The T.C. Jacoby Weekly Market Report Week Ending December 8, 2023

The T.C. Jacoby Weekly Market Report Week Ending December 8, 2023

Cheese vats remain full, despite lower milk output. U.S. cheese production reached 1.19 billion pounds in October, up 0.8% from the year before. Given the continued investment in U.S. cheese production capacity, cheese output is likely to grow for the foreseeable future, to the detriment of U.S. cheese and Class III prices. But the details of U.S. cheese production offered some fodder for the bulls. In October, cheesemakers shifted milk into fresh cheeses like cream cheese and Neufchatel (+6.8% year-over-year), cottage cheese (+13%), Hispanic cheeses (+5.7%), ricotta (+12.2%) and Mozzarella (+2.3%).

Cheese vats remain full, despite lower milk output. U.S. cheese production reached 1.19 billion pounds in October, up 0.8% from the year before. Given the continued investment in U.S. cheese production capacity, cheese output is likely to grow for the foreseeable future, to the detriment of U.S. cheese and Class III prices. But the details of U.S. cheese production offered some fodder for the bulls. In October, cheesemakers shifted milk into fresh cheeses like cream cheese and Neufchatel (+6.8% year-over-year), cottage cheese (+13%), Hispanic cheeses (+5.7%), ricotta (+12.2%) and Mozzarella (+2.3%). Unlike Cheddar, fresh cheeses are made to be consumed immediately. They won’t show up on a Cold Storage report or at the CME spot market in Chicago. Stronger output of these cheeses hints at better domestic demand and greater export prospects for Mozzarella after a cruel summer of slower orders. The focus on these cheese varieties allowed U.S. cheesemakers to turn out 2.5% less Cheddar in October than they did the year before.

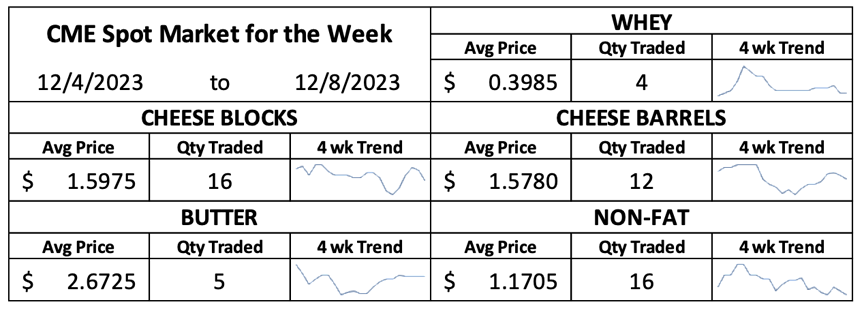

While the latest production data and reports of lower milk and cheese output in Europe fueled hopes for a rebound in U.S. cheese exports, shipments in October remained soft. The U.S. sent just 76 million pounds of cheese abroad in October, 3.4% less than the year before. Shipments to Mexico set a new high for the month, but sales to key buyers in Asia faltered, as cheaper European product dominated those markets. Despite the disappointing export data, U.S. cheese prices climbed this week, boosted by continued strength in European pricing and an impressive jump at Tuesday’s Global Dairy Trade (GDT) auction. CME spot Cheddar blocks rallied 6ȼ this week to $1.58 per pound. Barrels advanced 3ȼ to $1.55.

The Dairy Products report confirmed that whey processors have finally shifted more of the whey stream to whey protein concentrates and isolates, leaving less for the drier. Dry whey output slumped 1.2% below year-ago volumes in September and October output was down 2.6% year over year. Whey stocks waned, but they remain above year-ago levels for now, and exports are soft. Dry whey exports fell to 30.8 million pounds in October, down 37.6% from a year ago. U.S. whey exports are likely to struggle until Chinese hog producers are back in the black, and that may not happen until the Chinese economy finds its footing. Whey prices are holding above the summer lows, but they’re not climbing. This week CME spot whey slipped to 39.5ȼ, down a half-cent from last Friday.

Milk powder prices also retreated, despite convincing rebounds in both skim milk powder (SMP) and whole milk powder (WMP) values at the GDT auction. CME spot nonfat dry milk (NDM) lost 1.5ȼ this week and dropped to $1.165, the lowest price since September. U.S. milk powder output remains in the doldrums, as cheesemakers continue to pull milk and cream away from the dryer and the butter churn. Combined production of NDM and SMP totaled 169.1 million pounds, down 12.9% from October 2022. Manufacturers’ stocks of NDM dropped to 223.6 million pounds, down 10.8% year over year to the lowest stockpile since November 2019. But whittling down inventories through industry attrition is not enough to lift prices any further. We’ll need better global demand for milk powder or even steeper declines in milk powder output from Europe before prices can climb. For now, U.S. exports are too slow to provide much support. U.S. milk powder exports lagged last year’s volumes by 11.8% in October.

Butter production totaled 160.6 million pounds in October, down 0.9% from a year ago. Exports are abysmal, but it doesn’t matter. The U.S. has a butterfat deficit, and butter prices remain well supported. CME spot butter rallied 1.5ȼ this week to $2.67. That’s down significantly from the pre-holiday peak, but it’s still a pretty hefty price.

The setback in the milk powder market weighed on nearby Class IV futures. The December contract slipped 4ȼ to $19.20 per cwt., and January Class IV futures tumbled 28ȼ to $18.94. But deferred Class IV contracts gained a little ground this week and so did most Class III futures. However, Class III prices remain dishearteningly low. December Class III settled at $16.20 and January finished at $16.34. Further down the board, prices look more promising, but there will be plenty of red ink between here and there.

The corn market held in a relatively tight range. March corn futures settled today at $4.855 per bushel, up a fraction of a cent from last Friday. The soy complex continued to retreat. January beans closed at $13.04, down 41.5ȼ for the week. January soybean meal finished at $404.70 per ton, down another $8. There were no surprises in USDA’s monthly update to crop balance sheets. The agency confirmed that U.S. and global corn supplies are plentiful, while soybean and soybean meal stocks are tighter. The United States is going to crush a record volume of soybeans into oil and meal in the 2023-24 crop year. But soybean meal exports will also set a new all-time high, so U.S. dairy producers and livestock growers will have to pay up to keep their share of U.S. soybean meal at home.

Original Report At: https://www.jacoby.com/market-report/fresh-cheese-production-rises-unexpectedly/