The T.C. Jacoby Weekly Market Report Week Ending May 14, 2021

Some dairy producers are partially shielded from higher feed expenses through a combination of inventories, contracts, and farming. Many have been battered by low Class IV values and widespread depooling, and are now being clobbered by immense feed bills. They are reeling.

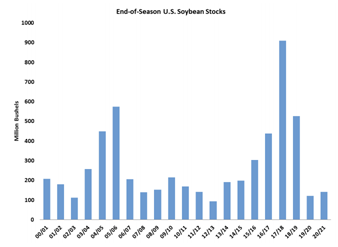

Soybeans made their debut at the Chicago Board of Trade in 1936. In the past 85 years, they have traded above $16 per bushel in just 61 daily trading sessions, including four times this week. Record-breaking exports have reduced U.S. soybean supplies to impossibly low levels. USDA projects that when the season ends on August 31, there will be just 120 million bushels of soybeans left over, an all-time low. With stocks dwindling, July soybean futures briefly touched $16.675 per bushel on Wednesday, the highest price since 2012, when crops withered in a crippling drought.

Soybeans made their debut at the Chicago Board of Trade in 1936. In the past 85 years, they have traded above $16 per bushel in just 61 daily trading sessions, including four times this week. Record-breaking exports have reduced U.S. soybean supplies to impossibly low levels. USDA projects that when the season ends on August 31, there will be just 120 million bushels of soybeans left over, an all-time low. With stocks dwindling, July soybean futures briefly touched $16.675 per bushel on Wednesday, the highest price since 2012, when crops withered in a crippling drought.

USDA expects big exports in the 2021-22 crop year as well, although the volumes will likely fall short of the staggering totals sent abroad in the current season. In its first detailed look at the next crop year, the agency called for bigger soy acreage and higher yields than last harvest. Even so, next year’s ending stocks will be historically low at 140 million bushels. There is no room for error in the soybean balance sheet and prices will likely remain high. Although soybean and soybean meal futures took a big step back on Thursday, they started to climb once again today. July soybeans closed at $15.84 per bushel, down 5.75ȼ this week.

USDA expects big exports in the 2021-22 crop year as well, although the volumes will likely fall short of the staggering totals sent abroad in the current season. In its first detailed look at the next crop year, the agency called for bigger soy acreage and higher yields than last harvest. Even so, next year’s ending stocks will be historically low at 140 million bushels. There is no room for error in the soybean balance sheet and prices will likely remain high. Although soybean and soybean meal futures took a big step back on Thursday, they started to climb once again today. July soybeans closed at $15.84 per bushel, down 5.75ȼ this week.

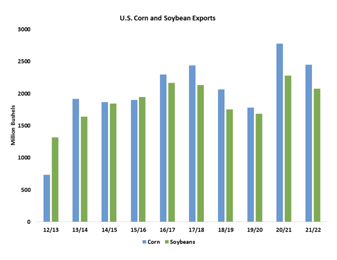

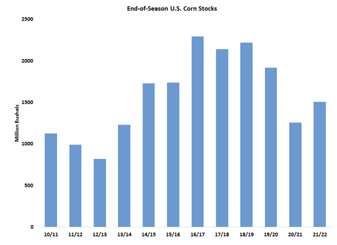

Record-breaking exports are tightening corn supplies too, although not to the extremes seen in the soybean market. USDA expects that when the season ends in a few months, corn stocks will fall below 1.26 billion bushels, the smallest ending inventories since 2013-14. USDA stuck with the 91.1 million acres of corn it called for in the Prospective Plantings report, but corn prices have done nothing but climb since the agency surveyed farmers in March. Farmers have likely increased their ambitions for corn acreage since then. The agency calls for a trend-line yield of 179.5 bushels per acre. If the weather cooperates, this record-setting yield would help U.S. corn inventories back over 1.5 billion bushels by the end of next season. The prospect of a huge corn crop weighed heavily on the futures market. July corn settled at $6.7475, down 57.5ȼ from last Friday.

Record-breaking exports are tightening corn supplies too, although not to the extremes seen in the soybean market. USDA expects that when the season ends in a few months, corn stocks will fall below 1.26 billion bushels, the smallest ending inventories since 2013-14. USDA stuck with the 91.1 million acres of corn it called for in the Prospective Plantings report, but corn prices have done nothing but climb since the agency surveyed farmers in March. Farmers have likely increased their ambitions for corn acreage since then. The agency calls for a trend-line yield of 179.5 bushels per acre. If the weather cooperates, this record-setting yield would help U.S. corn inventories back over 1.5 billion bushels by the end of next season. The prospect of a huge corn crop weighed heavily on the futures market. July corn settled at $6.7475, down 57.5ȼ from last Friday.

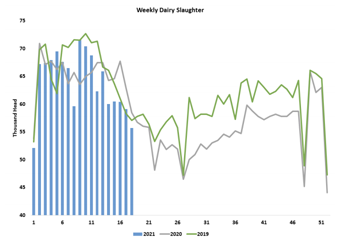

Although crop valuesfell back this week, they are still historically high. Dairy producers are paying more to feed their cows than they have in years, and they likely won’t see much relief until a bumper crop is assured. Even then, soybean meal is likely to remain pricey. Expensive feed and staggering construction costs are likely suppressing dairy producers’ appetite to build new facilities, but there is no evidence that they are crimping production just yet. Dairy producers were still adding cows at a rapid clip earlier this spring. In March, the milkcow herd reached a 25-year high. Slaughter volumes remain well behind the pace set in 2019 and 2020, when the herd was notably smaller than it is today.

Although crop valuesfell back this week, they are still historically high. Dairy producers are paying more to feed their cows than they have in years, and they likely won’t see much relief until a bumper crop is assured. Even then, soybean meal is likely to remain pricey. Expensive feed and staggering construction costs are likely suppressing dairy producers’ appetite to build new facilities, but there is no evidence that they are crimping production just yet. Dairy producers were still adding cows at a rapid clip earlier this spring. In March, the milkcow herd reached a 25-year high. Slaughter volumes remain well behind the pace set in 2019 and 2020, when the herd was notably smaller than it is today.

Big milk checks have likely numbed the impact of exorbitant feed costs for dairy producers who derive most of their revenue from Class III. And some dairy producers are at least partially shielded from higher feed expenses through a combination of inventories, contracts, and farming. But many have been battered by low Class IV values and widespread depooling, and they are now being clobbered by immense feed bills. They are reeling.

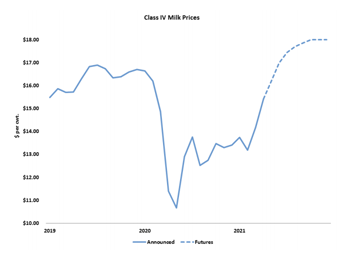

Fortunately, Class IV values are on the rise. Most contracts added between 25 and 45ȼ this week. Second-half futures scored life of contract highs and are now projected to average $17.84 per cwt., sharply higher than in the last six months of 2020, when Class IV contracts averaged a pitiful $13.21. Class III futures moved higher early in the week and then fell back. But they still gained ground. Most Class III futures contracts settled 15ȼ to 45ȼ higher than last Friday. The June through November contracts sit north above $19.

Fortunately, Class IV values are on the rise. Most contracts added between 25 and 45ȼ this week. Second-half futures scored life of contract highs and are now projected to average $17.84 per cwt., sharply higher than in the last six months of 2020, when Class IV contracts averaged a pitiful $13.21. Class III futures moved higher early in the week and then fell back. But they still gained ground. Most Class III futures contracts settled 15ȼ to 45ȼ higher than last Friday. The June through November contracts sit north above $19.

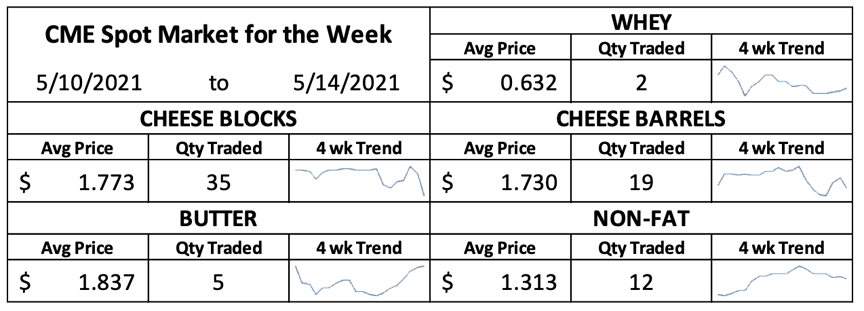

After a couple rough weeks, the butter market came roaring back. CME spot butter jumped 10.5ȼ from Friday to Friday and now stands at $1.875 per pound. Booming ice cream sales have helped to tighten cream supplies in the West and slow churning activity at the margins. However, in the rest of the country, cream supplies are not as

tight as they were a few weeks ago. Butter makers report that demand is coming in fits and starts. According to Dairy Market News, “Accurately forecasting demand remains a challenge for dairy manufacturers and food service customers both.”

CME spot nonfat dry milk slipped 2.25ȼ this week to $1.30. Domestic buyers have started to balk at high prices, and sales are slowing a bit. But exports remain strong. After several months in the doldrums, Mexico is catching up on its milk powder purchases. Drought is widespread south of the border, which is likely to raise costs and reduce milk output down the road. But for now, milk continues to flow. Mexican milk production was up 2.2% in April and is up 2.4% for the year to date.

CME whey powder values climbed 1.25ȼ this week to 64ȼ. The futures consolidated. Exports are moving and demand for high-protein whey products remains strong, but domestic whey powder buyers are backing off a little in hopes that prices will falter.

CME spot Cheddar barrels climbed through most of the week and reached $1.78 on Thursday. But they dropped a nickel today and closed at $1.73, up just 0.25ȼ from last Friday. Blocks dropped 2.25ȼ to $1.725. At some point, formidable cheese output could weigh on prices, but for now, cheese and Class III values remain lofty.