The T.C. Jacoby Weekly Market Report Week Ending September 22, 2023

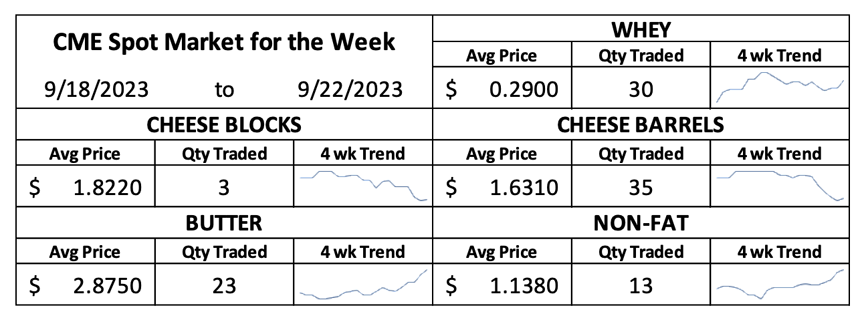

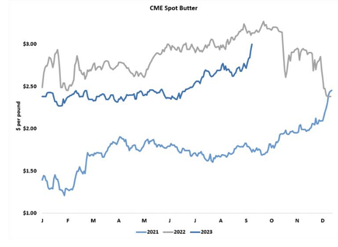

CME spot butter soared an astounding 28.25ȼ this week and closed right at the $3 mark. Exports are out of the question, but domestic demand is firm, and butter churns are running light.

Three dollar butter is back. CME spot butter soared an astounding 28.25ȼ this week and closed right at the $3 mark. Exports are out of the question, but domestic demand is firm, and butter  churns are running light. Cream supplies are tight thanks to lower milk output and fierce competition from cheese vats and makers of whips and dips. Butter buyers are anxious as baking season looms large. They fear a repeat of last year’s persistently high prices and they’re chasing the market upward. October and November futures jumped 7.5ȼ today, the maximum gain allowed under the CME’s daily trading limits.

churns are running light. Cream supplies are tight thanks to lower milk output and fierce competition from cheese vats and makers of whips and dips. Butter buyers are anxious as baking season looms large. They fear a repeat of last year’s persistently high prices and they’re chasing the market upward. October and November futures jumped 7.5ȼ today, the maximum gain allowed under the CME’s daily trading limits.

Milk powder prices also climbed, buoyed by a strong showing at the Global Dairy Trade (GDT) auction. Buyers in North Asia – which includes South Korea, Japan, and, most notably, China – snapped up more milk powder at the GDT than they have in two years, and they pushed prices higher to boot. Both whole milk powder (WMP) prices and the GDT Index rallied 4.6%, their second straight positive performance. GDT skim milk powder (SMP) finally showed some signs of life as well. In Chicago, CME spot nonfat dry milk (NDM) leapt 5.75ȼ to $1.17 per pound, matching its highest price since May.

Global milk powder production is slowing as milk output wanes and manufacturers direct milk to other uses. In Europe and the United Kingdom, milk collections topped year-ago volumes by just  0.2% in June and July, and driers ran light. New Zealand’s new season is off to a poor start. August milk solids output fell 0.9% from the prior year to the lowest volume since 2017. U.S. milk production continues to shrink. USDA trimmed its estimate of July milk output and now reports mid-summer production down 0.7% from July 2022. But August milk output was larger than expected, down just 0.2% from last year.

0.2% in June and July, and driers ran light. New Zealand’s new season is off to a poor start. August milk solids output fell 0.9% from the prior year to the lowest volume since 2017. U.S. milk production continues to shrink. USDA trimmed its estimate of July milk output and now reports mid-summer production down 0.7% from July 2022. But August milk output was larger than expected, down just 0.2% from last year.

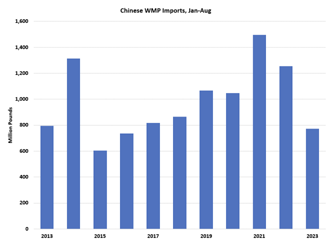

Lower milk production is obviously supportive of milk powder prices, but demand matters too. The market was relieved to see China getting more aggressive at the GDT, but it remains wary, and the latest round of trade data offered little fodder for the bulls. China imported less WMP last month than it has in any August since 2016. China’s year-to-date WMP imports also stand at seven-year lows. And Chinese SMP imports, which had been going strong, fell 36% short of year-ago volumes last month. Despite disappointing trade  from China, the U.S. milk powder market is as taut as a bowstring. It will shoot even higher at the first sign that China’s appetite for foreign milk powder has recovered.

from China, the U.S. milk powder market is as taut as a bowstring. It will shoot even higher at the first sign that China’s appetite for foreign milk powder has recovered.

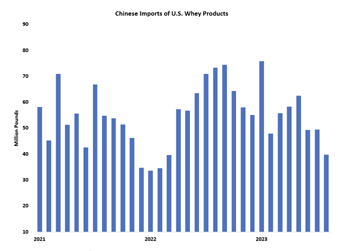

Whey powder followed NDM upward. CME spot dry whey gained a half-cent and reached 30.5ȼ. High-protein whey prices continue to climb, and manufacturers are sending more of the whey stream into concentrates, which is helping to tighten up supplies of whey powder. But the whey market is also capped by poor demand from China. Chinese imports of U.S. whey fell to a 17-month low in August.

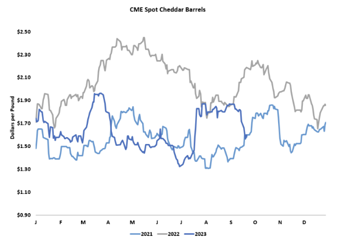

Cheese bucked the trend and suffered huge losses this week. CME spot Cheddar blocks fell a dime to $1.78 per pound, a two-month low. Barrels were even worse. They plummeted 21ȼ to $1.60, also the lowest price in two months. High prices this summer have stymied export opportunities this fall, and, now that the heat has abated, there is more fresh Cheddar making its way to Chicago. The trade expects cheese output to remain strong, as Midwestern milk output held firm in August despite the heat. There are also plenty of cows in the cheese states. Dairy slaughter volumes are not running quite as hot as they did this summer, and USDA reported no change in cow numbers from July to August. However, the agency did trim its assessment of the July milk-cow herd by 10,000 head, confirming the prevalence of sellouts and very high cull rates this summer.

Cheese bucked the trend and suffered huge losses this week. CME spot Cheddar blocks fell a dime to $1.78 per pound, a two-month low. Barrels were even worse. They plummeted 21ȼ to $1.60, also the lowest price in two months. High prices this summer have stymied export opportunities this fall, and, now that the heat has abated, there is more fresh Cheddar making its way to Chicago. The trade expects cheese output to remain strong, as Midwestern milk output held firm in August despite the heat. There are also plenty of cows in the cheese states. Dairy slaughter volumes are not running quite as hot as they did this summer, and USDA reported no change in cow numbers from July to August. However, the agency did trim its assessment of the July milk-cow herd by 10,000 head, confirming the prevalence of sellouts and very high cull rates this summer.

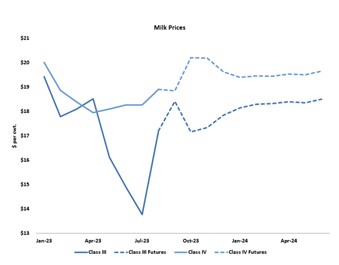

The setback in the cheese markets took a heavy toll on Class III prices. October Class III fell 94ȼ this week to an inadequate $17.16 per cwt. November was not much better. It dropped 99ȼ to $17.34. Fourth quarter Class III futures now average just $17.45, which will not pay the bills. Dairy producers outside the cheese states will enjoy much better prices, although the share of their milk check derived from Class IV is likely falling as underutilized balancing plants represent an increasingly small share of the blend price. October Class IV jumped $1.24 this week and both October and November Class IV topped $20 for the first time since February. Dairy producers will certainly welcome these higher prices. This has been a tough year on the farm, and they have a lot of rebuilding to do.

The setback in the cheese markets took a heavy toll on Class III prices. October Class III fell 94ȼ this week to an inadequate $17.16 per cwt. November was not much better. It dropped 99ȼ to $17.34. Fourth quarter Class III futures now average just $17.45, which will not pay the bills. Dairy producers outside the cheese states will enjoy much better prices, although the share of their milk check derived from Class IV is likely falling as underutilized balancing plants represent an increasingly small share of the blend price. October Class IV jumped $1.24 this week and both October and November Class IV topped $20 for the first time since February. Dairy producers will certainly welcome these higher prices. This has been a tough year on the farm, and they have a lot of rebuilding to do.

Choppers and combines are rolling through the Corn Belt. Yields are extremely variable, but most farmers have been pleasantly surprised at how well their corn has held up through strange and often unfavorable weather. There is plenty of corn, and prices are approaching two-year lows. December corn settled today at $4.7725 per bushel, up a penny from last week. Corn futures often notch their seasonal low in late September. This looks like an opportunity for dairy producers to lock in grain costs at relatively attractive levels.

Soybean supplies are much tighter, and the soy crop appears to have struggled a bit more than corn through the late-season heat and drought. Crop analysts warn that scarce soybean supplies could reduce the crush and limit soybean meal output over the next 12 months. Nonetheless, soybean and soybean meal prices continued to fade. November soybeans finished at $12.9625, down another 44ȼ this week. December soybean meal settled at $385.80 per ton, down $6.30 from last Friday.

Original Report At: https://www.jacoby.com/market-report/cme-spot-butter-soars/