health-of-global-demand-for-milk-powder-sparks-fear/