The T.C. Jacoby Weekly Market Report Week Ending July 30, 2021

Although this year’s losses have none of last year’s frenzy, the ink is just as red. But it may be a while before lower prices translate to less milk.

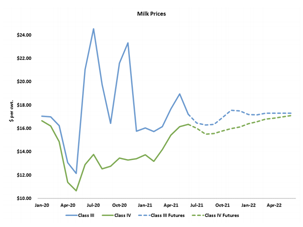

Like a balloon with a pinhole, the dairy markets are slowly deflating. The summer setback lacks the drama of July 2020, when – flush with government largesse – the cheese market balloon grew and grew and grew until it burst spectacularly. Although this year’s losses have none of last year’s frenzy, the ink is just as red. Both Class III and Class IV futures posted double-digit declines once again this week. September and October Class III settled below $17 per cwt., at their lowest values so far in 2021. In Class IV, the September through November contracts plumbed life-of-contract lows in the $15s. Given historically high costs for feed, fuel, freight, and labor, these values are extremely disappointing for dairy producers.

Like a balloon with a pinhole, the dairy markets are slowly deflating. The summer setback lacks the drama of July 2020, when – flush with government largesse – the cheese market balloon grew and grew and grew until it burst spectacularly. Although this year’s losses have none of last year’s frenzy, the ink is just as red. Both Class III and Class IV futures posted double-digit declines once again this week. September and October Class III settled below $17 per cwt., at their lowest values so far in 2021. In Class IV, the September through November contracts plumbed life-of-contract lows in the $15s. Given historically high costs for feed, fuel, freight, and labor, these values are extremely disappointing for dairy producers.

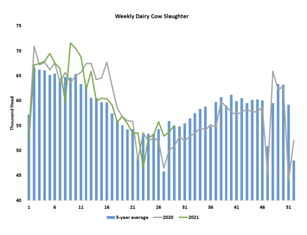

But it may be a while before lower prices translate to less milk. Dairy slaughter has accelerated relative to the 2020 pace. But, as is always the case during the summer, the numbers aren’t all that high. Although slaughter volumes have eclipsed the prior year for the past six weeks, year-to-date slaughter is still 0.2% behind the 2020 pace, and the dairy herd is 1.6% larger than it was a year ago. Dairy producers are clearly not culling cows at the pace required to significantly shrink the herd. And, given how many cows we are milking, it will take significant slaughter to bring production back down to a level that necessitates higher prices. Low prices are the best cure for low prices, but the healing process is often painful and achingly slow.

But it may be a while before lower prices translate to less milk. Dairy slaughter has accelerated relative to the 2020 pace. But, as is always the case during the summer, the numbers aren’t all that high. Although slaughter volumes have eclipsed the prior year for the past six weeks, year-to-date slaughter is still 0.2% behind the 2020 pace, and the dairy herd is 1.6% larger than it was a year ago. Dairy producers are clearly not culling cows at the pace required to significantly shrink the herd. And, given how many cows we are milking, it will take significant slaughter to bring production back down to a level that necessitates higher prices. Low prices are the best cure for low prices, but the healing process is often painful and achingly slow.

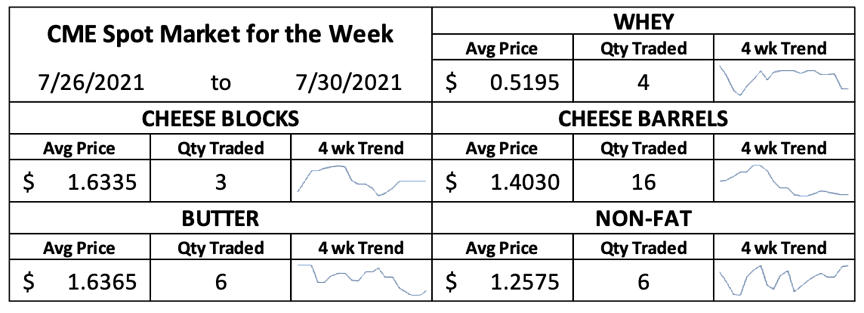

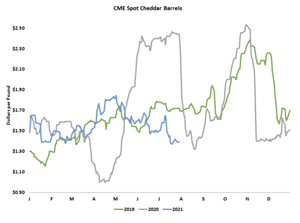

USDA’s Dairy Market News reports, “Milk volumes are plentiful enough for strong cheese production schedules.” But packaging issues continue to shift some milk out of blocks and into barrels. The proof is in the prices. Cheddar blocks closed today at $1.635 per pound, up a nickel this week and 8.25ȼ higher than where they began the month. In contrast, barrels fell 1.25ȼ this week to $1.39. They are down 11.25ȼ for the month and not far from the calendar-year lows. Demand is good, but output is strong.

Heavy production continues to weigh on the whey market as well. CME spot whey powder fell 3.5ȼ this week to 50.25ȼ. Spot dry whey finished July 5.75ȼ lower than where it began, trimming roughly 35ȼ from implied Class III values in the process. Demand for highprotein whey products remains impressive, but whey powder is piling up nonetheless.

Heavy production continues to weigh on the whey market as well. CME spot whey powder fell 3.5ȼ this week to 50.25ȼ. Spot dry whey finished July 5.75ȼ lower than where it began, trimming roughly 35ȼ from implied Class III values in the process. Demand for highprotein whey products remains impressive, but whey powder is piling up nonetheless.

Plentiful cream and well-stocked warehouses are dragging on butter values. This week CME spot butter probed five-month lows. It closed today at $1.6425, down 5.25ȼ from last Friday and nearly a dime lower than where it began the month.

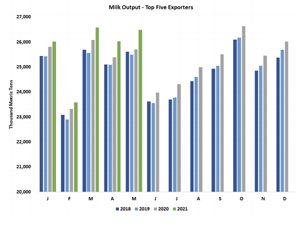

Despite the summer heat, there is more than enough milk to keep driers busy. Demand is steady, but shipping issues are slowing the flow of product from manufacturers to end users at home and abroad. While foreign milk powder values took another step back this week, CME spot nonfat dry milk (NDM) rallied. It closed today at $1.2675, up 1.5ȼ this week and up just 0.75ȼ for the month. Milk powder values could come under further pressure in the months to come if global demand falters. Dairy Market News notes that some Southeast Asian countries likely ordered extra skim milk powder (SMP) in the first half of the year, hoping to avoid shortages caused by shipping delays. But now, “inventories may be building to the point where buyers are willing to wait before making more purchases.” If that’s the case, a slowdown in demand could collide with growing supplies. Global milk output is high and rising. In May, milk production among the four largest

Despite the summer heat, there is more than enough milk to keep driers busy. Demand is steady, but shipping issues are slowing the flow of product from manufacturers to end users at home and abroad. While foreign milk powder values took another step back this week, CME spot nonfat dry milk (NDM) rallied. It closed today at $1.2675, up 1.5ȼ this week and up just 0.75ȼ for the month. Milk powder values could come under further pressure in the months to come if global demand falters. Dairy Market News notes that some Southeast Asian countries likely ordered extra skim milk powder (SMP) in the first half of the year, hoping to avoid shortages caused by shipping delays. But now, “inventories may be building to the point where buyers are willing to wait before making more purchases.” If that’s the case, a slowdown in demand could collide with growing supplies. Global milk output is high and rising. In May, milk production among the four largest

dairy exporters other than the United States outpaced the prior year by 2.5%. Throw the U.S. in the mix, and output among the big five was 3.1% greater than in May 2020. That’s the largest year-over-year increase since late 2017, which does not bode well for prices in the coming year.

Back and forth and back and forth. The grain and oilseed markets traversed the same ground several times this week and ended up not far from where they started. September corn closed today at $5.47 per bushel, down a quarter-cent from last Friday. December corn futures, the benchmark for new-crop corn, rallied 2.25ȼ to $5.4525. Soybean and soybean meal contracts were similarly steady. November soybeans closed at $13.4925 per bushel, while September soybean meal finished at $351.30 per ton.

The corn crop has made it through the critical pollination phase in fine shape overall. USDA assessed 64% of the crop in good or excellent condition, although ratings lag considerably in Minnesota (38%), South Dakota (30%), and North Dakota (21%), where rain has been scarce. Much of the Northern Plains enjoyed a good soak today, but the Corn Belt forecast looks relatively dry for the next week. The market is marking time until fall, when it can be assured of a good crop. In the meantime, feed expenses remain relatively lofty.

Original Report at: Jacoby